[课程资料] 高级统计方法书后习题(六)

本系列内容为《统计学习导论——基于R应用》(机械工业出版社)部分课后习题答案。

本章为6.8节习题答案。

声明:本博客中的习题分享仅供学习和参考之用。请勿将其用于任何形式的学术欺骗、抄袭或违反学术诚信的行为。尊重知识,诚实学习。

如果您发现文章内容中任何不妥或错误之处,请随时通过联系方式或评论功能与我交流,以便我进行改正和完善。

一、概念题

6.8.3

在该问题中,题目要求最小化残差和并引入了L1正则化约束\sum_{j=1}^{p}|\beta_j| \le s。而传统的Lasso回归要求最小化残差平方和且引入L1正则化约束。但是二者本质上相似,对于约束部分的效果也相同,都是对回归系数的绝对值进行惩罚。

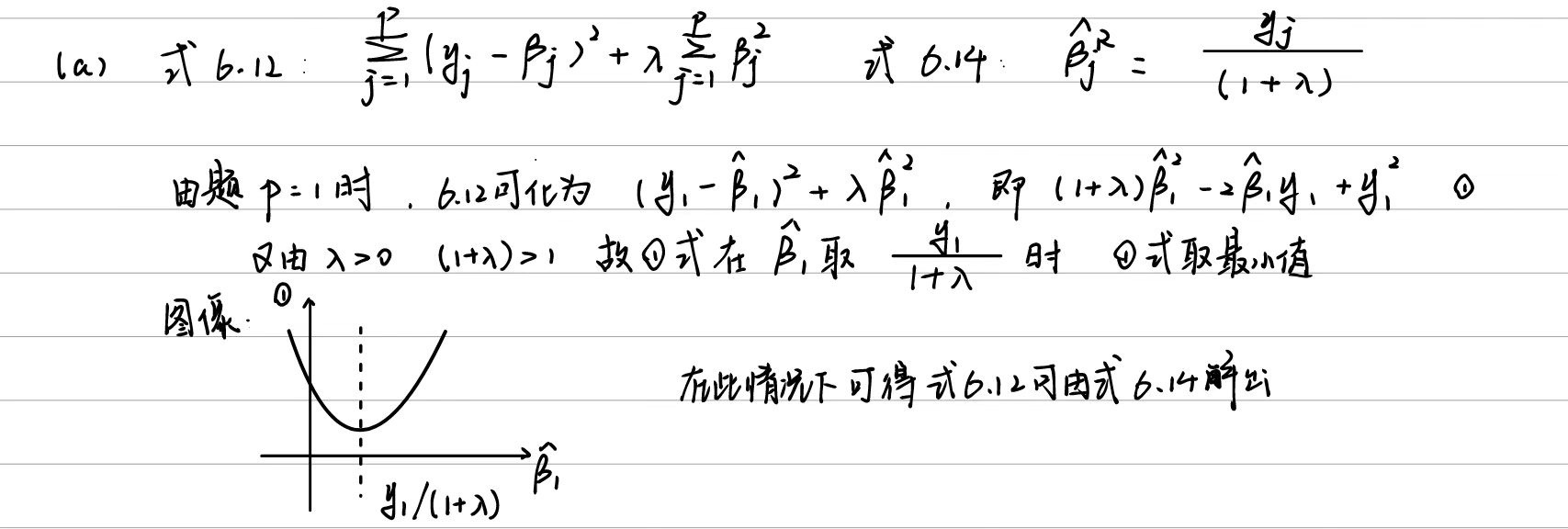

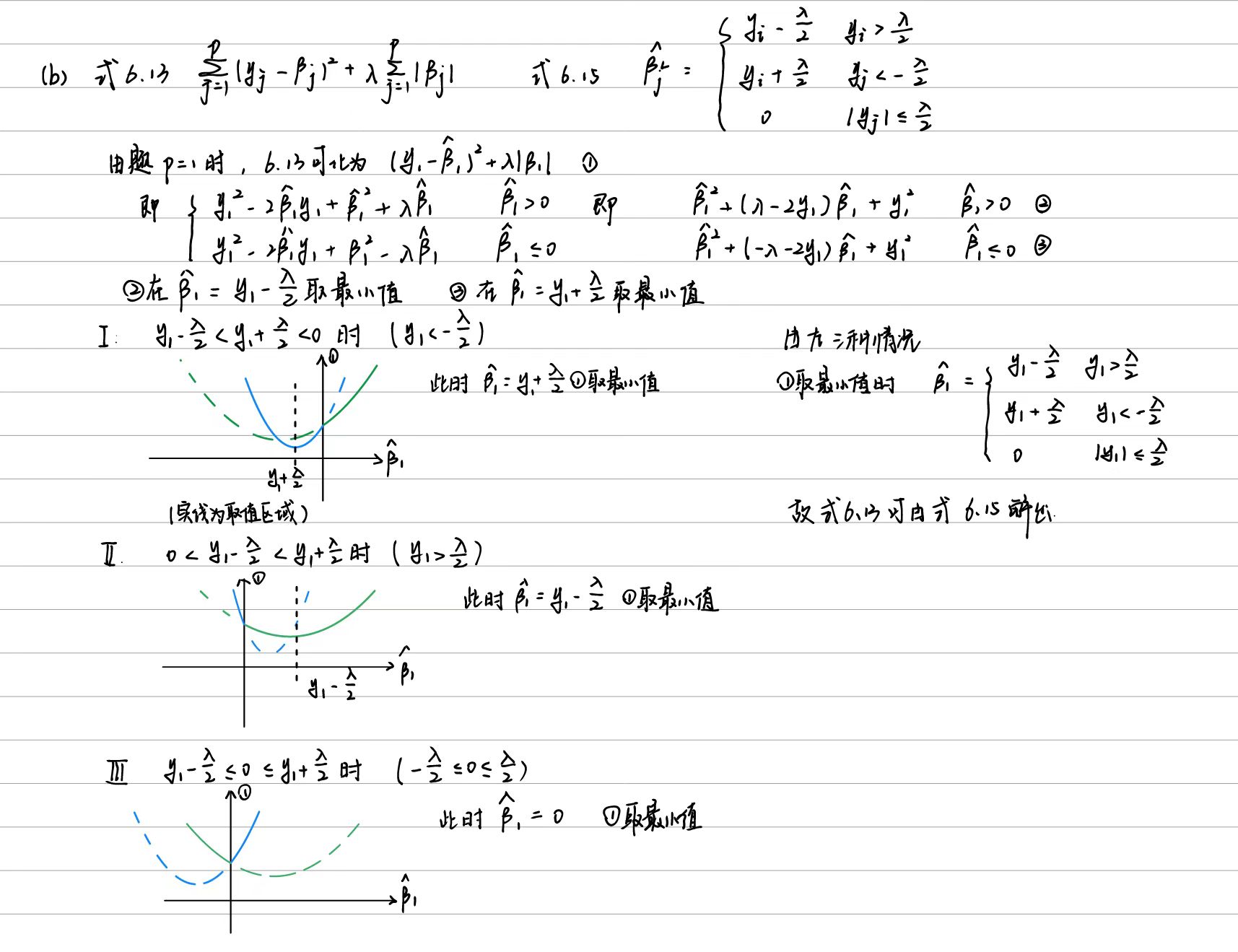

(a)

随着s从0开始增加,对系数的约束也从严格变得宽松。当s=0时,那么要求所有的\beta_j均为0,模型自由度很低。当s足够大时,那么模型也趋近于标准的最小二乘回归。可以看出随着s的增加,模型自由度有所增加,那么在训练集上的拟合效果也就会变好,训练集RSS也会变小。

(b)

