[课程资料] 高级统计方法书后习题(八)

本系列内容为《统计学习导论——基于R应用》(机械工业出版社)部分课后习题答案。

本章为8.4节、9.7节习题答案。

声明:本博客中的习题分享仅供学习和参考之用。请勿将其用于任何形式的学术欺骗、抄袭或违反学术诚信的行为。尊重知识,诚实学习。

如果您发现文章内容中任何不妥或错误之处,请随时通过联系方式或评论功能与我交流,以便我进行改正和完善。

一、概念题

8.4.2

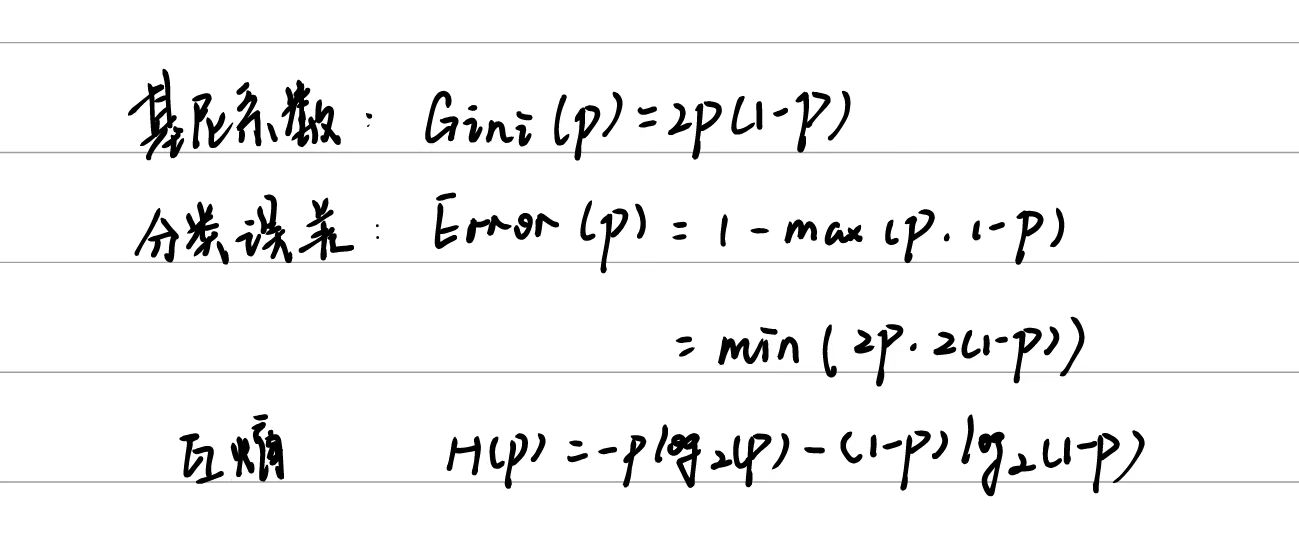

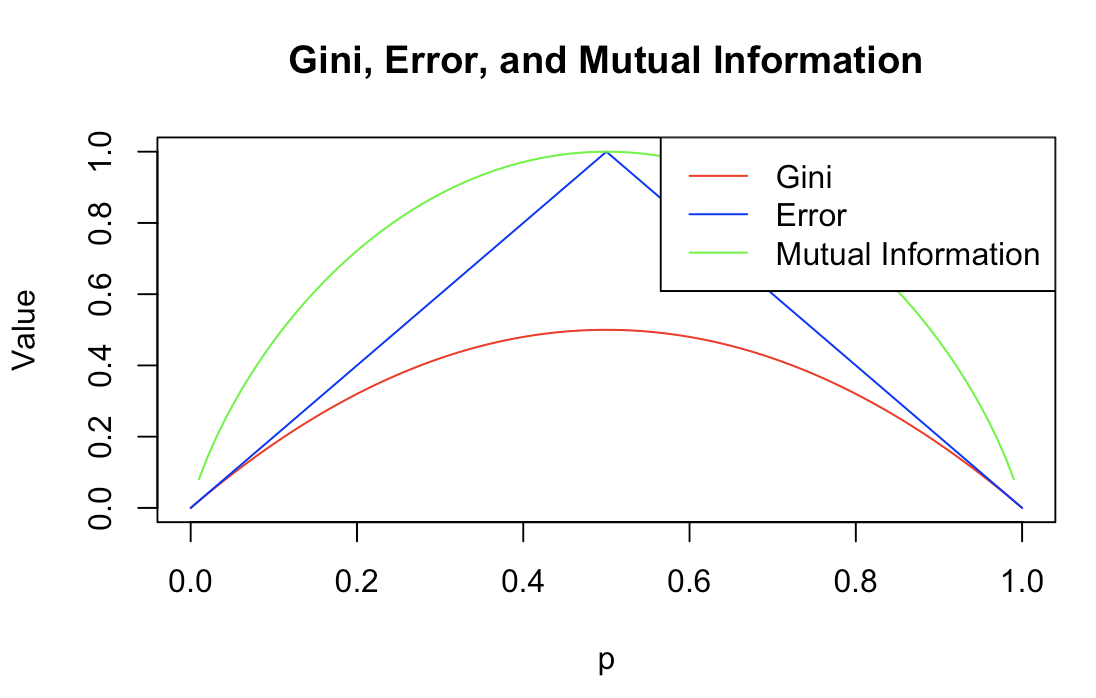

8.4.3

# 定义概率范围

p = seq(0, 1, by = 0.01)

# 计算基尼系数

gini = 2 * p * (1 - p)

#gini = 1 - p^2 - (1-p)^2

# 计算分类误差

error = pmin(2 * p, 2 * (1 - p))

# 计算互熵

mutual_info = -p * log2(p) - (1 - p) * log2(1 - p)

# 绘图

plot(p, gini, type = "l", col = "red", xlab = "p", ylab = "Value", ylim = c(0, 1), main = "Gini, Error, and Mutual Information")

lines(p, error, type = "l", col = "blue")

lines(p, mutual_info, type = "l", col = "green")

legend("topright", legend = c("Gini", "Error", "Mutual Information"), col = c("red", "blue", "green"), lty = 1)

8.4.5

多数投票:当P(类别是Red|X的概率)大于0.5的时候,认为数据是Red类别。而满足P>0.5的数据有6个,也就是这6个数据指向Red类,剩下4个数据指向Green类,所以根据多数投票,该数据为Red。

平均概率:该数据为Red的平均概率为0.45,小于0.5,故认为Green。

9.7.2

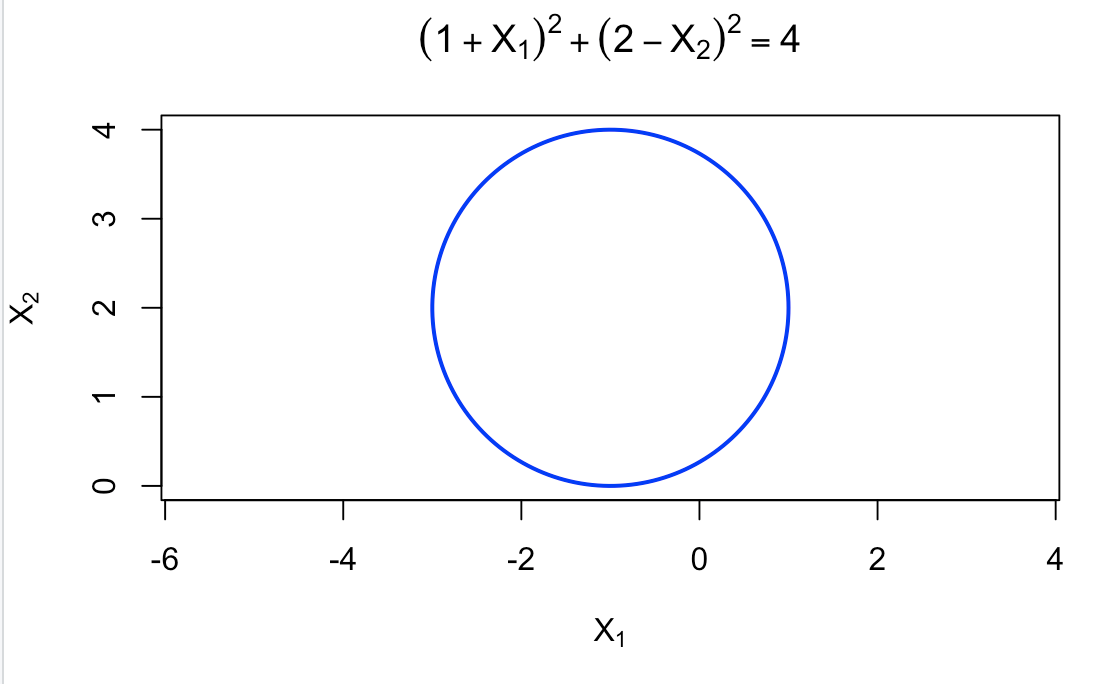

(a)

# 设置图形窗口 plot(-3:1, 0:4, type = "n", xlab = expression(X[1]), ylab = expression(X[2]), asp = 1) title(main = expression((1 + X[1])^2 + (2 - X[2])^2 == 4)) # 计算圆的坐标 theta <- seq(0, 2 * pi, length.out = 200) x <- -1 + 2 * cos(theta) y <- 2 + 2 * sin(theta) # 绘制圆 lines(x, y, col = "blue", lwd = 2)

(b)

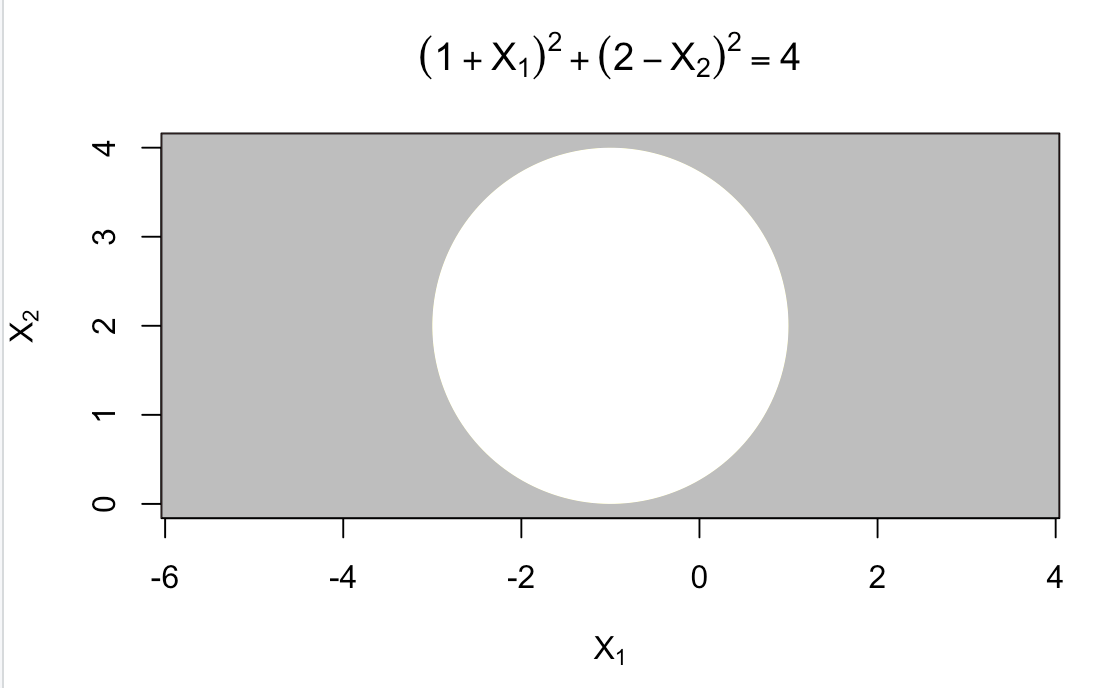

# 填充圆外部(>4的点集) rect(par("usr")[1], par("usr")[3], par("usr")[2], par("usr")[4], col = "grey") polygon(x, y, col = "white", border = NA) # 填充圆内部(<=4的点集) polygon(x, y, col = "white", border = NA)

灰色为>4点集,白色为<4点集。

(c)

(0,0):蓝色 (-1,1):红色 (2,2):蓝色 (3,8):蓝色

(d)

化简后可以得到5+2X_1-4X_2+X_1^2+X_2^2\gt4。

这个决策边界对于X_1和X_2不是线性的,但是对于X_1,X_2,X_1^2,X_2^2是线性的。

9.7.3

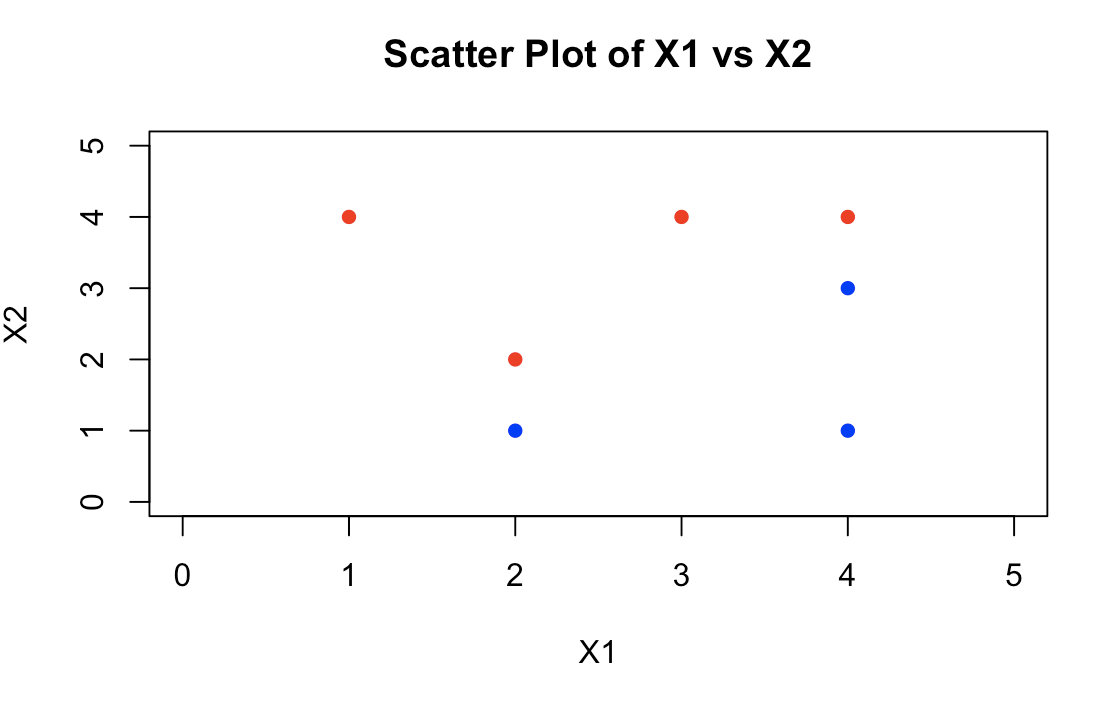

(a)

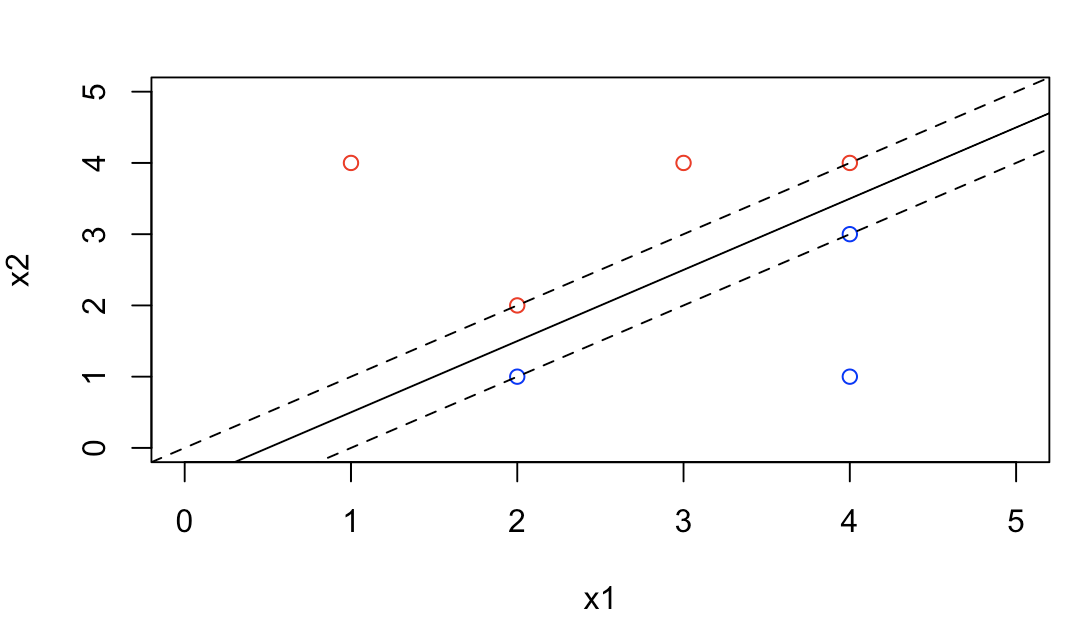

# 定义数据 x1 <- c(3, 2, 4, 1, 2, 4, 4) x2 <- c(4, 2, 4, 4, 1, 3, 1) # 定义颜色(根据类别) colors <- c("red", "red", "red", "red", "blue", "blue", "blue") # 绘制散点图 plot(x1, x2, col = colors, pch = 16, xlim = c(0, 5), ylim = c(0, 5), xlab = "X1", ylab = "X2", main = "Scatter Plot of X1 vs X2")

(b) 决策边界表达式:-X_1+X_2+0.5\gt0。

(c)

\beta_0=0.5,\beta_1=-1,\beta_2=1。

(d)

plot(x1, x2, col = colors, xlim = c(0, 5), ylim = c(0, 5)) abline(-0.5, 1) abline(-1, 1, lty = 2) abline(0, 1, lty = 2)

(e)