随着s的增加,模型自由度逐渐从零模型趋向标准最小二乘回归。期间当s逐渐从0增加到某一特定值的过程中,模型能够使用更多的特征来拟合数据,自由度也趋近于真实情况,此时测试集RSS会随着拟合效果趋于真实情况而减小。当s从特定值再增加的时候,此时自由度的情况开始超过真实情况,出现过拟合的情况,此时模型已经使用了过多的特征,测试集RSS开始增大。综上,测试集RSS最初减小,然后开始增加,图像呈现一个U形。

(c)

当s很小的时候,模型自由度很低,模型使用的特征也很少,所以对数据敏感度很低,方差也比较低。随着s增加,模型自由度提升,对数据敏感度也提高,此时方差就会逐渐变大。所以随着s从0开始增加,方差稳定增长。

(d)

随着s增加,约束放松,模型自由度升高,在测试集上能够更好的拟合数据,能够更好的捕捉数据的模式,偏差稳定减小。

(e)

s的变化会改变对系数的约束,从而影响模型复杂度。而不可约误差是数据本身的固有误差,不会根据模型的改变(包括复杂度的改变)而发生改变。所以随着s增加,不可约误差保持不变。

6.8.4

在该问题中,题目要求最小化残差和并引入了L2正则化约束(正则化项\lambda\sum_{j=1}^{p}\beta^2_j)。而传统的岭回归则是要求最小化残差平方和且引入L2正则化约束。但是二者本质上相似,对于约束部分的效果也相同,都是对回归系数的平方值进行惩罚。

(a)

当λ=0时,表示对系数没有约束,那么模型会尽可能拟合数据,拟合效果最好,此时训练RSS最小。随着λ增大,对系数约束增强,惩罚增强,从而模型的复杂度会降低,导致在训练集上拟合效果变差,训练RSS逐渐增大。综上,随着λ从0增加,训练集RSS会稳定增长。

(b)

在λ=0时,没有对系数进行约束,那么模型会使用过多的数据特征,从而导致过拟合,此时测试集RSS比较高。在λ增加之某一个特定值的期间,对系数的约束逐渐增大,模型复杂度逐渐趋近于真实情况,此时测试集RSS会逐渐减小。当λ超过某一特定值,对系数约束过大,模型复杂度开始低于真实情况,此时模型开始过于简单,出现欠拟合情况,导致测试集RSS增大。综上,测试集RSS为最初减小,然后开始增加,图像呈现一个U形。

(c)

在λ=0的时候,对系数没有约束,那么模型会尽可能的拟合数据的特征,此时对训练数据的敏感程度也最高,可能存在过拟合情况,方差最高。在λ逐渐增加的过程中,对系数约束逐渐增大,此时模型对数据敏感程度降低,从而方差也减小。综上,方差随λ增大稳定减小。

(d)

随着λ增大,对系数约束越来越强,模型灵活度越来越低,在训练数据上的拟合效果也越来越差,导致偏差越来越大。所以偏差随λ增大稳定增长。

(e)

λ的变化会改变对系数的约束,从而影响模型复杂度。而不可约误差是数据本身的固有误差,不会根据模型的改变(包括复杂度的改变)而发生改变。所以随着λ增加,不可约误差保持不变。