支持向量为坐标(2,1) (4,3) (2,2) (4,4)的四个数据。

(f)

非支持向量的移动对于决策边界的影响较小,而且第七个观测点距离间隔较远,它的轻微移动并不会影响最大间隔超平面。

(g)

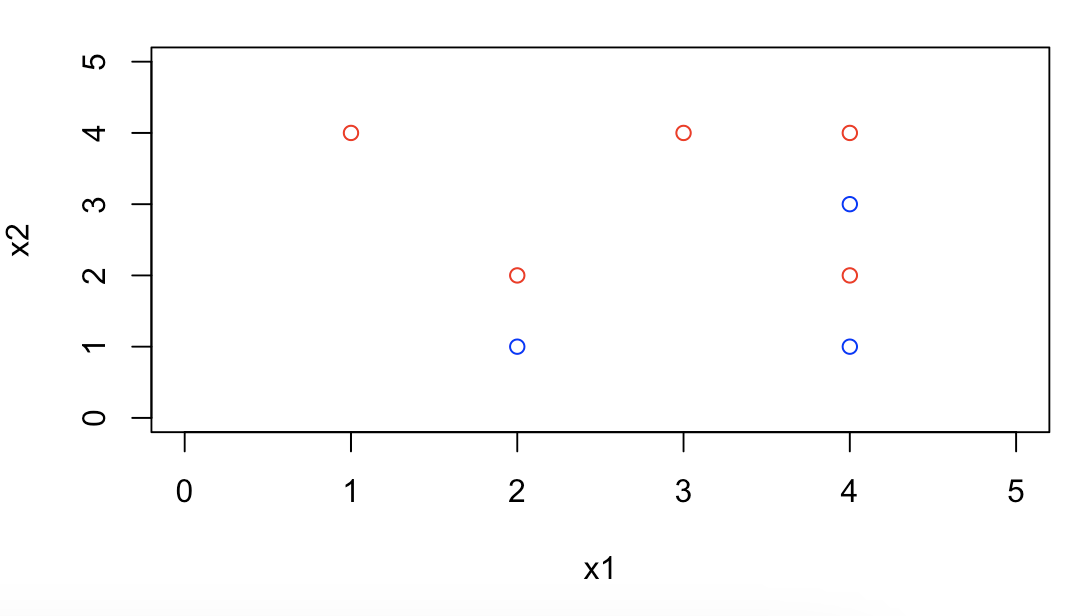

表达式:-X_1+X_2+0.8=0。

(h)

plot(x1, x2, col = colors, xlim = c(0, 5), ylim = c(0, 5)) points(c(4), c(2), col = c("red"))

二、应用题

8.4.8

(a)

# 8.(a) library(ISLR) attach(Carseats) set.seed(1) train = sample(dim(Carseats)[1], dim(Carseats)[1]/2) Carseats.train = Carseats[train, ] Carseats.test = Carseats[-train, ]

(b)

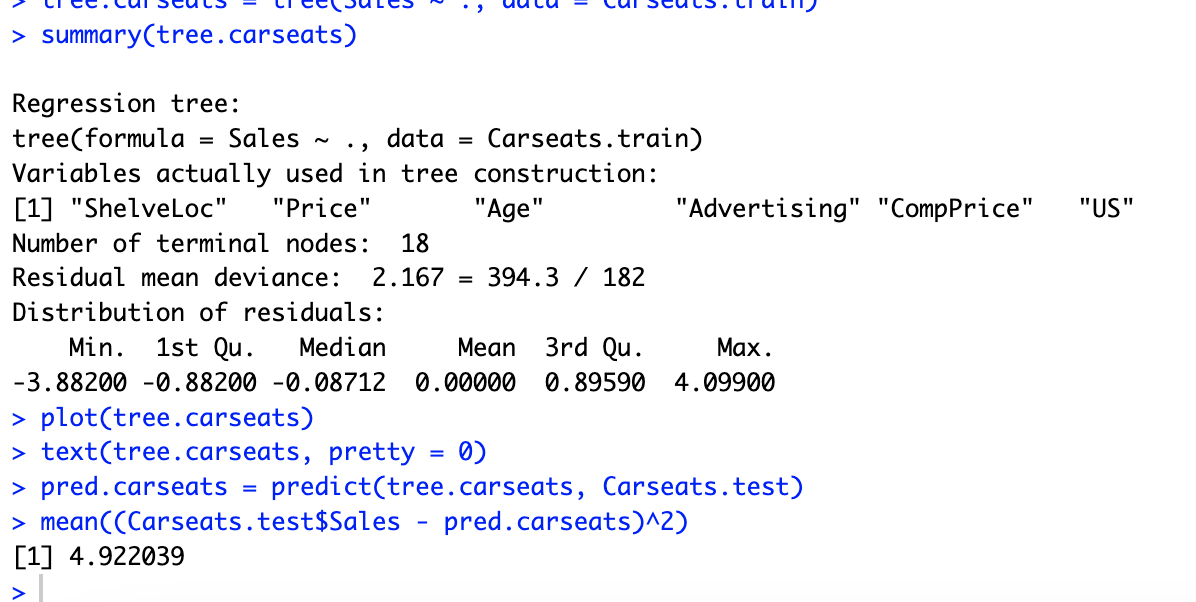

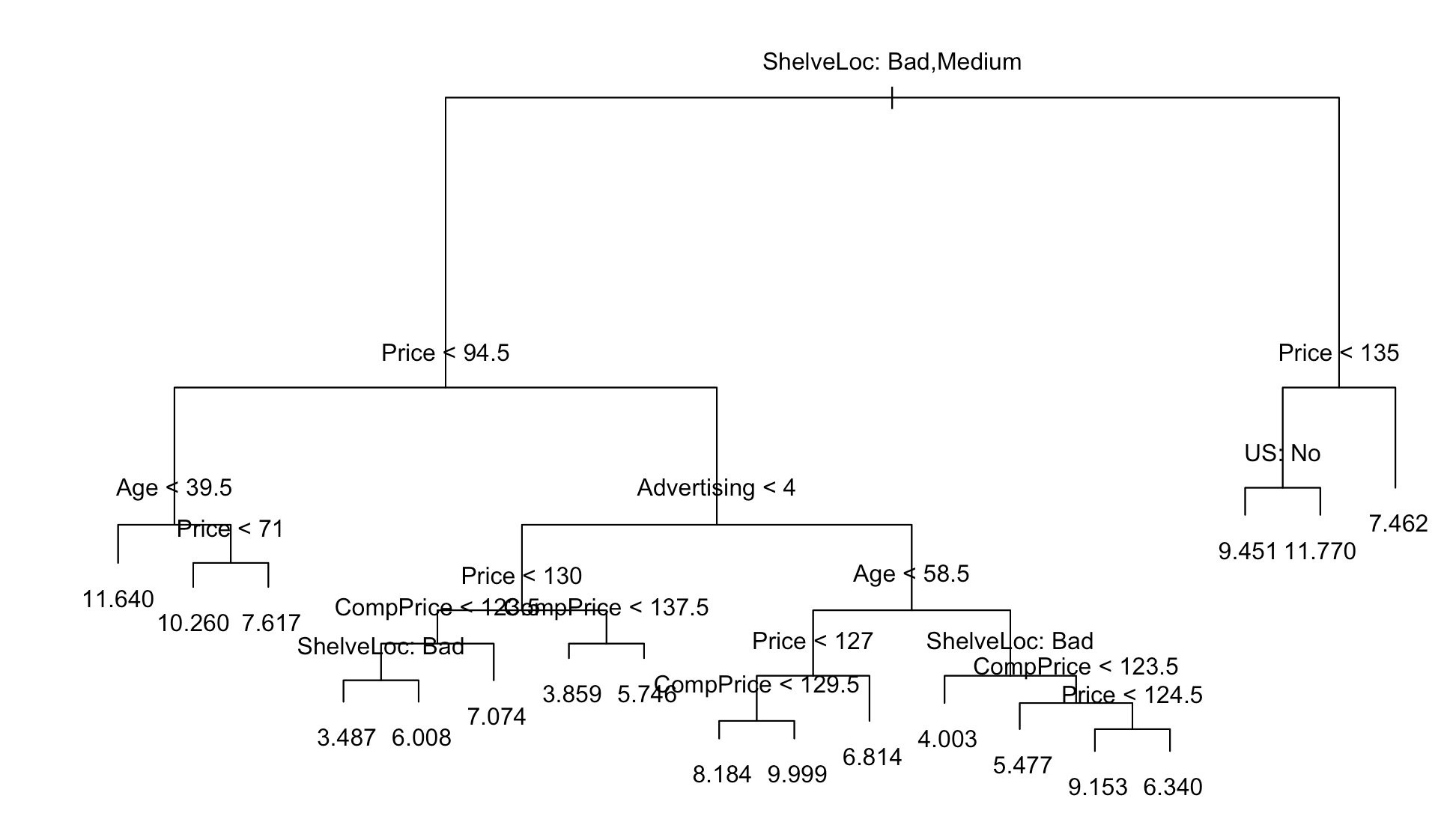

# 8.(b) library(tree) tree.carseats = tree(Sales ~ ., data = Carseats.train) summary(tree.carseats) plot(tree.carseats) text(tree.carseats, pretty = 0) pred.carseats = predict(tree.carseats, Carseats.test) mean((Carseats.test$Sales - pred.carseats)^2) ## 可以看出较为重要的变量为 Price,得到的测试错误率为 4.922039

(c)

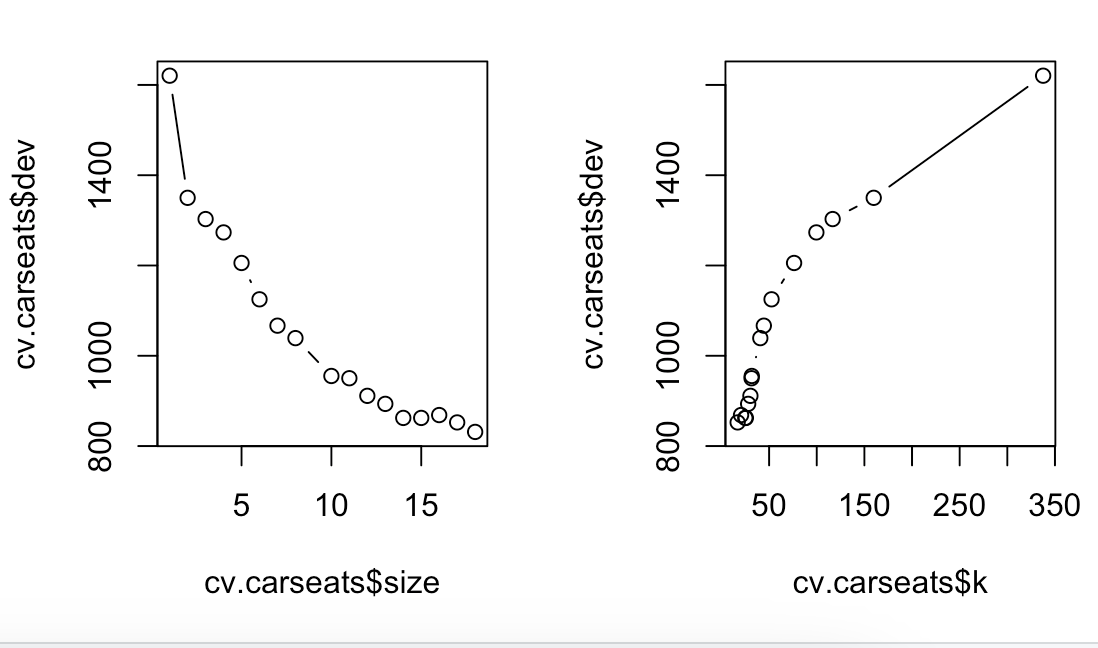

# 8.(c) cv.carseats = cv.tree(tree.carseats, FUN = prune.tree) par(mfrow = c(1, 2)) plot(cv.carseats$size, cv.carseats$dev, type = "b") plot(cv.carseats$k, cv.carseats$dev, type = "b") ## 可以观察得到剪枝后的回归树并不一定能够减小 MSE,相反,未剪枝的模型具有最小的 MSE。

(d)

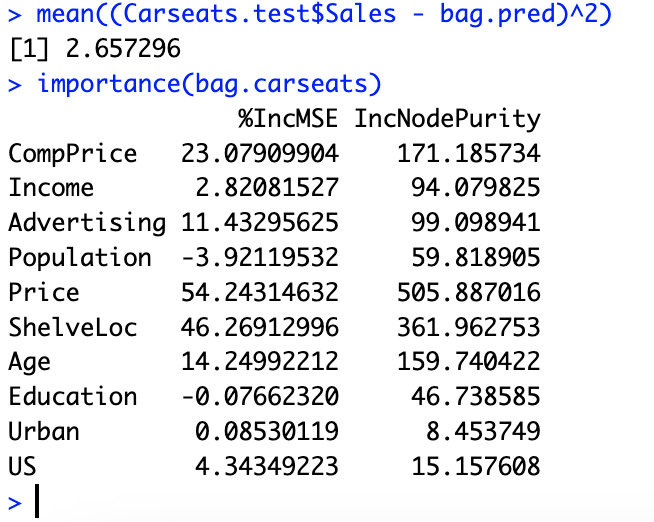

# 8.(d) library(randomForest) bag.carseats = randomForest(Sales ~ ., data = Carseats.train, mtry =10, ntree = 500, importance = T) bag.pred = predict(bag.carseats, Carseats.test) mean((Carseats.test$Sales - bag.pred)^2) importance(bag.carseats) ## 测试错误率为 2.622982。 ## 可以看出: 较为重要的变量有 Price、 ShelveLoc、 CompPrice 和 Age 等等。

(e)

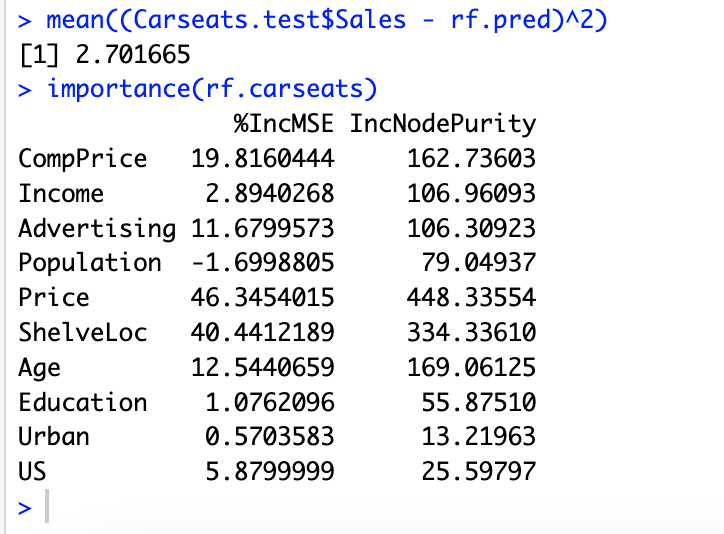

# 8.(e) rf.carseats = randomForest(Sales ~ ., data = Carseats.train, mtry = 5,ntree = 500,importance = T) rf.pred = predict(rf.carseats, Carseats.test) mean((Carseats.test$Sales - rf.pred)^2) importance(rf.carseats) ## 测试错误率为 2.70217。 ##较为重要的变量有 Price、ShelveLoc、CompPrice 和 Age 等等。

完整代码

# 8.(a) library(ISLR) attach(Carseats) set.seed(1) train = sample(dim(Carseats)[1], dim(Carseats)[1]/2) Carseats.train = Carseats[train, ] Carseats.test = Carseats[-train, ] # 8.(b) library(tree) tree.carseats = tree(Sales ~ ., data = Carseats.train) summary(tree.carseats) plot(tree.carseats) text(tree.carseats, pretty = 0) pred.carseats = predict(tree.carseats, Carseats.test) mean((Carseats.test$Sales - pred.carseats)^2) ## 可以看出较为重要的变量为 Price,得到的测试错误率为 4.922039 # 8.(c) cv.carseats = cv.tree(tree.carseats, FUN = prune.tree) par(mfrow = c(1, 2)) plot(cv.carseats$size, cv.carseats$dev, type = "b") plot(cv.carseats$k, cv.carseats$dev, type = "b") ## 可以观察得到剪枝后的回归树并不一定能够减小 MSE,相反,未剪枝的模型具有最小的 MSE。 # 8.(d) library(randomForest) bag.carseats = randomForest(Sales ~ ., data = Carseats.train, mtry =10, ntree = 500, importance = T) bag.pred = predict(bag.carseats, Carseats.test) mean((Carseats.test$Sales - bag.pred)^2) importance(bag.carseats) ## 测试错误率为 2.622982。 ## 可以看出: 较为重要的变量有 Price、 ShelveLoc、 CompPrice 和 Age 等等。 # 8.(e) rf.carseats = randomForest(Sales ~ ., data = Carseats.train, mtry = 5,ntree = 500,importance = T) rf.pred = predict(rf.carseats, Carseats.test) mean((Carseats.test$Sales - rf.pred)^2) importance(rf.carseats) ## 测试错误率为 2.70217。 ##较为重要的变量有 Price、ShelveLoc、CompPrice 和 Age 等等。

8.4.9

(a)

# 9.(a) library(ISLR) attach(OJ) set.seed(1013) train = sample(dim(OJ)[1], 800) OJ.train = OJ[train, ] OJ.test = OJ[-train, ]

(b)