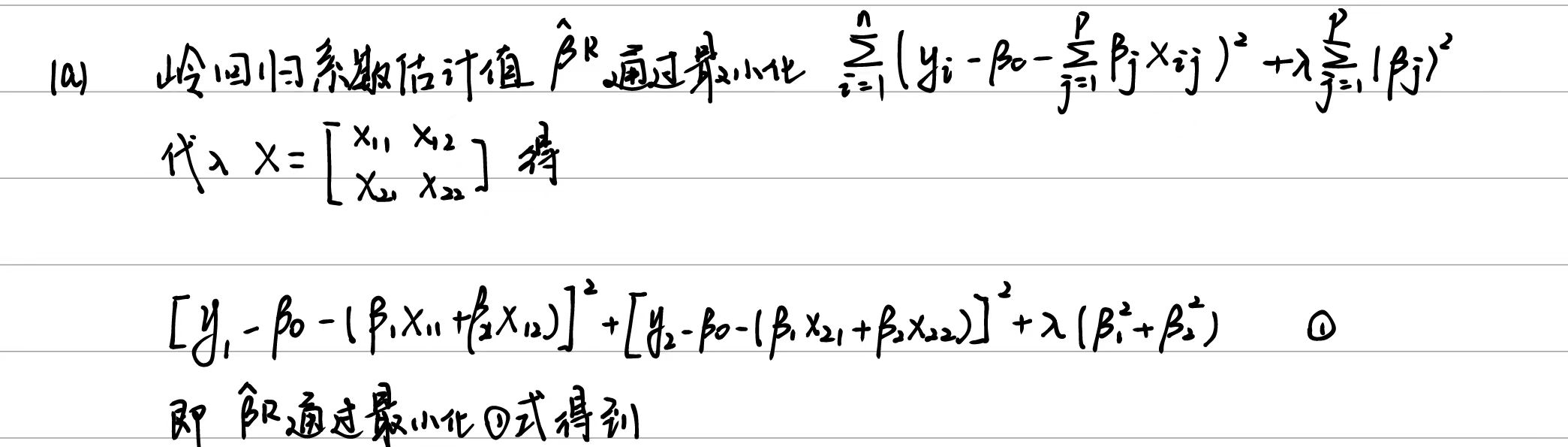

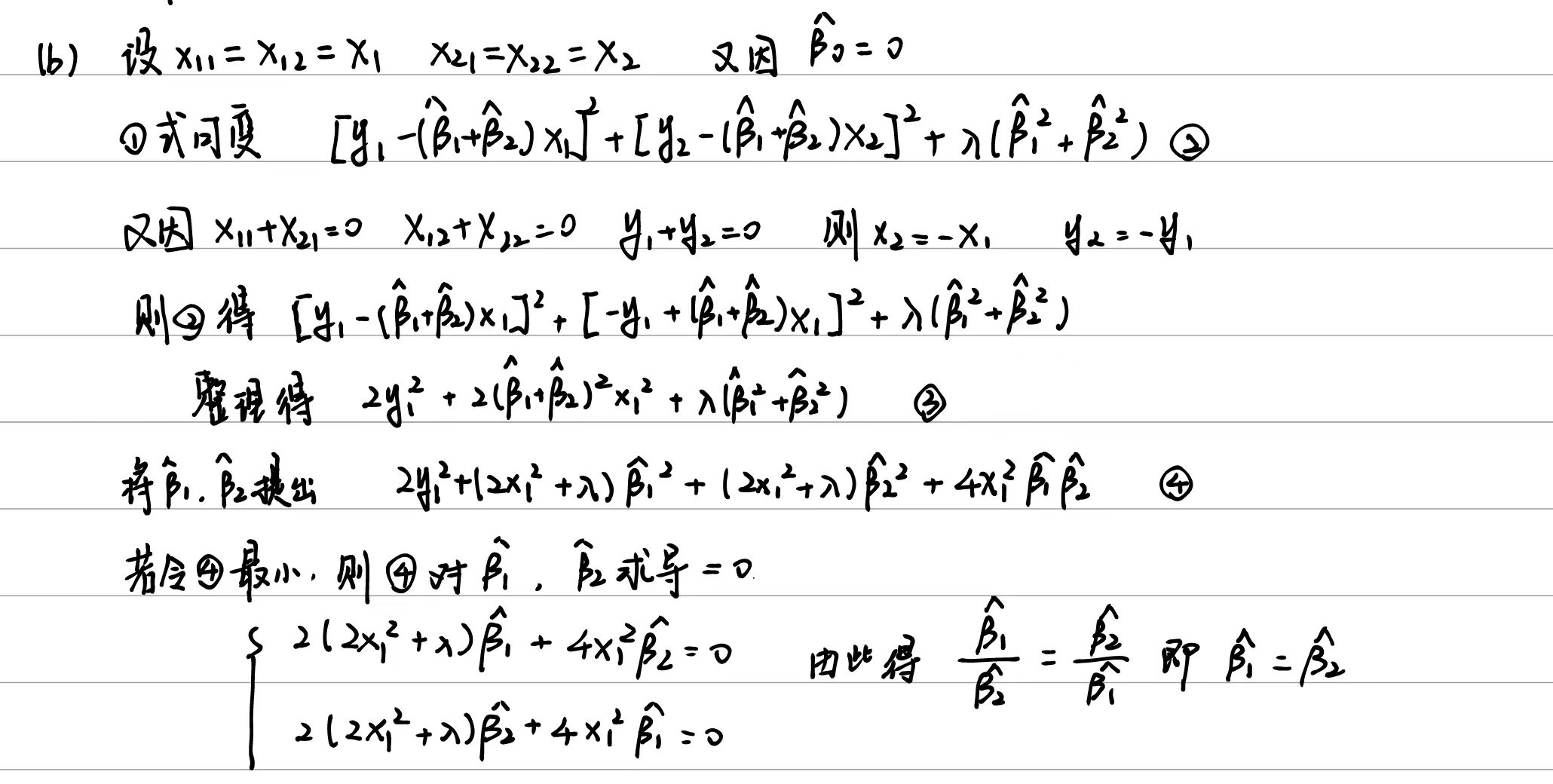

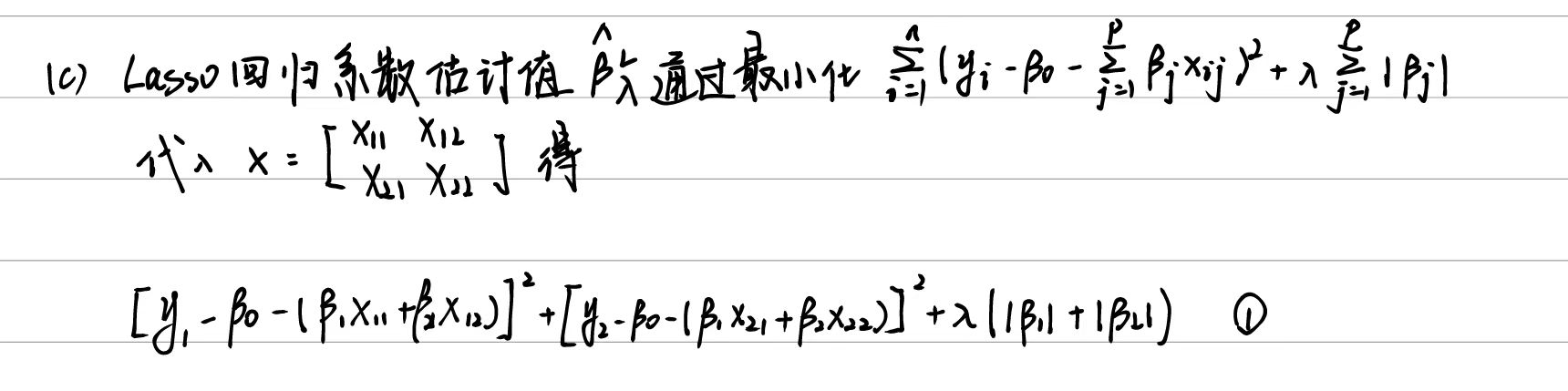

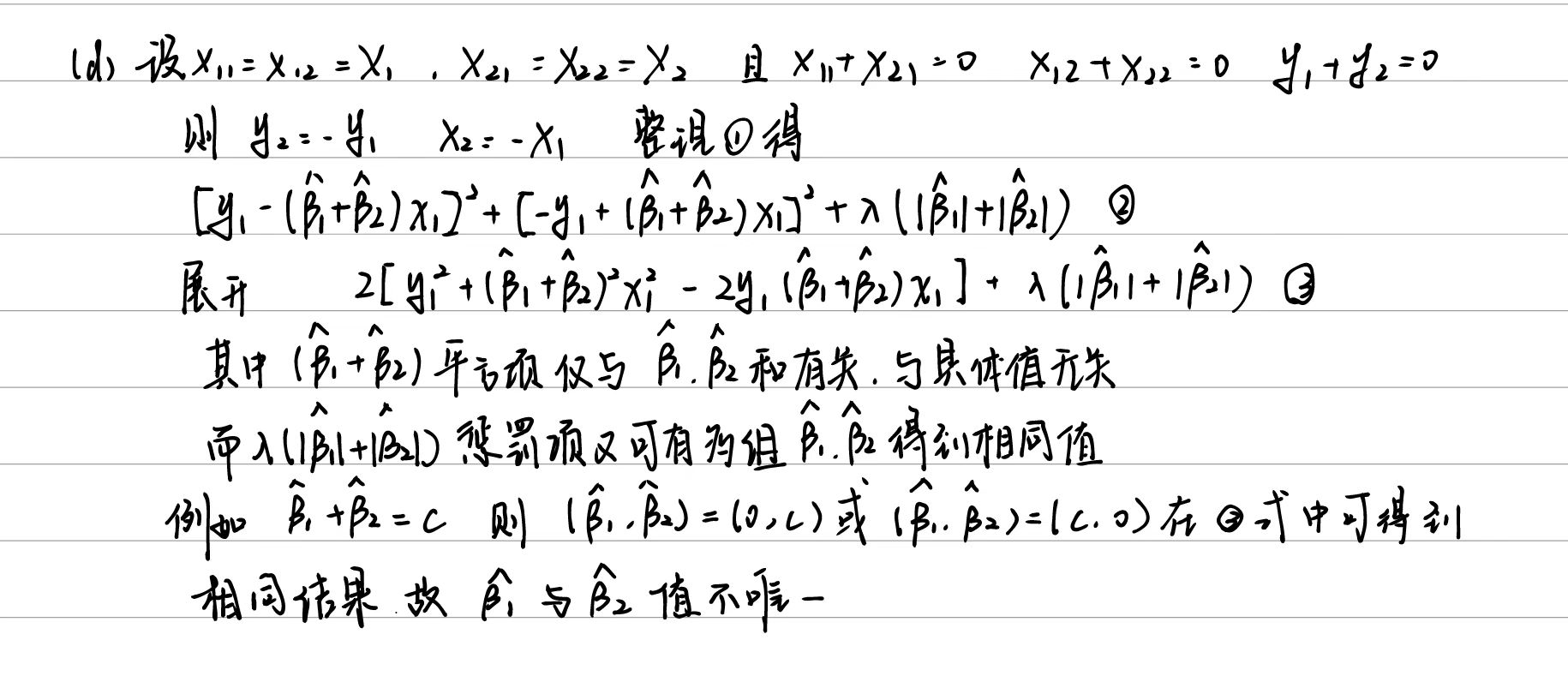

6.8.5

(a)

(b)

(c)

(d)

6.8.6

(a)

(b)

二、应用题

6.8.8

(a)

# 8.(a) set.seed(1) X = rnorm(100, mean=0, sd=1) # 默认均值为0,标准差为1 eps = rnorm(100)

(b)

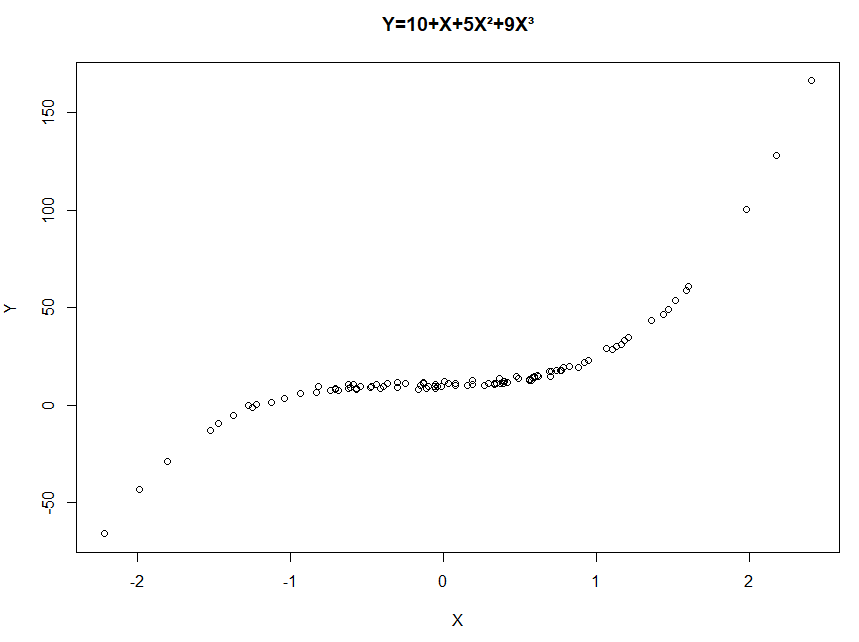

# 8.(b) ## 设置β0=10,β1=1,β2=5,β3=9 b0 = 10 b1 = 1 b2 = 5 b3 = 9 Y = b0 + b1*X + b2*X^2 + b3*X^3 + eps par(mfrow = c(1, 1)) plot(X, Y, main="Y=10+X+5X²+9X³") data.XY = data.frame(x = X, y = Y)

(c)