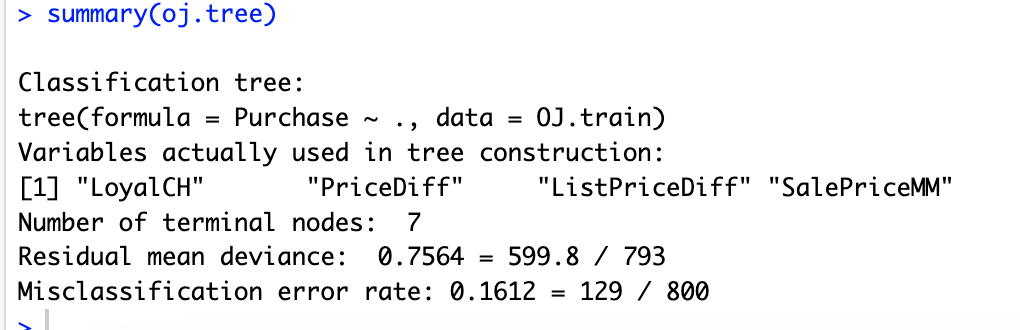

# 9.(b) library(tree) oj.tree = tree(Purchase ~., data = OJ.train) summary(oj.tree)

(c)

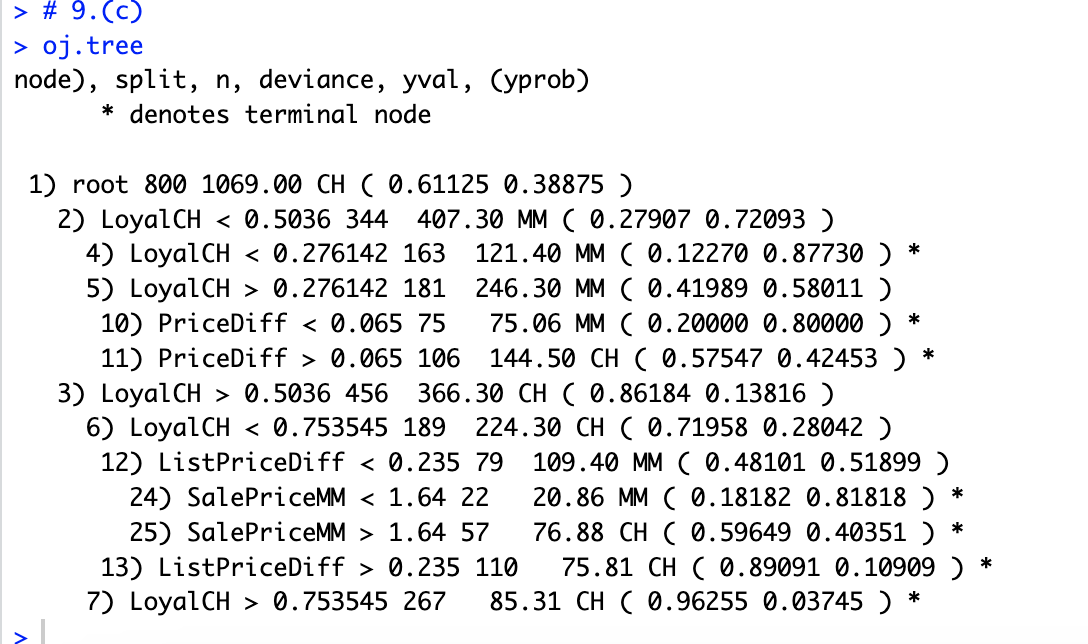

# 9.(c) oj.tree ## 以结点10作为分析:该结点以PriceDiff<0.065作为分割依据,其下共有75个数据 ## 所有点的偏差为75.06。该结点上的预测是Sales=MM。 ## 该节点中约有20%的数据认为Sales=CH,剩下的80%数据认为Sales=MM。

(d)

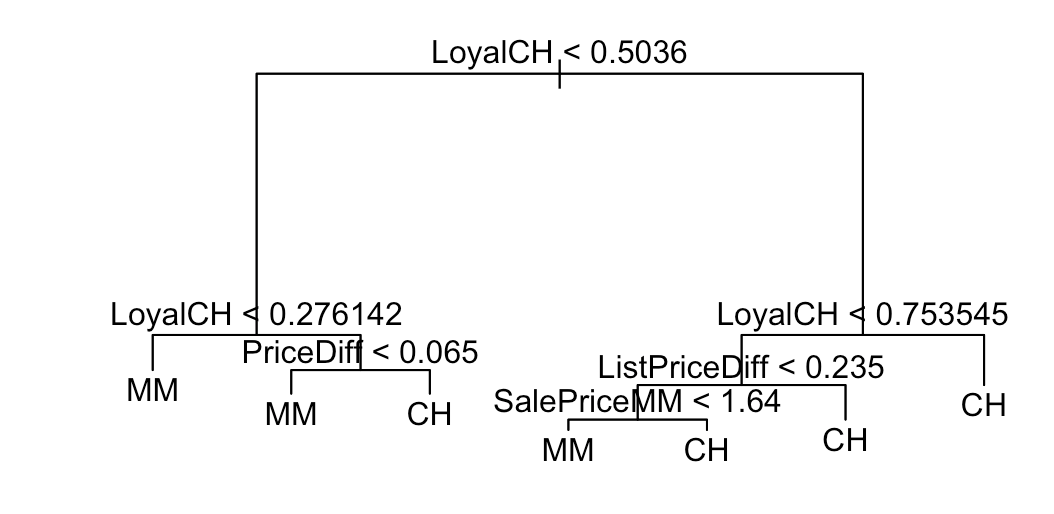

# 9.(d) par(mfrow=c(1,1)) plot(oj.tree) text(oj.tree, pretty = 0)

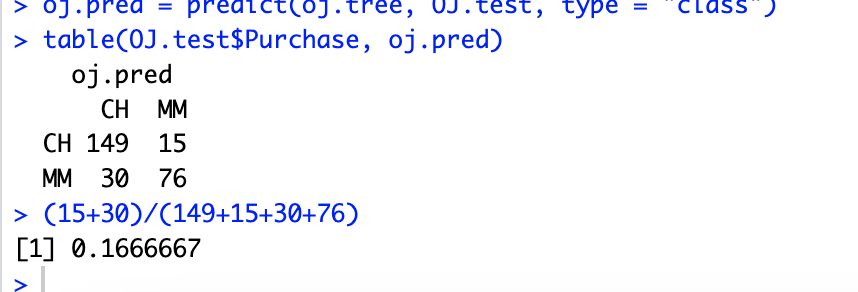

(e)

# 9.(e) oj.pred = predict(oj.tree, OJ.test, type = "class") table(OJ.test$Purchase, oj.pred) (15+30)/(149+15+30+76)

(f)

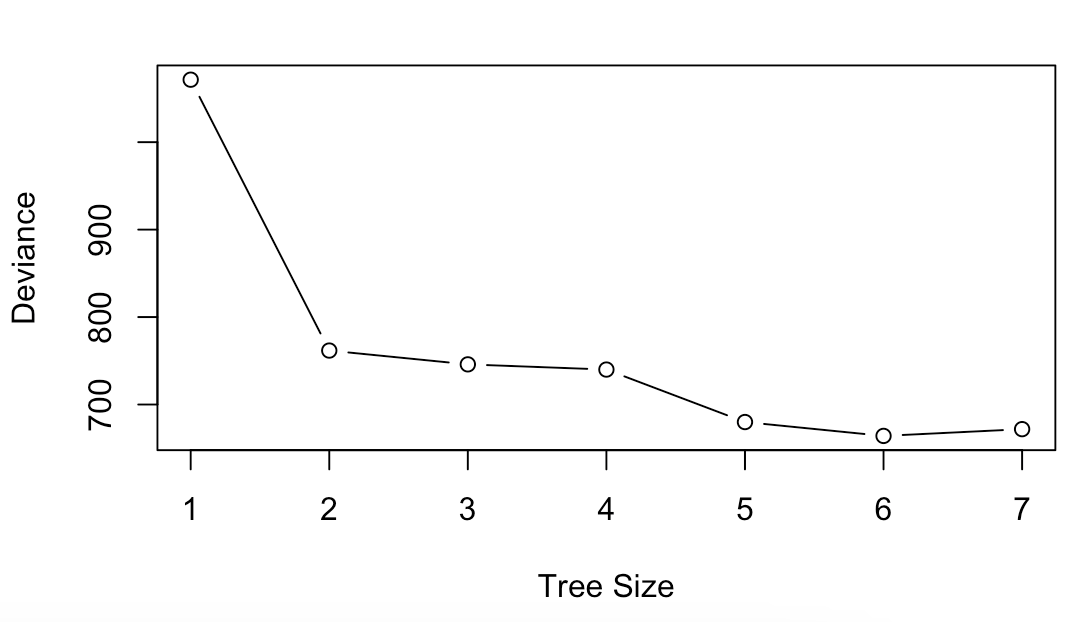

# 9.(f) cv.oj = cv.tree(oj.tree, FUN = prune.tree)(g)

# 9.(g) plot(cv.oj$size, cv.oj$dev, type = "b", xlab = "Tree Size", ylab = "Deviance")

(h)

# 9.(h) ## 可以看出:当 Size=6 的时候,利用交叉验证分类错误率最低(i)

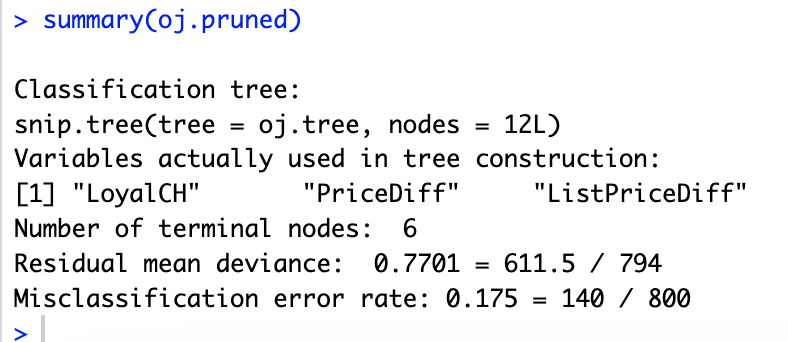

# 9.(i) oj.pruned = prune.tree(oj.tree, best = 6)(j)

# 9.(j) summary(oj.pruned)

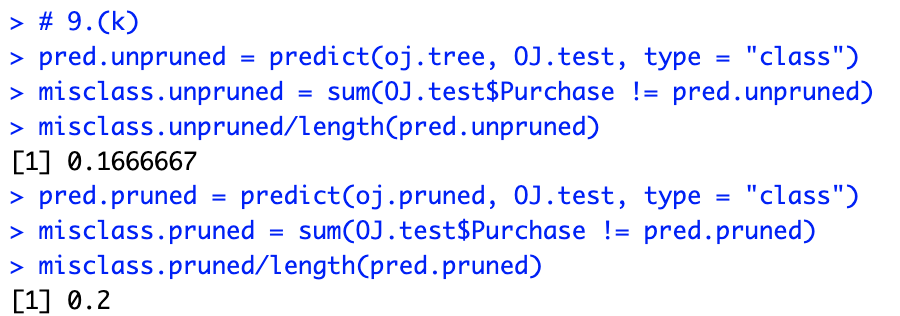

(k)

# 9.(k) pred.unpruned = predict(oj.tree, OJ.test, type = "class") misclass.unpruned = sum(OJ.test$Purchase != pred.unpruned) misclass.unpruned/length(pred.unpruned) pred.pruned = predict(oj.pruned, OJ.test, type = "class") misclass.pruned = sum(OJ.test$Purchase != pred.pruned) misclass.pruned/length(pred.pruned) ## 剪枝前后的测试错误率分别为 0.1666667 和 0.2, 因此剪枝之后的测试错误率更高

完整代码

# 9.(a) library(ISLR) attach(OJ) set.seed(1013) train = sample(dim(OJ)[1], 800) OJ.train = OJ[train, ] OJ.test = OJ[-train, ] # 9.(b) library(tree) oj.tree = tree(Purchase ~., data = OJ.train) summary(oj.tree) # 9.(c) oj.tree ## 以结点10作为分析:该结点以PriceDiff<0.065作为分割依据,其下共有75个数据 ## 所有点的偏差为75.06。该结点上的预测是Sales=MM。 ## 该节点中约有20%的数据认为Sales=CH,剩下的80%数据认为Sales=MM。 # 9.(d) par(mfrow=c(1,1)) plot(oj.tree) text(oj.tree, pretty = 0) # 9.(e) oj.pred = predict(oj.tree, OJ.test, type = "class") table(OJ.test$Purchase, oj.pred) (15+30)/(149+15+30+76) # 9.(f) cv.oj = cv.tree(oj.tree, FUN = prune.tree) # 9.(g) plot(cv.oj$size, cv.oj$dev, type = "b", xlab = "Tree Size", ylab = "Deviance") # 9.(h) ## 可以看出:当 Size=6 的时候,利用交叉验证分类错误率最低 # 9.(i) oj.pruned = prune.tree(oj.tree, best = 6) # 9.(j) summary(oj.pruned) # 9.(k) pred.unpruned = predict(oj.tree, OJ.test, type = "class") misclass.unpruned = sum(OJ.test$Purchase != pred.unpruned) misclass.unpruned/length(pred.unpruned) pred.pruned = predict(oj.pruned, OJ.test, type = "class") misclass.pruned = sum(OJ.test$Purchase != pred.pruned) misclass.pruned/length(pred.pruned) ## 剪枝前后的测试错误率分别为 0.1666667 和 0.2, 因此剪枝之后的测试错误率更高

8.4.10

(a)

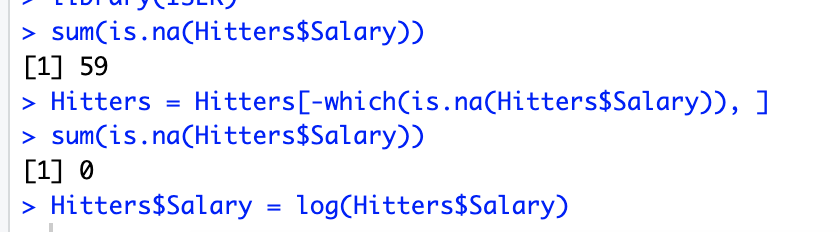

# 10.(a) library(ISLR) sum(is.na(Hitters$Salary)) Hitters = Hitters[-which(is.na(Hitters$Salary)), ] sum(is.na(Hitters$Salary)) Hitters$Salary = log(Hitters$Salary)

(b)

# 10.(b) train = 1:200 Hitters.train = Hitters[train, ] Hitters.test = Hitters[-train, ]

(c)

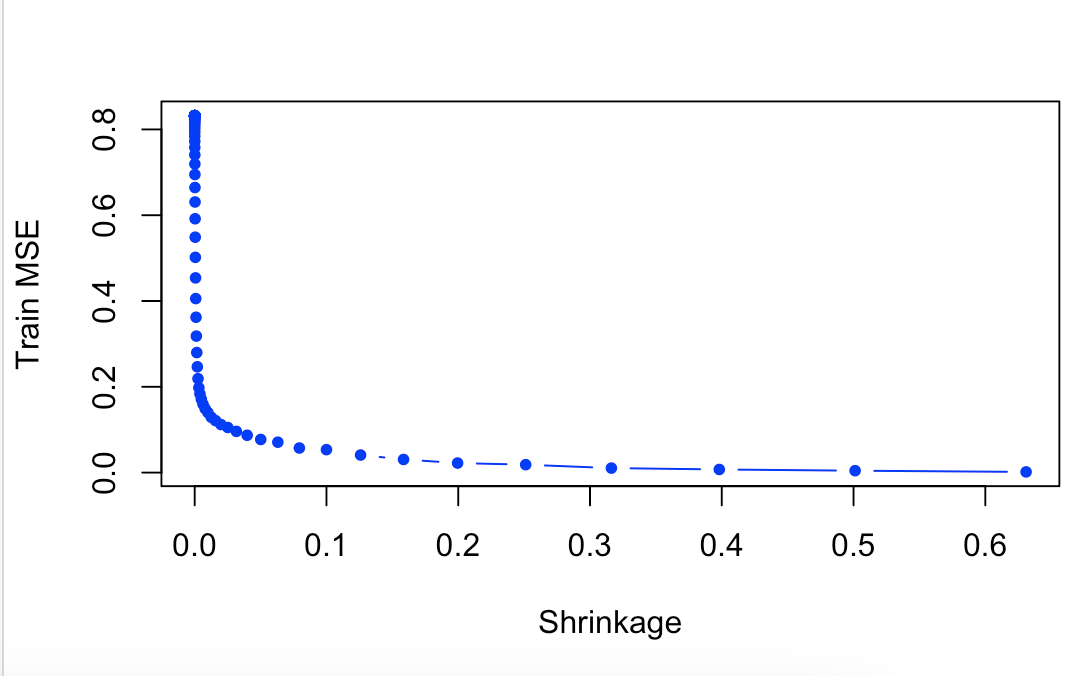

# 10.(c) library(gbm) set.seed(103) pows = seq(-10, -0.2, by = 0.1) lambdas = 10^pows length.lambdas = length(lambdas) train.errors = rep(NA, length.lambdas) test.errors = rep(NA, length.lambdas) for (i in 1:length.lambdas) { boost.hitters = gbm(Salary ~ ., data = Hitters.train, distribution = "gaussian", n.trees = 1000, shrinkage = lambdas[i]) train.pred = predict(boost.hitters, Hitters.train, n.trees = 1000) test.pred = predict(boost.hitters, Hitters.test, n.trees = 1000) train.errors[i] = mean((Hitters.train$Salary - train.pred)^2) test.errors[i] = mean((Hitters.test$Salary - test.pred)^2) } plot(lambdas, train.errors, type = "b", col = "blue", xlab = "Shrinkage", ylab = "Train MSE", pch = 20)

(d)

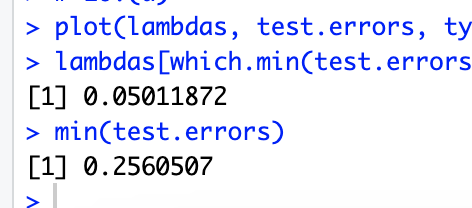

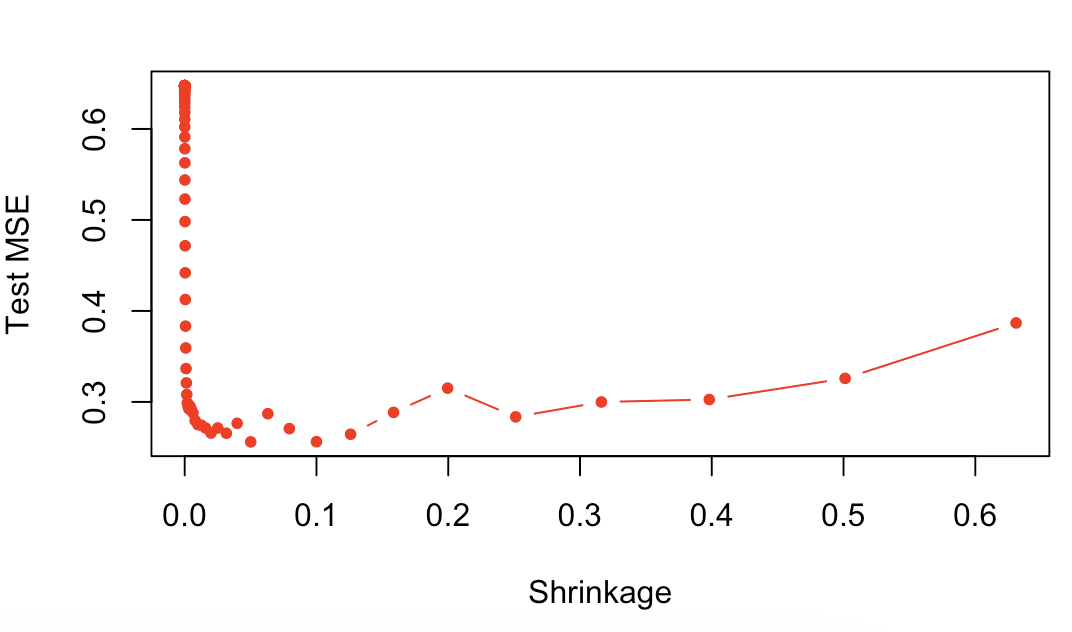

# 10.(d) plot(lambdas, test.errors, type = "b", xlab = "Shrinkage", ylab = "Test MSE", col = "red", pch = 20) lambdas[which.min(test.errors)] min(test.errors)

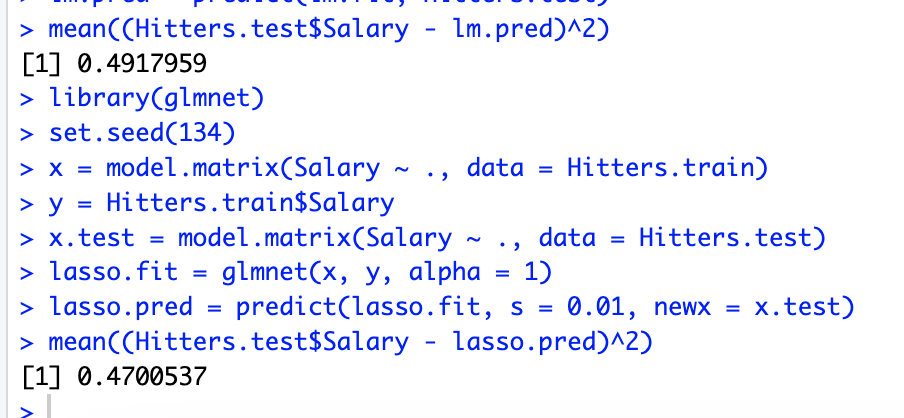

(e)

# 10.(e) lm.fit = lm(Salary ~ ., data = Hitters.train) lm.pred = predict(lm.fit, Hitters.test) mean((Hitters.test$Salary - lm.pred)^2) library(glmnet) set.seed(134) x = model.matrix(Salary ~ ., data = Hitters.train) y = Hitters.train$Salary x.test = model.matrix(Salary ~ ., data = Hitters.test) lasso.fit = glmnet(x, y, alpha = 1) lasso.pred = predict(lasso.fit, s = 0.01, newx = x.test) mean((Hitters.test$Salary - lasso.pred)^2) ## 相较于使用提升法的树模型来说,误差都相对较高

(f)

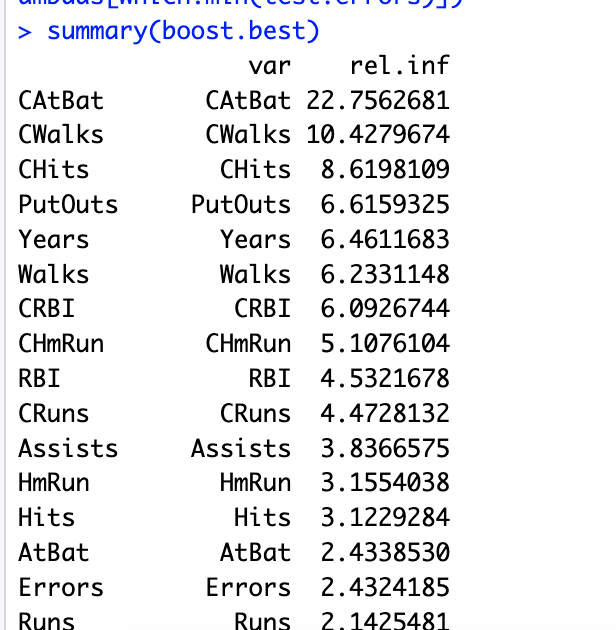

# 10.(f) boost.best = gbm(Salary ~ ., data = Hitters.train, distribution = "gaussian", n.trees = 1000, shrinkage = lambdas[which.min(test.errors)]) summary(boost.best) ## CAtBat、CWalks 和 Chits 是最重要的三个变量

(g)

# 10.(g) library(randomForest) set.seed(21) rf.hitters = randomForest(Salary ~ ., data = Hitters.train, ntree = 500, mtry = 19) rf.pred = predict(rf.hitters, Hitters.test) mean((Hitters.test$Salary - rf.pred)^2)

完整代码

# 10.(a) library(ISLR) sum(is.na(Hitters$Salary)) Hitters = Hitters[-which(is.na(Hitters$Salary)), ] sum(is.na(Hitters$Salary)) Hitters$Salary = log(Hitters$Salary) # 10.(b) train = 1:200 Hitters.train = Hitters[train, ] Hitters.test = Hitters[-train, ] # 10.(c) library(gbm) set.seed(103) pows = seq(-10, -0.2, by = 0.1) lambdas = 10^pows length.lambdas = length(lambdas) train.errors = rep(NA, length.lambdas) test.errors = rep(NA, length.lambdas) for (i in 1:length.lambdas) { boost.hitters = gbm(Salary ~ ., data = Hitters.train, distribution = "gaussian", n.trees = 1000, shrinkage = lambdas[i]) train.pred = predict(boost.hitters, Hitters.train, n.trees = 1000) test.pred = predict(boost.hitters, Hitters.test, n.trees = 1000) train.errors[i] = mean((Hitters.train$Salary - train.pred)^2) test.errors[i] = mean((Hitters.test$Salary - test.pred)^2) } plot(lambdas, train.errors, type = "b", col = "blue", xlab = "Shrinkage", ylab = "Train MSE", pch = 20) # 10.(d) plot(lambdas, test.errors, type = "b", xlab = "Shrinkage", ylab = "Test MSE", col = "red", pch = 20) lambdas[which.min(test.errors)] min(test.errors) # 10.(e) lm.fit = lm(Salary ~ ., data = Hitters.train) lm.pred = predict(lm.fit, Hitters.test) mean((Hitters.test$Salary - lm.pred)^2) library(glmnet) set.seed(134) x = model.matrix(Salary ~ ., data = Hitters.train) y = Hitters.train$Salary x.test = model.matrix(Salary ~ ., data = Hitters.test) lasso.fit = glmnet(x, y, alpha = 1) lasso.pred = predict(lasso.fit, s = 0.01, newx = x.test) mean((Hitters.test$Salary - lasso.pred)^2) ## 相较于使用提升法的树模型来说,误差都相对较高 # 10.(f) boost.best = gbm(Salary ~ ., data = Hitters.train, distribution = "gaussian", n.trees = 1000, shrinkage = lambdas[which.min(test.errors)]) summary(boost.best) ## CAtBat、CWalks 和 Chits 是最重要的三个变量 # 10.(g) library(randomForest) set.seed(21) rf.hitters = randomForest(Salary ~ ., data = Hitters.train, ntree = 500, mtry = 19) rf.pred = predict(rf.hitters, Hitters.test) mean((Hitters.test$Salary - rf.pred)^2)

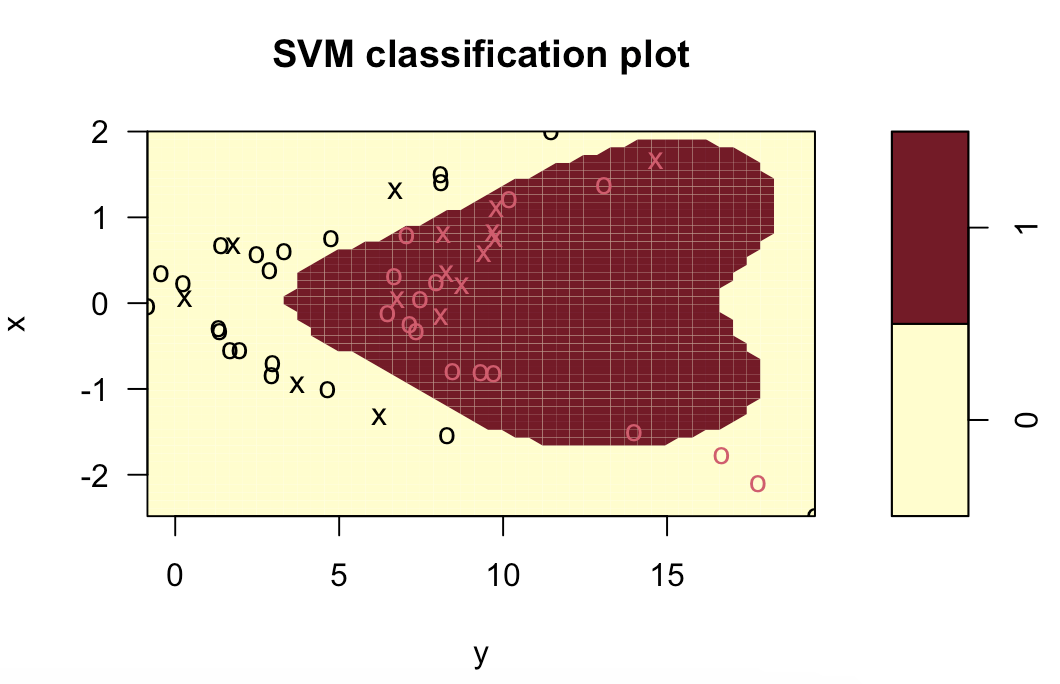

9.7.4

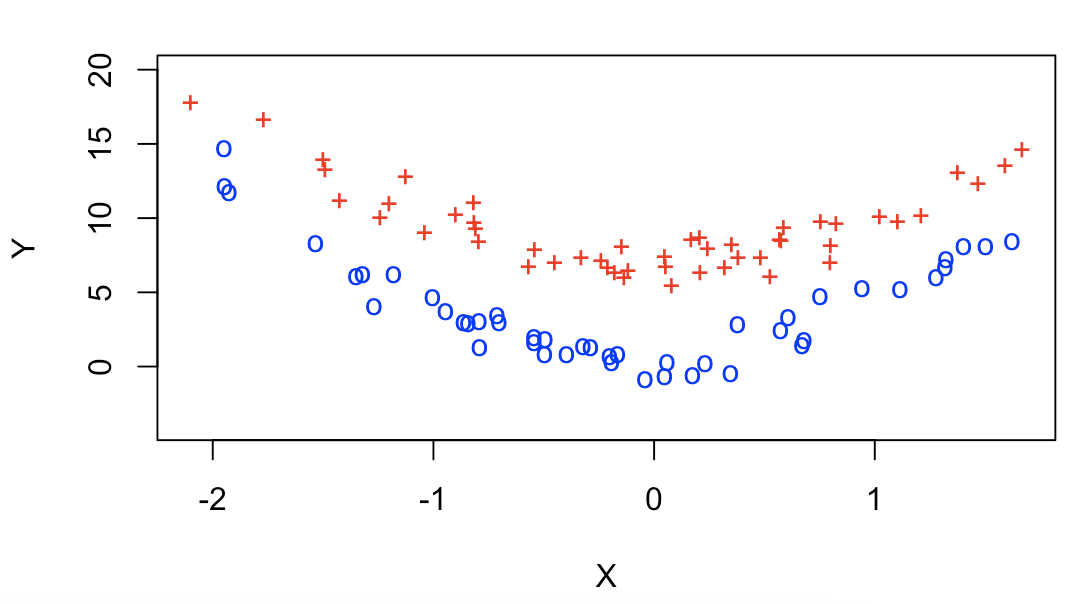

set.seed(131)

x = rnorm(100)

y = 3 * x^2 + 4 + rnorm(100)

train = sample(100, 50)

y[train] = y[train] + 3

y[-train] = y[-train] - 3

plot(x[train], y[train], pch="+", lwd=4, col="red", ylim=c(-4, 20),

xlab="X", ylab="Y")

points(x[-train], y[-train], pch="o", lwd=4, col="blue")

训练集表现:

set.seed(315)

z = rep(0, 100)

z[train] = 1

final.train = c(sample(train, 25), sample(setdiff(1:100, train), 25))

data.train = data.frame(x=x[final.train], y=y[final.train], z=as.factor(z[final.train]))

data.test = data.frame(x=x[-final.train], y=y[-final.train], z=as.factor(z[-final.train]))

library(e1071)

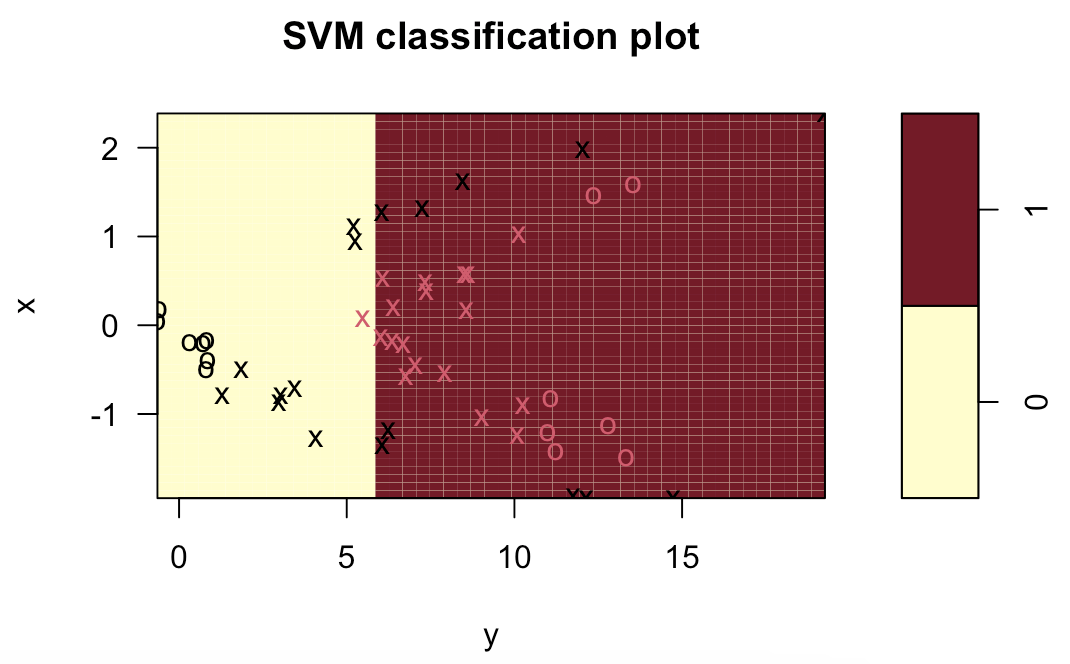

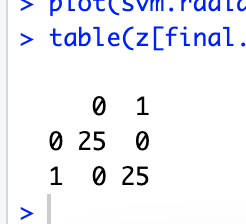

svm.linear = svm(z~., data=data.train, kernel="linear", cost=10)

plot(svm.linear, data.train)

table(z[final.train], predict(svm.linear, data.train))

(10+1)/(15+10+1+24)

set.seed(32545)