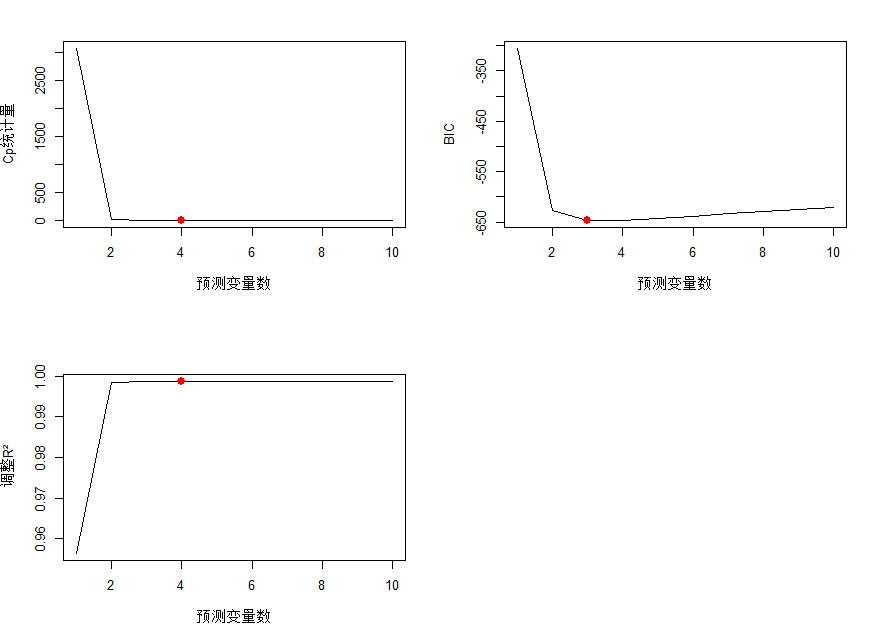

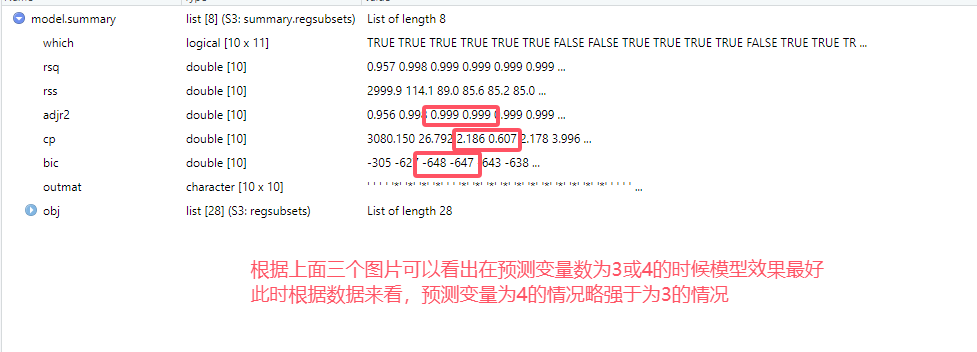

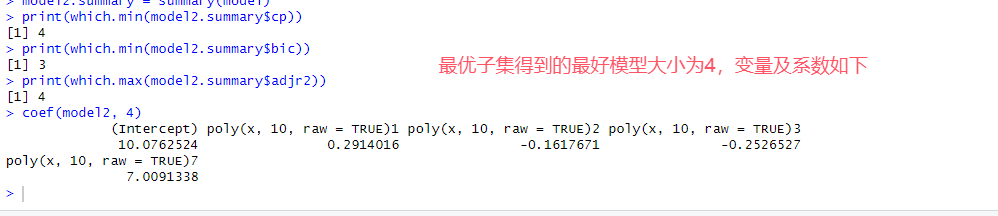

# 8.(c) library(leaps) model = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY, nvmax=10) ## ploy(x,10,raw=T)生成x到x^10的非正交多项式(非正交:原始多项式,正交:减少多重共线性) ## nvmax最大使用的参数量,即模型最大大小 summary(model) model.summary = summary(model) par(mfrow = c(2, 2)) ## Cp图 plot(1:length(model.summary$cp), model.summary$cp, xlab = "预测变量数", ylab = "Cp统计量", type = "l") ## type=l绘制线图 points(which.min(model.summary$cp), min(model.summary$cp), col = "red", cex = 2, pch = 20) ### 横轴which.min(model.summary$cp), 纵轴min(model.summary$cp), 颜色红色,大小为2,形状为填充 ## BIC plot(1:length(model.summary$bic), model.summary$bic, xlab = "预测变量数", ylab = "BIC", type = "l") points(which.min(model.summary$bic), min(model.summary$bic), col = "red", cex = 2, pch = 20) ## 调整R² plot(1:length(model.summary$adjr2), model.summary$adjr2, xlab = "预测变量数", ylab = "调整R²", type = "l") points(which.max(model.summary$adjr2), max(model.summary$adjr2), col = "red", cex = 2, pch = 20) ## 选择大小为4的模型(虽然实际情况应为3,但是得到结果为4,可能考虑eps项以及随机性) ## 模型包含 常数+一次项+二次项+三次项+五次项 coef(model, 4) ## β0=10.1 β1=1.4 β2=4.8 β3=8.6 β4=0.1

(d)

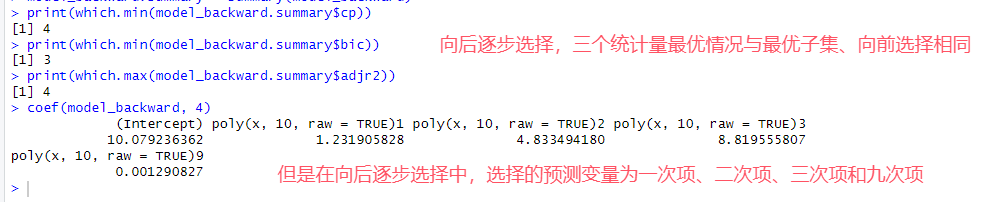

# 8.(d) model_forward = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY, nvmax=10, method="forward") model_forward.summary = summary(model_forward) print(which.min(model_forward.summary$cp)) print(which.min(model_forward.summary$bic)) print(which.max(model_forward.summary$adjr2)) coef(model_forward, 4) model_backward = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY, nvmax=10, method="backward") model_backward.summary = summary(model_backward) print(which.min(model_backward.summary$cp)) print(which.min(model_backward.summary$bic)) print(which.max(model_backward.summary$adjr2)) coef(model_backward, 4)

(e)