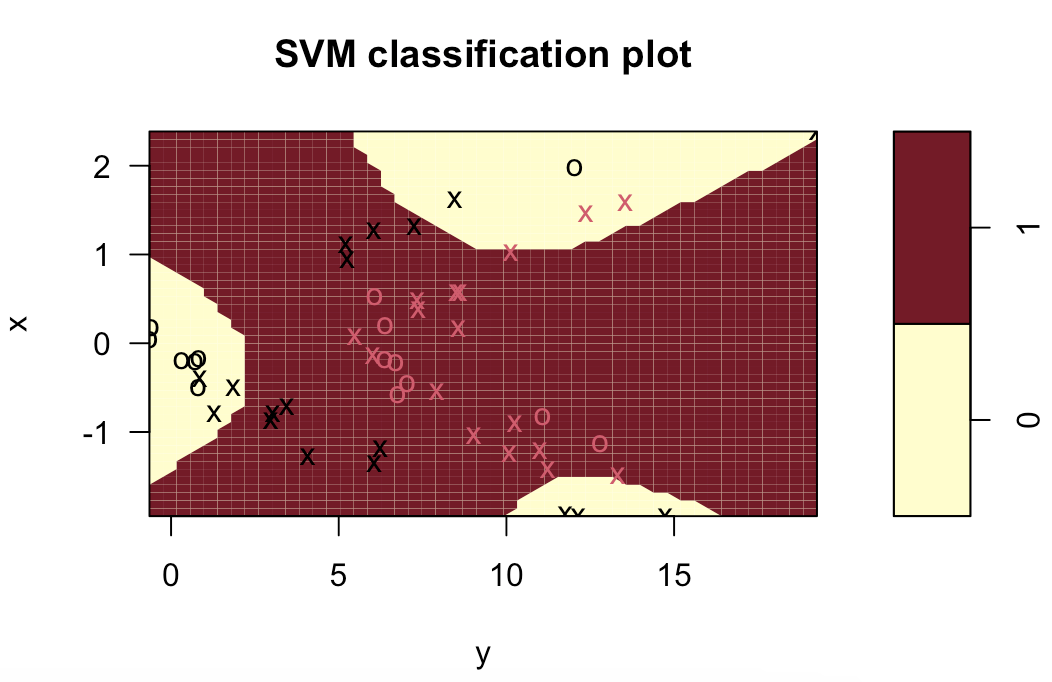

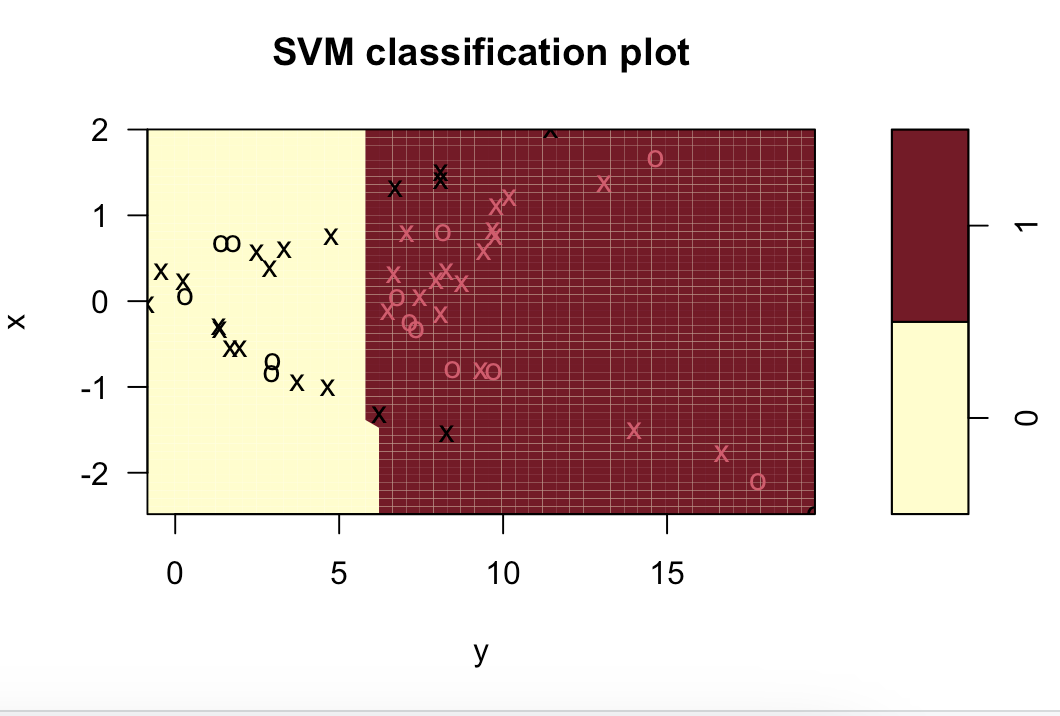

svm.poly = svm(z~., data=data.train, kernel="polynomial", cost=10)

plot(svm.poly, data.train)

table(z[final.train], predict(svm.poly, data.train))

(10+2)/(15+10+2+23)

set.seed(996)

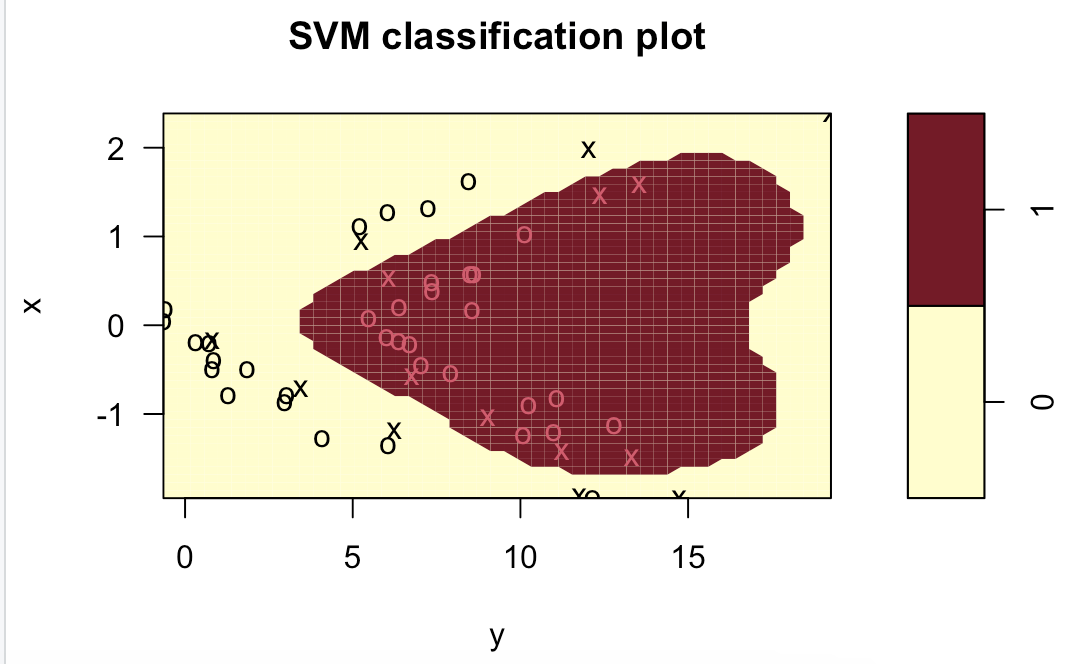

svm.radial = svm(z~., data=data.train, kernel="radial", gamma=1, cost=10)

plot(svm.radial, data.train)

table(z[final.train], predict(svm.radial, data.train))

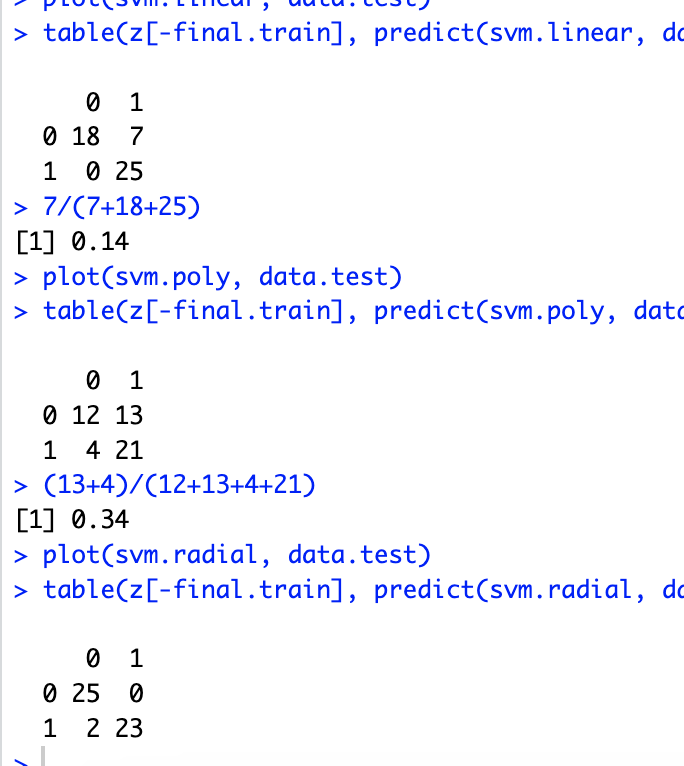

在测试集:

plot(svm.linear, data.test)

table(z[-final.train], predict(svm.linear, data.test))

7/(7+18+25)

plot(svm.poly, data.test)

table(z[-final.train], predict(svm.poly, data.test))

(13+4)/(12+13+4+21)

plot(svm.radial, data.test)

table(z[-final.train], predict(svm.radial, data.test))

完整代码

set.seed(131) x = rnorm(100) y = 3 * x^2 + 4 + rnorm(100) train = sample(100, 50) y[train] = y[train] + 3 y[-train] = y[-train] - 3 plot(x[train], y[train], pch="+", lwd=4, col="red", ylim=c(-4, 20), xlab="X", ylab="Y") points(x[-train], y[-train], pch="o", lwd=4, col="blue") set.seed(315) z = rep(0, 100) z[train] = 1 final.train = c(sample(train, 25), sample(setdiff(1:100, train), 25)) data.train = data.frame(x=x[final.train], y=y[final.train], z=as.factor(z[final.train])) data.test = data.frame(x=x[-final.train], y=y[-final.train], z=as.factor(z[-final.train])) library(e1071) svm.linear = svm(z~., data=data.train, kernel="linear", cost=10) plot(svm.linear, data.train) table(z[final.train], predict(svm.linear, data.train)) (10+1)/(15+10+1+24) set.seed(32545) svm.poly = svm(z~., data=data.train, kernel="polynomial", cost=10) plot(svm.poly, data.train) table(z[final.train], predict(svm.poly, data.train)) (10+2)/(15+10+2+23) set.seed(996) svm.radial = svm(z~., data=data.train, kernel="radial", gamma=1, cost=10) plot(svm.radial, data.train) table(z[final.train], predict(svm.radial, data.train)) plot(svm.linear, data.test) table(z[-final.train], predict(svm.linear, data.test)) 7/(7+18+25) plot(svm.poly, data.test) table(z[-final.train], predict(svm.poly, data.test)) (13+4)/(12+13+4+21) plot(svm.radial, data.test) table(z[-final.train], predict(svm.radial, data.test))

9.7.5

(a)

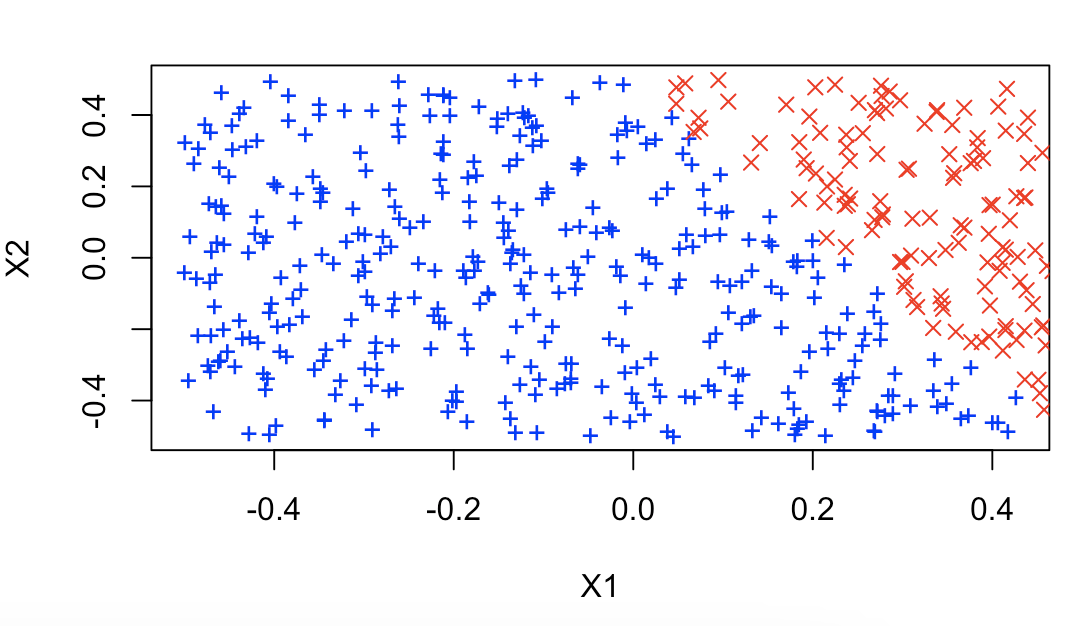

# 5.(a) set.seed(421) x1 = runif(500) - 0.5 x2 = runif(500) - 0.5 y = 1 * (x1^2 - x2^2 > 0)

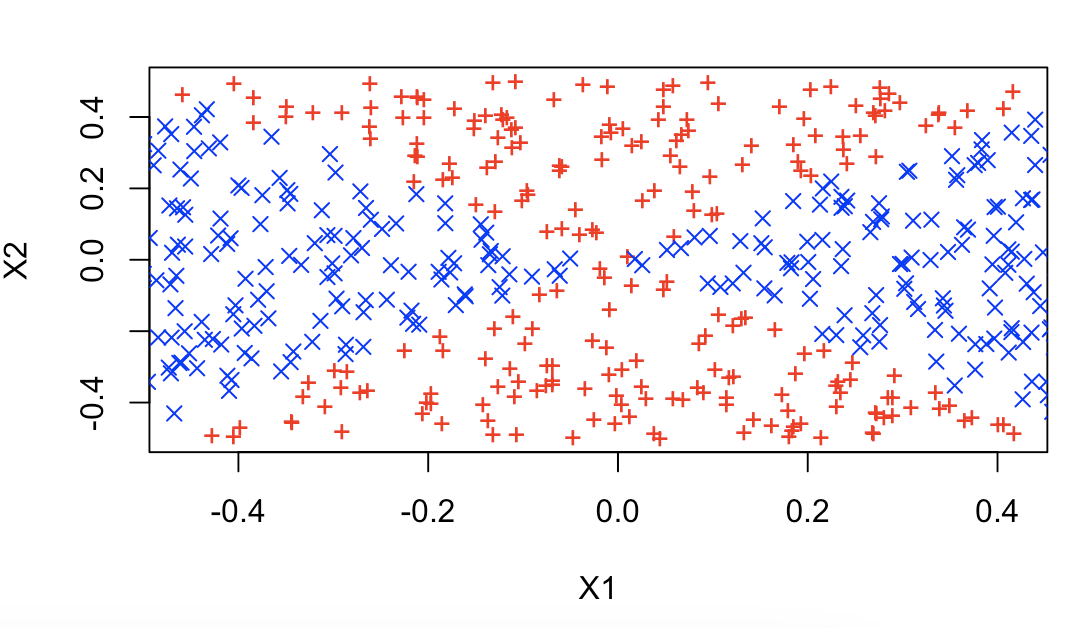

(b)

# 5.(b) plot(x1[y == 0], x2[y == 0], col = "red", xlab = "X1", ylab = "X2", pch = "+") points(x1[y == 1], x2[y == 1], col = "blue", pch = 4)

(c)

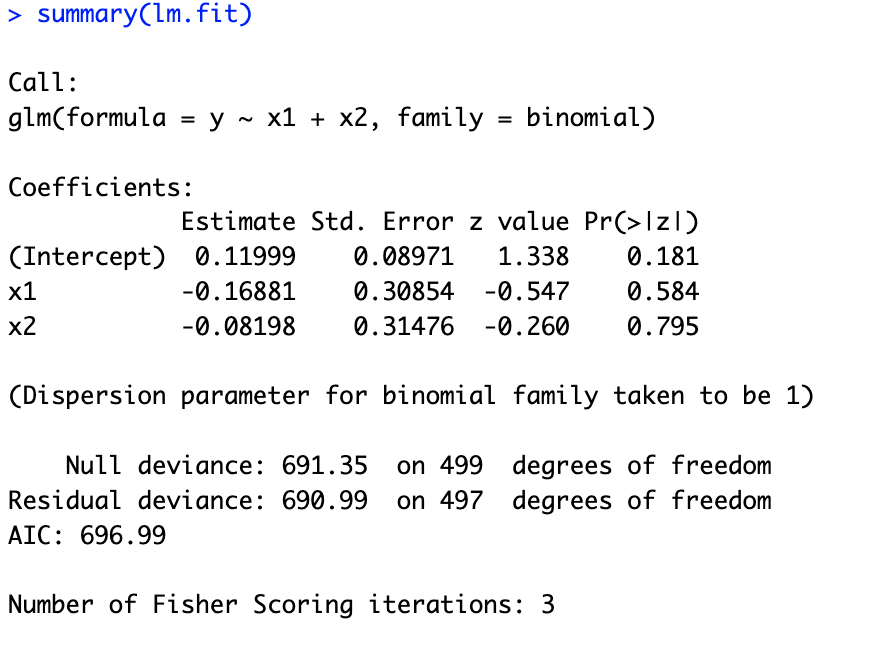

# 5.(c) lm.fit = glm(y ~ x1 + x2, family = binomial) summary(lm.fit) ## p 值较大,和 x1、x2 之间存在的关系并不显著。

(d)

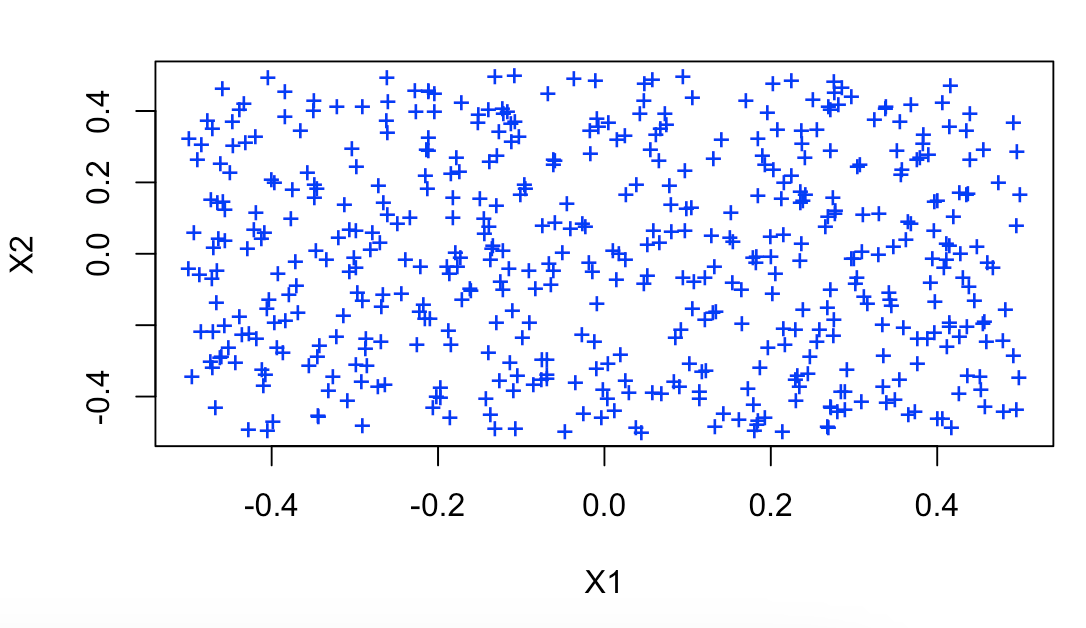

# 5.(d) data = data.frame(x1 = x1, x2 = x2, y = y) lm.prob = predict(lm.fit, data, type = "response") lm.pred = ifelse(lm.prob > 0.52, 1, 0) data.pos = data[lm.pred == 1, ] data.neg = data[lm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4) ## 在给定模型和概率阈值为 0.5 的情况下, 无法显示决策边界。 我们将概率阈值移至 0.52,以显示有意义的决策边界。

(e)

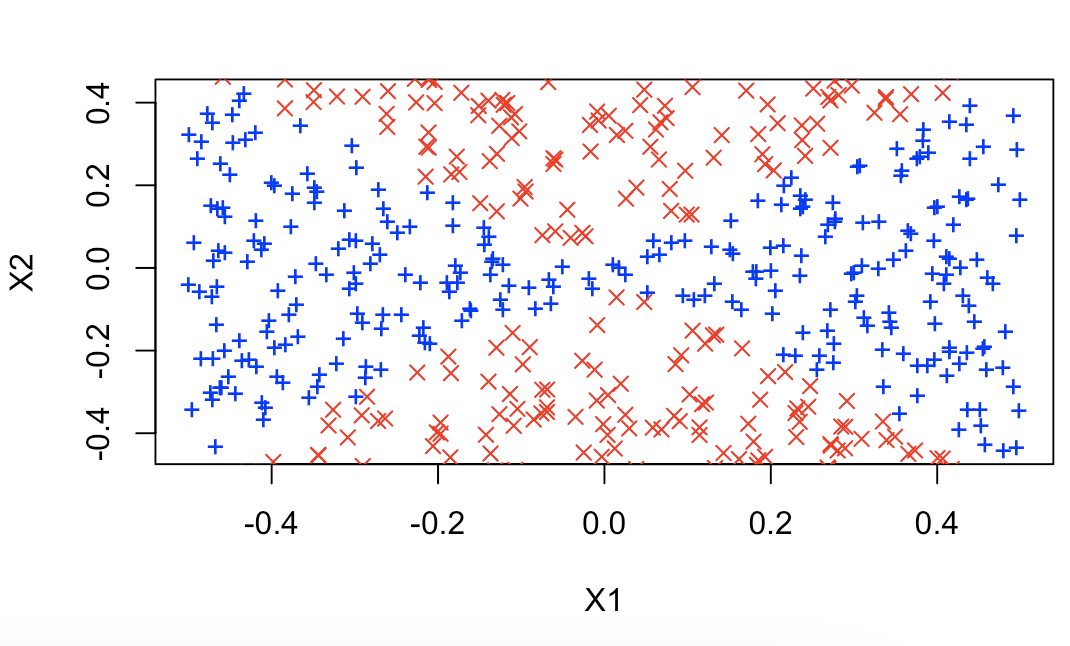

# 5.(e) lm.fit = glm(y ~ poly(x1, 2) + poly(x2, 2) + I(x1 * x2), data = data, family = binomial)(f)

# 5.(f) lm.prob = predict(lm.fit, data, type = "response") lm.pred = ifelse(lm.prob > 0.5, 1, 0) data.pos = data[lm.pred == 1, ] data.neg = data[lm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4)

(g)

# 5.(g) library(e1071) svm.fit = svm(as.factor(y) ~ x1 + x2, data, kernel = "linear", cost = 0.1) svm.pred = predict(svm.fit, data) data.pos = data[svm.pred == 1, ] data.neg = data[svm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4) ## 当我们使用线性核函数进行预测时,无法将各个类别之间区分开

(h)

# 5.(h) svm.fit = svm(as.factor(y) ~ x1 + x2, data, gamma = 1) svm.pred = predict(svm.fit, data) data.pos = data[svm.pred == 1, ] data.neg = data[svm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4)

(i)

# 5.(i) ## 这个实验展示了一个重要的观点:使用非线性核的 SVM 在识别非线性决策边界方面具有显著优势。 ## 相比之下,没有交互项的逻辑回归模型和仅使用线性核的 SVM 难以捕捉到这样的边界。 ## 虽然在逻辑回归中加入交互项可以提升模型的拟合能力,使其与径向基核的 SVM 相媲美, ## 但这需要手动选择和调整交互项,这在特征数量众多的情况下会非常耗时且复杂。 ## 相比之下,径向基核 SVM 只需调整一个参数——gamma ## 并且这个参数可以通过交叉验证来优化,使得模型选择过程更加简便和高效。完整代码

# 5.(a) set.seed(421) x1 = runif(500) - 0.5 x2 = runif(500) - 0.5 y = 1 * (x1^2 - x2^2 > 0) # 5.(b) plot(x1[y == 0], x2[y == 0], col = "red", xlab = "X1", ylab = "X2", pch = "+") points(x1[y == 1], x2[y == 1], col = "blue", pch = 4) # 5.(c) lm.fit = glm(y ~ x1 + x2, family = binomial) summary(lm.fit) ## p 值较大,和 x1、x2 之间存在的关系并不显著。 # 5.(d) data = data.frame(x1 = x1, x2 = x2, y = y) lm.prob = predict(lm.fit, data, type = "response") lm.pred = ifelse(lm.prob > 0.52, 1, 0) data.pos = data[lm.pred == 1, ] data.neg = data[lm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4) ## 在给定模型和概率阈值为 0.5 的情况下, 无法显示决策边界。 我们将概率阈值移至 0.52,以显示有意义的决策边界。 # 5.(e) lm.fit = glm(y ~ poly(x1, 2) + poly(x2, 2) + I(x1 * x2), data = data, family = binomial) # 5.(f) lm.prob = predict(lm.fit, data, type = "response") lm.pred = ifelse(lm.prob > 0.5, 1, 0) data.pos = data[lm.pred == 1, ] data.neg = data[lm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4) # 5.(g) library(e1071) svm.fit = svm(as.factor(y) ~ x1 + x2, data, kernel = "linear", cost = 0.1) svm.pred = predict(svm.fit, data) data.pos = data[svm.pred == 1, ] data.neg = data[svm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4) ## 当我们使用线性核函数进行预测时,无法将各个类别之间区分开 # 5.(h) svm.fit = svm(as.factor(y) ~ x1 + x2, data, gamma = 1) svm.pred = predict(svm.fit, data) data.pos = data[svm.pred == 1, ] data.neg = data[svm.pred == 0, ] plot(data.pos$x1, data.pos$x2, col = "blue", xlab = "X1", ylab = "X2", pch = "+") points(data.neg$x1, data.neg$x2, col = "red", pch = 4) # 5.(i) ## 这个实验展示了一个重要的观点:使用非线性核的 SVM 在识别非线性决策边界方面具有显著优势。 ## 相比之下,没有交互项的逻辑回归模型和仅使用线性核的 SVM 难以捕捉到这样的边界。 ## 虽然在逻辑回归中加入交互项可以提升模型的拟合能力,使其与径向基核的 SVM 相媲美, ## 但这需要手动选择和调整交互项,这在特征数量众多的情况下会非常耗时且复杂。 ## 相比之下,径向基核 SVM 只需调整一个参数——gamma ## 并且这个参数可以通过交叉验证来优化,使得模型选择过程更加简便和高效。

9.7.6

(a)

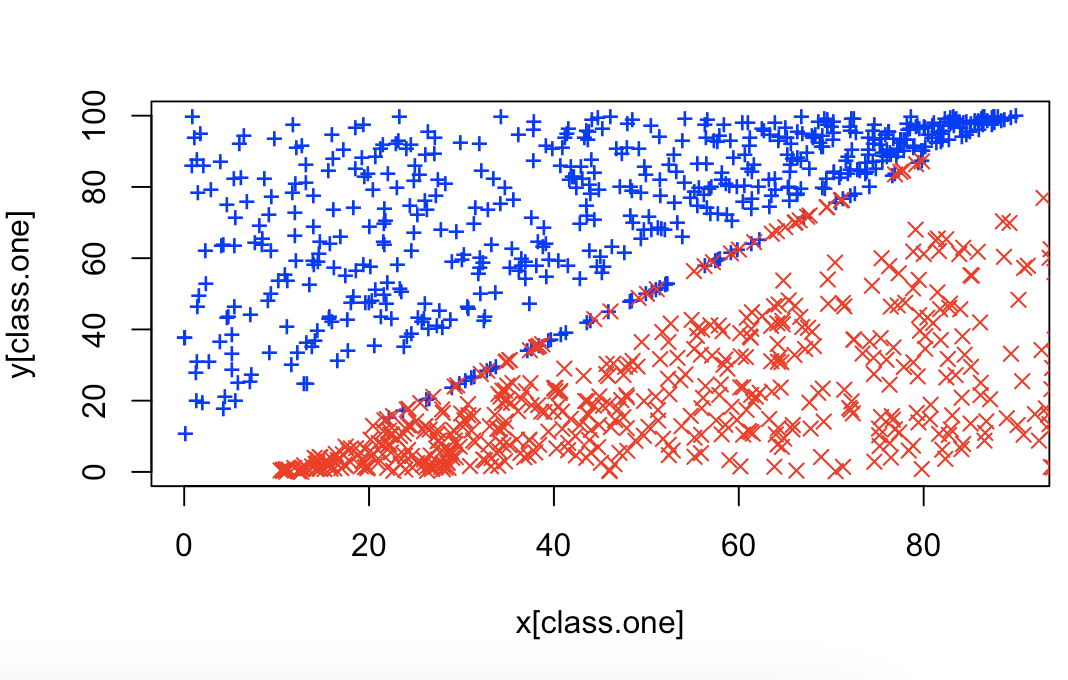

# 6.(a) set.seed(3154) x.one = runif(500, 0, 90) y.one = runif(500, x.one + 10, 100) x.one.noise = runif(50, 20, 80) y.one.noise = 5/4 * (x.one.noise - 10) + 0.1 x.zero = runif(500, 10, 100) y.zero = runif(500, 0, x.zero - 10) x.zero.noise = runif(50, 20, 80) y.zero.noise = 5/4 * (x.zero.noise - 10) - 0.1 class.one = seq(1, 550) x = c(x.one, x.one.noise, x.zero, x.zero.noise) y = c(y.one, y.one.noise, y.zero, y.zero.noise) plot(x[class.one], y[class.one], col = "blue", pch = "+", ylim = c(0, 100)) points(x[-class.one], y[-class.one], col = "red", pch = 4) ## 分界:5x–4y–50 = 0

(b)

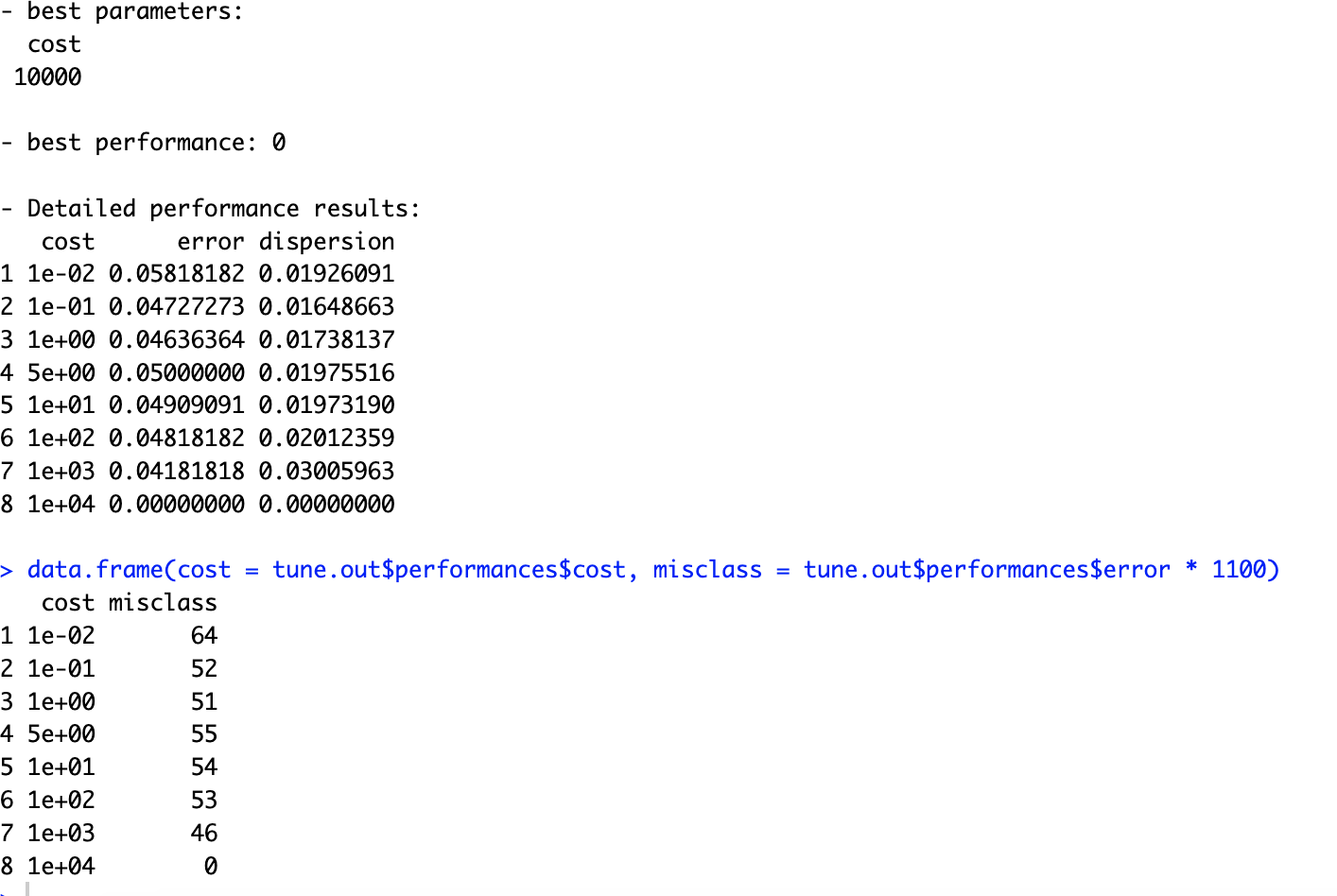

# 6.(b) library(e1071) set.seed(555) z = rep(0, 1100) z[class.one] = 1 data = data.frame(x = x, y = y, z = z) tune.out = tune(svm, as.factor(z) ~ ., data = data, kernel = "linear", ranges = list(cost = c(0.01, 0.1, 1, 5, 10, 100, 1000, 10000))) summary(tune.out) data.frame(cost = tune.out$performances$cost, misclass = tune.out$performances$error * 1100) ## 当 cost=10000 时,所有的点都能够被正确分类。

(c)

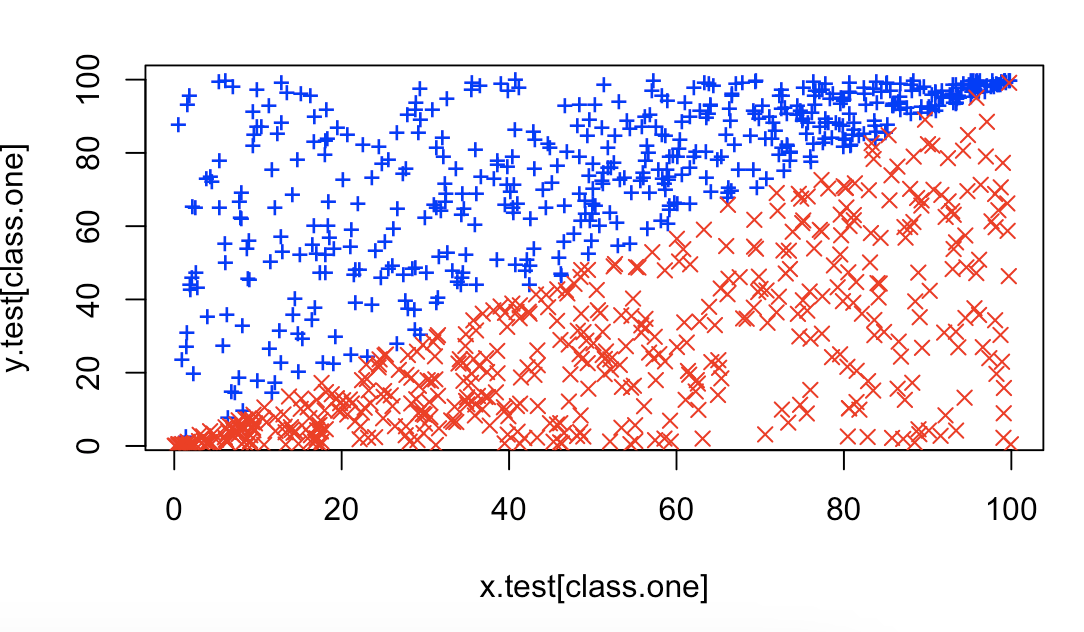

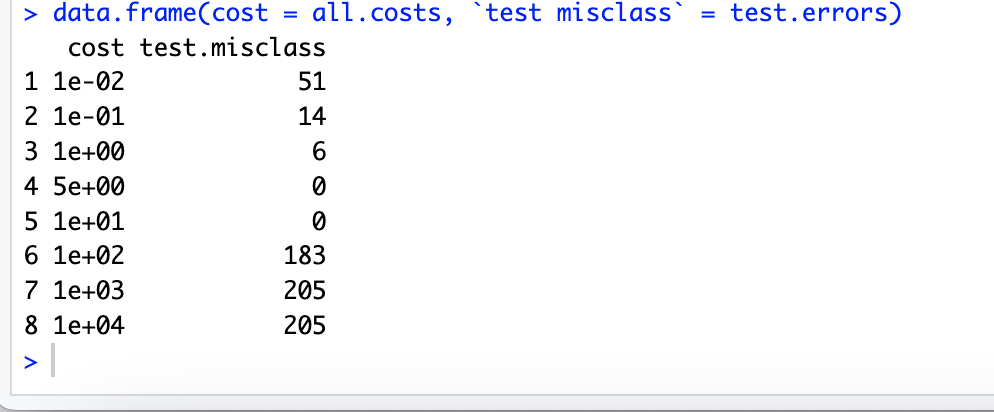

# 6.(c) set.seed(1111) x.test = runif(1000, 0, 100) class.one = sample(1000, 500) y.test = rep(NA, 1000) for (i in class.one) { y.test[i] = runif(1, x.test[i], 100) } for (i in setdiff(1:1000, class.one)) { y.test[i] = runif(1, 0, x.test[i]) } plot(x.test[class.one], y.test[class.one], col = "blue", pch = "+") points(x.test[-class.one], y.test[-class.one], col = "red", pch = 4) set.seed(30012) z.test = rep(0, 1000) z.test[class.one] = 1 all.costs = c(0.01, 0.1, 1, 5, 10, 100, 1000, 10000) test.errors = rep(NA, 8) data.test = data.frame(x = x.test, y = y.test, z = z.test) for (i in 1:length(all.costs)) { svm.fit = svm(as.factor(z) ~ ., data = data, kernel = "linear", cost = all.costs[i]) svm.predict = predict(svm.fit, data.test) test.errors[i] = sum(svm.predict != data.test$z) } data.frame(cost = all.costs, `test misclass` = test.errors) ## 当 cost=5 或 cost=10 时,误分数目最少

(d)

# 6.(d) ## 观察到线性核的过拟合现象。当代价参数较大时,模型试图精确地对训练数据中的噪声点进行分类 ## 导致对训练数据的过度拟合。然而,当代价参数较小时,模型在噪声测试点上可能会犯一些错误 ## 但在测试数据上的表现却更加优异。完整代码

# 6.(a) set.seed(3154) x.one = runif(500, 0, 90) y.one = runif(500, x.one + 10, 100) x.one.noise = runif(50, 20, 80) y.one.noise = 5/4 * (x.one.noise - 10) + 0.1 x.zero = runif(500, 10, 100) y.zero = runif(500, 0, x.zero - 10) x.zero.noise = runif(50, 20, 80) y.zero.noise = 5/4 * (x.zero.noise - 10) - 0.1 class.one = seq(1, 550) x = c(x.one, x.one.noise, x.zero, x.zero.noise) y = c(y.one, y.one.noise, y.zero, y.zero.noise) plot(x[class.one], y[class.one], col = "blue", pch = "+", ylim = c(0, 100)) points(x[-class.one], y[-class.one], col = "red", pch = 4) ## 分界:5x–4y–50 = 0 # 6.(b) library(e1071) set.seed(555) z = rep(0, 1100) z[class.one] = 1 data = data.frame(x = x, y = y, z = z) tune.out = tune(svm, as.factor(z) ~ ., data = data, kernel = "linear", ranges = list(cost = c(0.01, 0.1, 1, 5, 10, 100, 1000, 10000))) summary(tune.out) data.frame(cost = tune.out$performances$cost, misclass = tune.out$performances$error * 1100) ## 当 cost=10000 时,所有的点都能够被正确分类。 # 6.(c) set.seed(1111) x.test = runif(1000, 0, 100) class.one = sample(1000, 500) y.test = rep(NA, 1000) for (i in class.one) { y.test[i] = runif(1, x.test[i], 100) } for (i in setdiff(1:1000, class.one)) { y.test[i] = runif(1, 0, x.test[i]) } plot(x.test[class.one], y.test[class.one], col = "blue", pch = "+") points(x.test[-class.one], y.test[-class.one], col = "red", pch = 4) set.seed(30012) z.test = rep(0, 1000) z.test[class.one] = 1 all.costs = c(0.01, 0.1, 1, 5, 10, 100, 1000, 10000) test.errors = rep(NA, 8) data.test = data.frame(x = x.test, y = y.test, z = z.test) for (i in 1:length(all.costs)) { svm.fit = svm(as.factor(z) ~ ., data = data, kernel = "linear", cost = all.costs[i]) svm.predict = predict(svm.fit, data.test) test.errors[i] = sum(svm.predict != data.test$z) } data.frame(cost = all.costs, `test misclass` = test.errors) ## 当 cost=5 或 cost=10 时,误分数目最少 # 6.(d) ## 观察到线性核的过拟合现象。当代价参数较大时,模型试图精确地对训练数据中的噪声点进行分类 ## 导致对训练数据的过度拟合。然而,当代价参数较小时,模型在噪声测试点上可能会犯一些错误 ## 但在测试数据上的表现却更加优异。

9.7.7

(a)

# 7.(a) library(ISLR) gas.med = median(Auto$mpg) new.var = ifelse(Auto$mpg > gas.med, 1, 0) Auto$mpglevel = as.factor(new.var)(b)

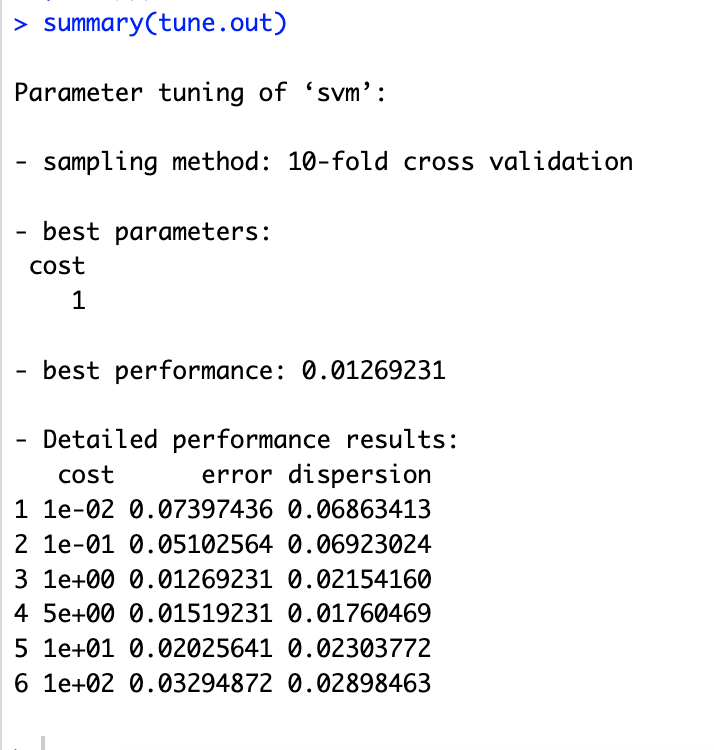

# 7.(b) library(e1071) set.seed(3255) tune.out = tune(svm, mpglevel ~ ., data = Auto, kernel = "linear", ranges = list(cost = c(0.01, 0.1, 1, 5, 10, 100))) summary(tune.out) ## 从结果可以看出:当采用 10 折交叉验证,当 cost=1 时,error 最小

(c)

# 7.(c) ### 多项式核函数 set.seed(21) tune.out = tune(svm, mpglevel ~ ., data = Auto, kernel = "polynomial", ranges = list(cost = c(0.1, 1, 5, 10), degree = c(2, 3, 4))) summary(tune.out) ## 当 cost=10,degree=2 时,error 最小。 ### 径向核函数 set.seed(463) tune.out = tune(svm, mpglevel ~ ., data = Auto, kernel = "radial", ranges = list(cost = c(0.1, 1, 5, 10), gamma = c(0.01, 0.1, 1, 5, 10, 100))) summary(tune.out) ## 当 cost=10,gamma=0.01 时,error 最小(d)

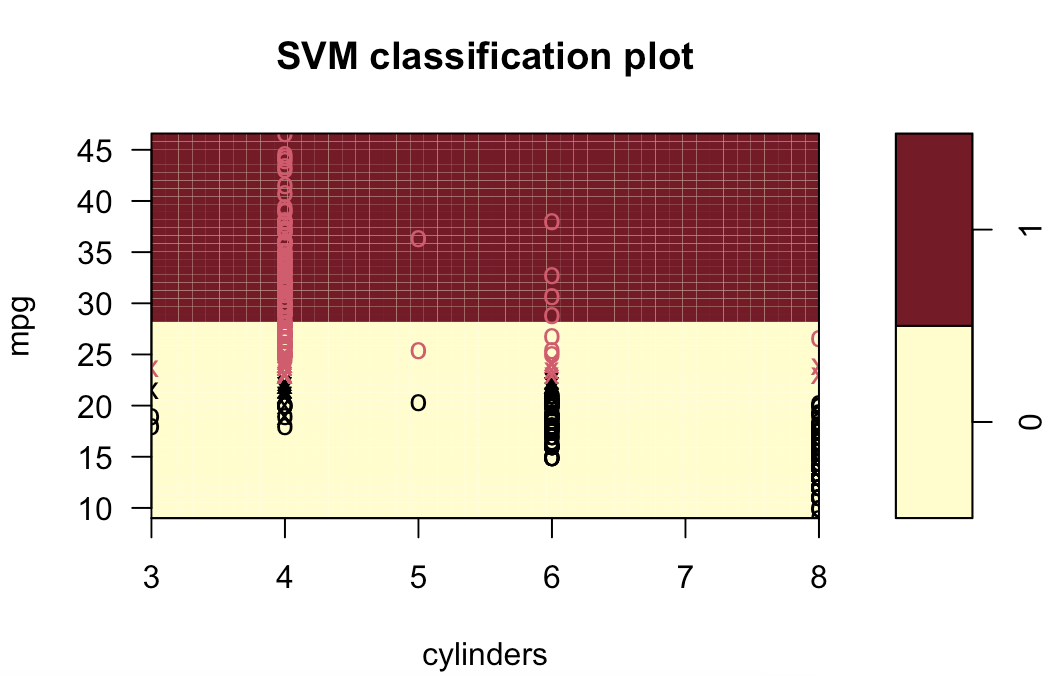

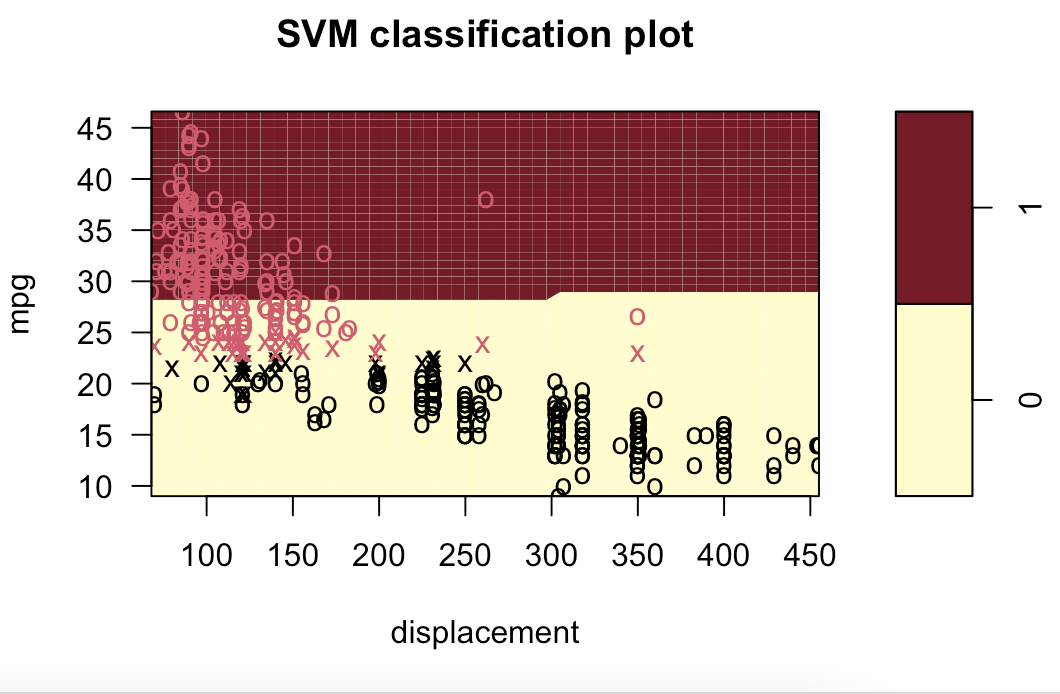

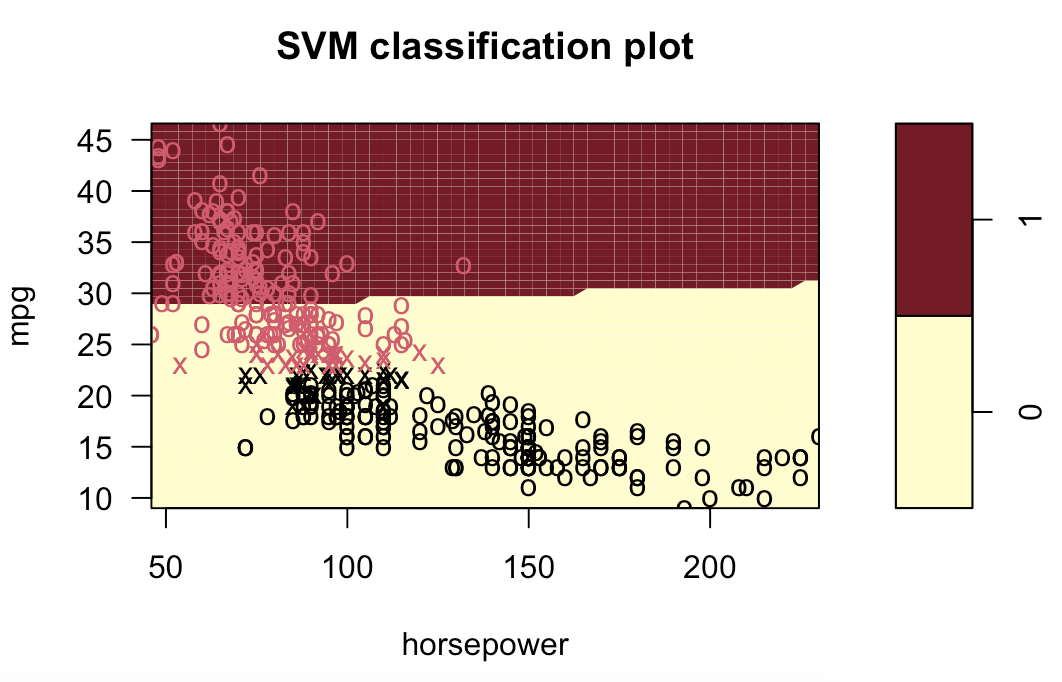

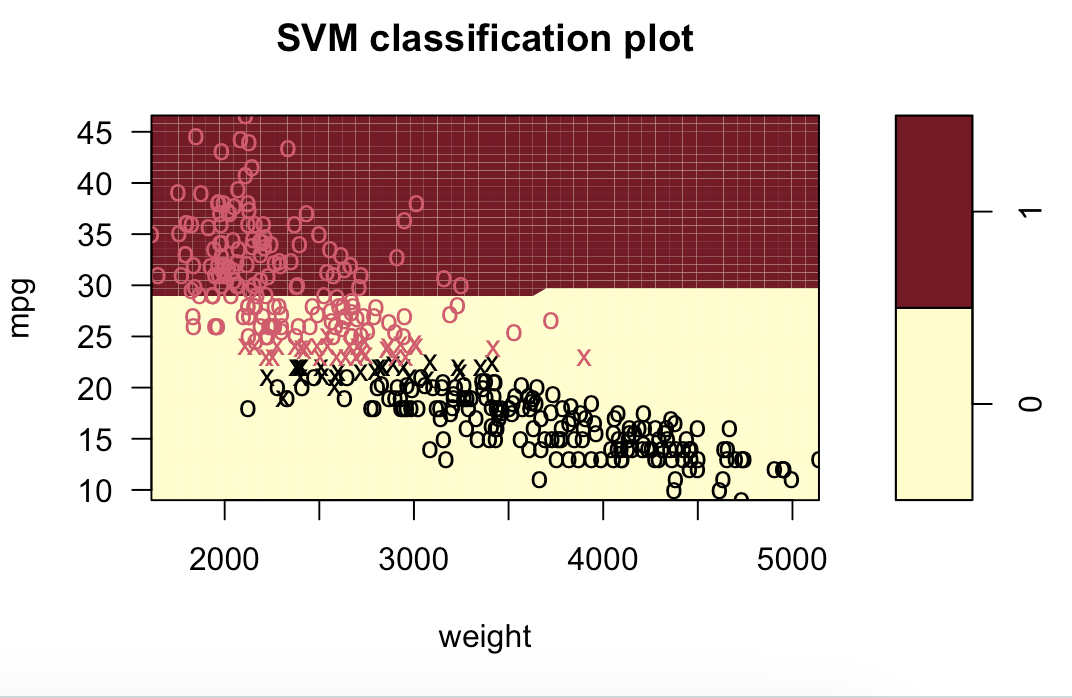

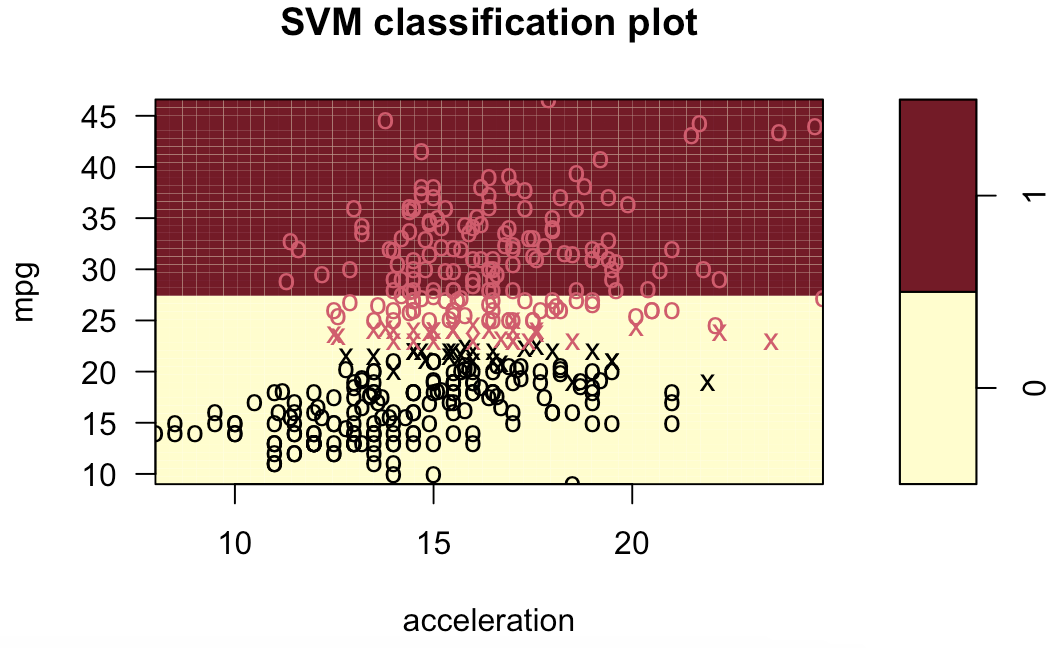

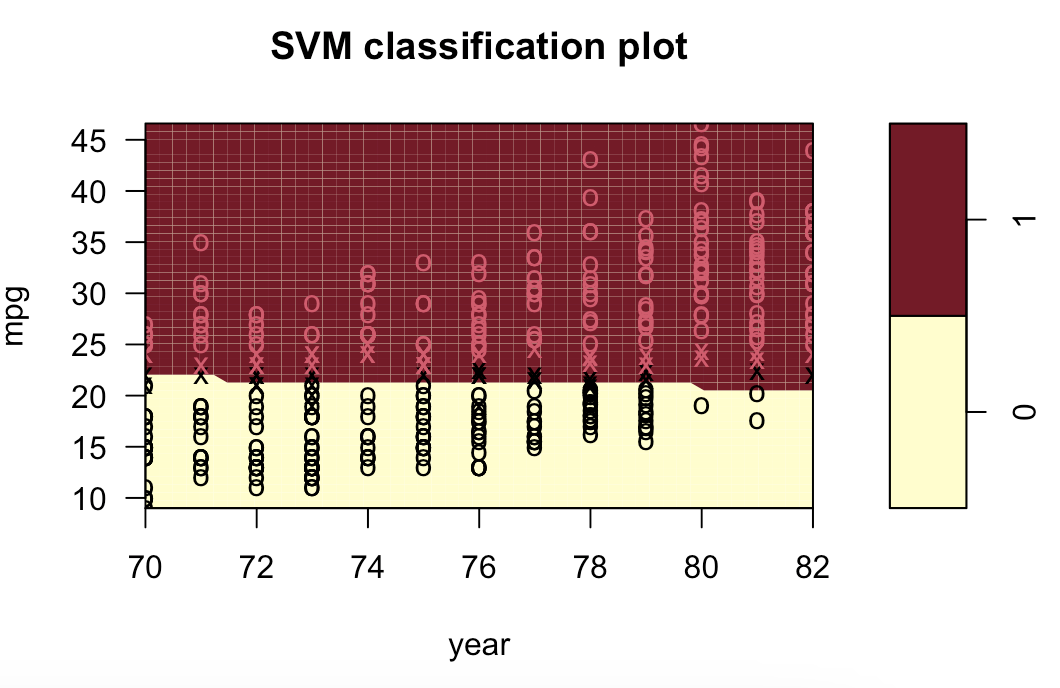

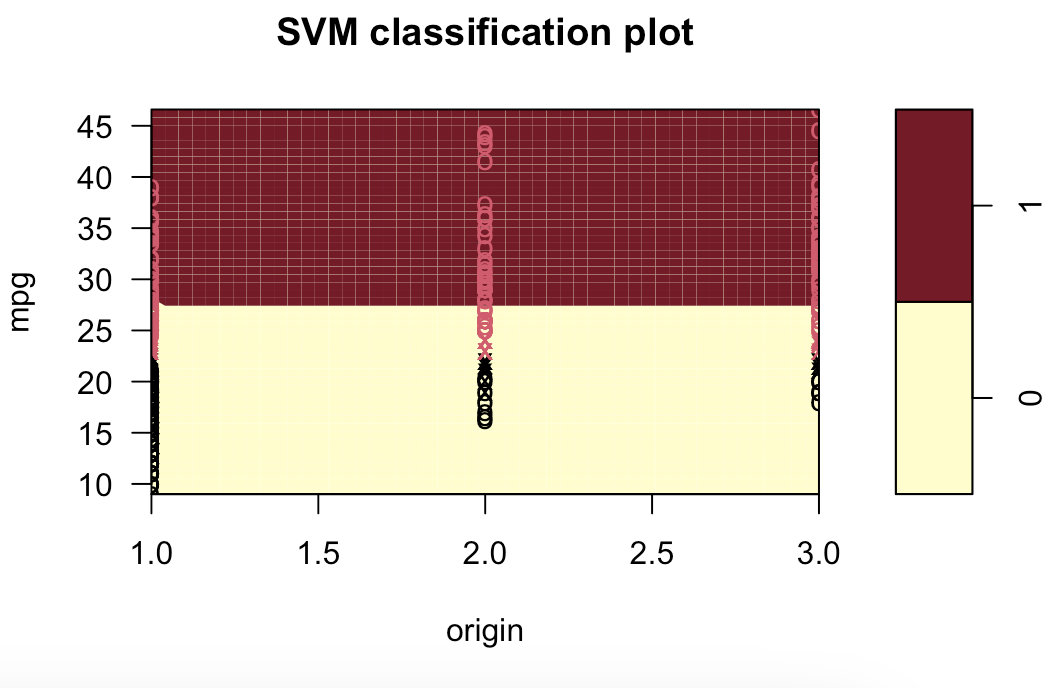

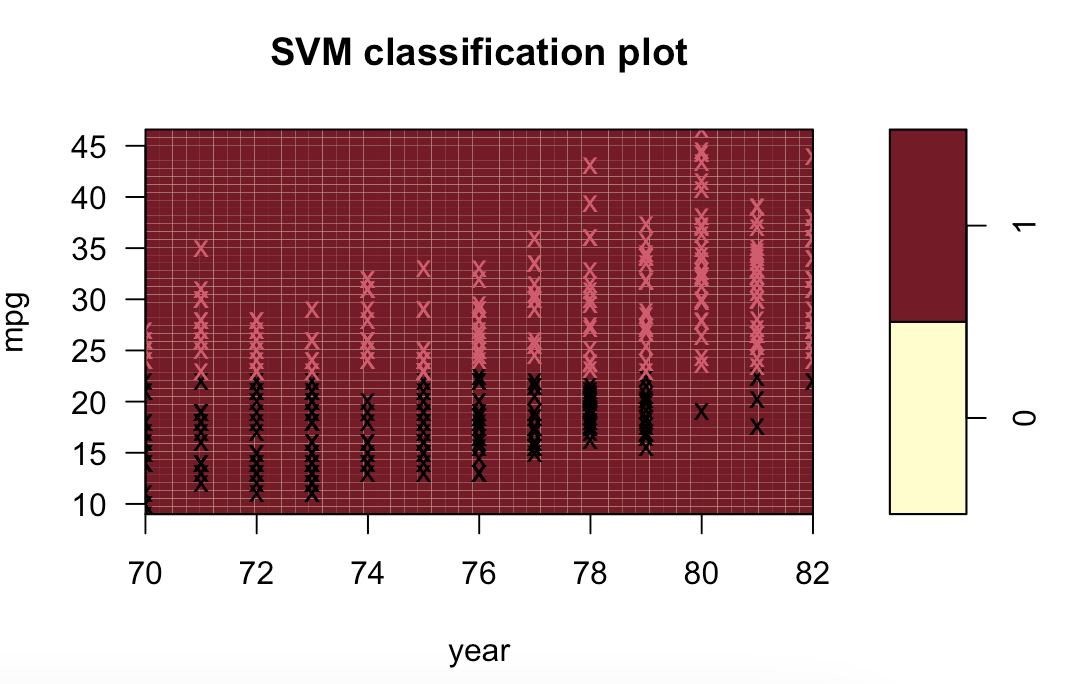

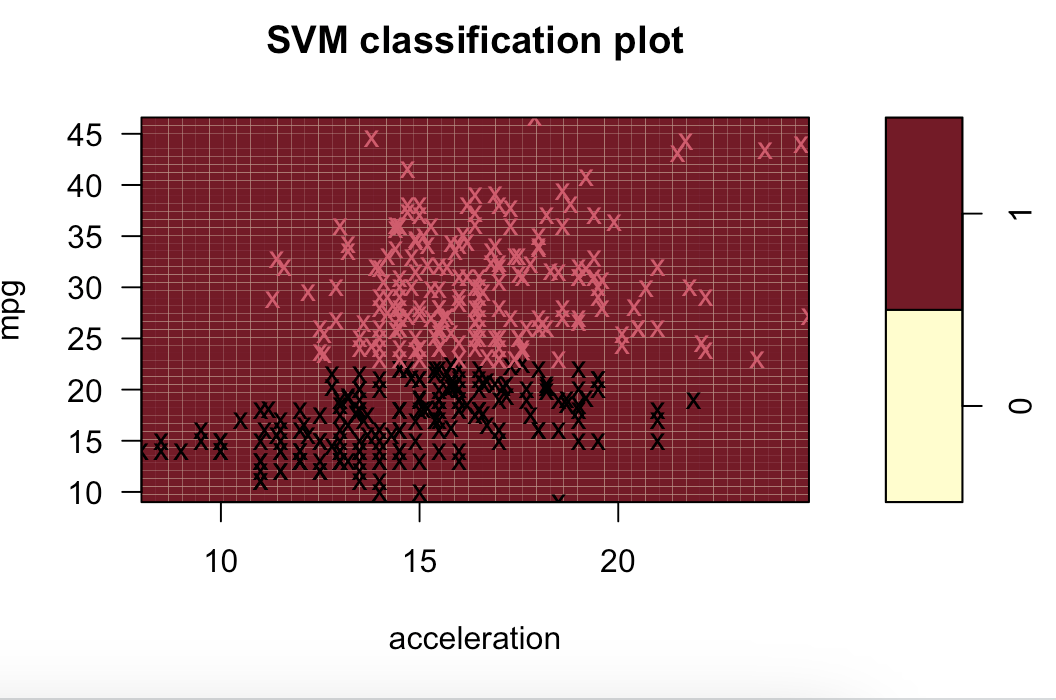

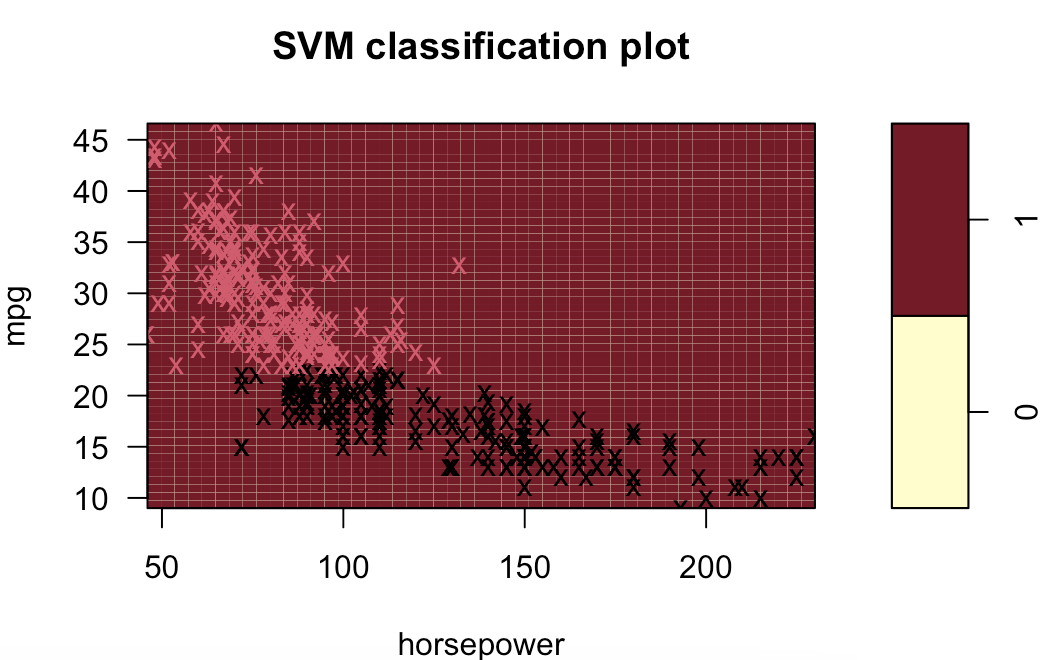

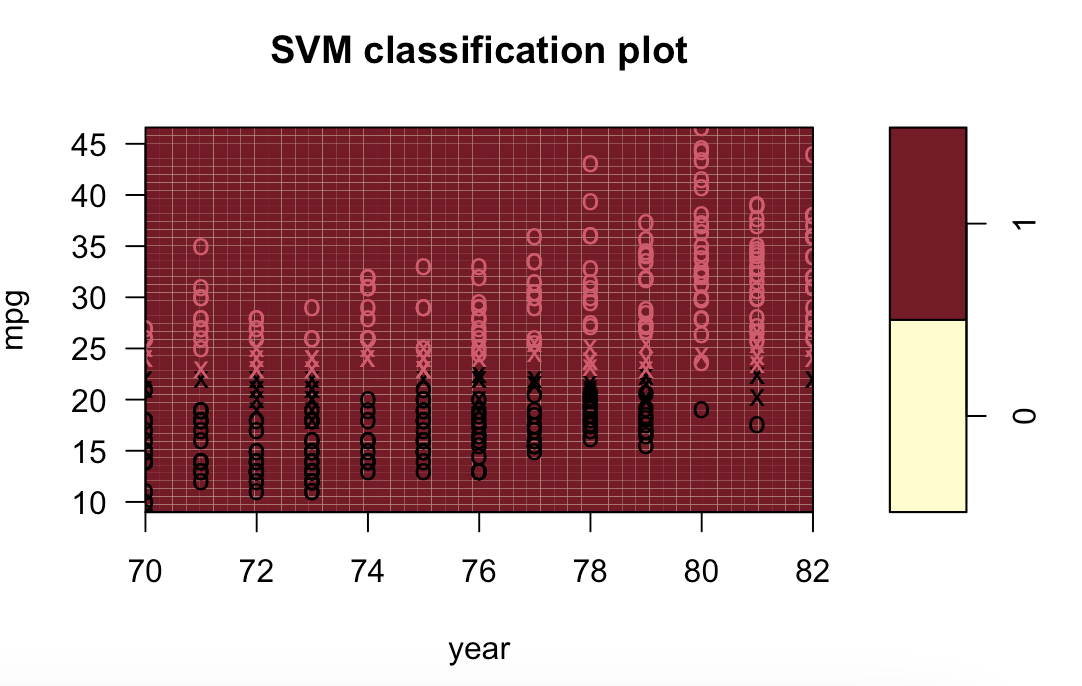

# 9.(d) ### 线性模型 svm.linear = svm(mpglevel ~ ., data = Auto, kernel = "linear", cost = 1) svm.poly = svm(mpglevel ~ ., data = Auto, kernel = "polynomial", cost = 10, degree = 2) svm.radial = svm(mpglevel ~ ., data = Auto, kernel = "radial", cost = 10, gamma = 0.01) plotpairs = function(fit) { for (name in names(Auto)[!(names(Auto) %in% c("mpg", "mpglevel", "name"))]) { plot(fit, Auto, as.formula(paste("mpg~", name, sep = ""))) } } plotpairs(svm.linear) plotpairs(svm.poly) plotpairs(svm.radial) 线性:

多项式(列出部分):

径向(列出部分):

完整代码

# 7.(a) library(ISLR) gas.med = median(Auto$mpg) new.var = ifelse(Auto$mpg > gas.med, 1, 0) Auto$mpglevel = as.factor(new.var) # 7.(b) library(e1071) set.seed(3255) tune.out = tune(svm, mpglevel ~ ., data = Auto, kernel = "linear", ranges = list(cost = c(0.01, 0.1, 1, 5, 10, 100))) summary(tune.out) ## 从结果可以看出:当采用 10 折交叉验证,当 cost=1 时,error 最小 # 7.(c) ### 多项式核函数 set.seed(21) tune.out = tune(svm, mpglevel ~ ., data = Auto, kernel = "polynomial", ranges = list(cost = c(0.1, 1, 5, 10), degree = c(2, 3, 4))) summary(tune.out) ## 当 cost=10,degree=2 时,error 最小。 ### 径向核函数 set.seed(463) tune.out = tune(svm, mpglevel ~ ., data = Auto, kernel = "radial", ranges = list(cost = c(0.1, 1, 5, 10), gamma = c(0.01, 0.1, 1, 5, 10, 100))) summary(tune.out) ## 当 cost=10,gamma=0.01 时,error 最小 # 9.(d) ### 线性模型 svm.linear = svm(mpglevel ~ ., data = Auto, kernel = "linear", cost = 1) svm.poly = svm(mpglevel ~ ., data = Auto, kernel = "polynomial", cost = 10, degree = 2) svm.radial = svm(mpglevel ~ ., data = Auto, kernel = "radial", cost = 10, gamma = 0.01) plotpairs = function(fit) { for (name in names(Auto)[!(names(Auto) %in% c("mpg", "mpglevel", "name"))]) { plot(fit, Auto, as.formula(paste("mpg~", name, sep = ""))) } } plotpairs(svm.linear) plotpairs(svm.poly) plotpairs(svm.radial)