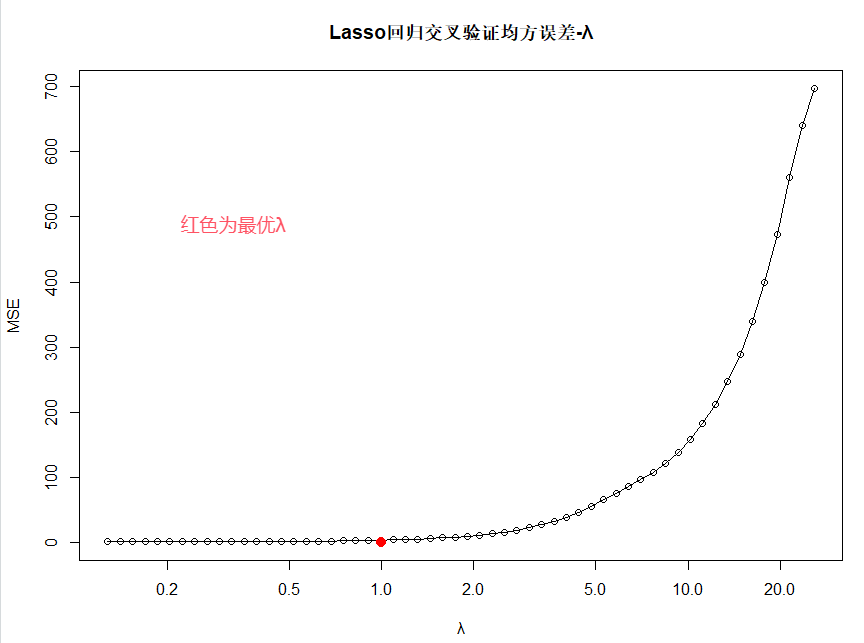

# 8.(e) library("glmnet") x = model.matrix(y ~ poly(x,10,raw=TRUE), data=data.XY)[,-1] ## 创建设计矩阵,并去掉第一列(截距列) y = data.XY$y set.seed(1) model.lasso = cv.glmnet(x, y, alpha=1, nfolds=10) ## alpha=1 Lasso =0 岭 ## nfolds=10折交叉验证 best.lambda = model.lasso$lambda.min best.lambda ## 0.128264 par(mfrow = c(1, 1)) plot(model.lasso$lambda, model.lasso$cvm, xlab="λ", ylab="MSE", main="Lasso回归交叉验证均方误差-λ", log="x", type ="o") points(which.max(best.lambda), best.lambda, col = "red", cex = 2, pch = 20) model.lasso.best = glmnet(x, y, alpha=1, lambda=best.lambda) coef(model.lasso.best)

(f)

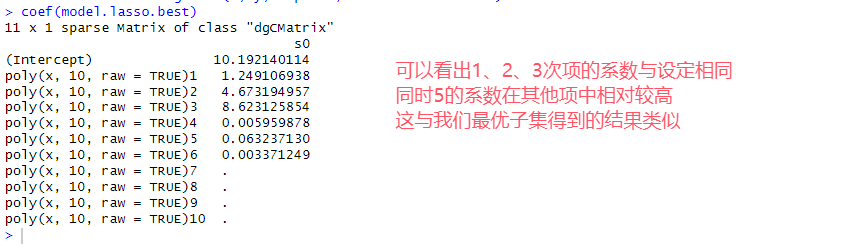

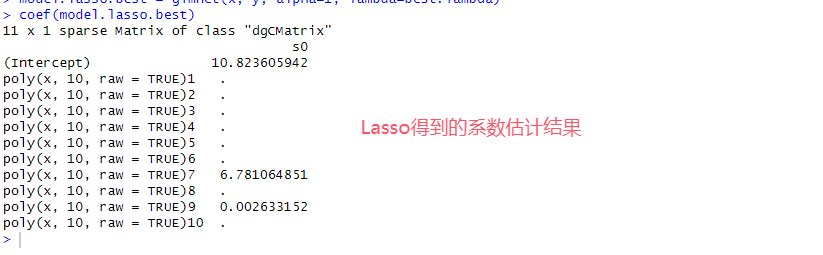

# 8.(f) Y2 = 10 + 7*X^7 + eps ## β0=10, β7=7 data.XY2 = data.frame(x=X, y=Y2) model2 = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY2, nvmax=10) model2.summary = summary(model) print(which.min(model2.summary$cp)) print(which.min(model2.summary$bic)) print(which.max(model2.summary$adjr2)) coef(model2, 4) x = model.matrix(y ~ poly(x,10,raw=TRUE), data=data.XY2)[,-1] y = data.XY2$y set.seed(1) model.lasso = cv.glmnet(x, y, alpha=1, nfolds=10) best.lambda = model.lasso$lambda.min model.lasso.best = glmnet(x, y, alpha=1, lambda=best.lambda) coef(model.lasso.best) ## 两种方法在七次项的系数均接近真实值7,而其他项系数均接近0

完整代码

# 8.(a) set.seed(1) X = rnorm(100, mean=0, sd=1) # 默认均值为0,标准差为1 eps = rnorm(100) # 8.(b) ## 设置β0=10,β1=1,β2=5,β3=9 b0 = 10 b1 = 1 b2 = 5 b3 = 9 Y = b0 + b1*X + b2*X^2 + b3*X^3 + eps par(mfrow = c(1, 1)) plot(X, Y, main="Y=10+X+5X²+9X³") data.XY = data.frame(x = X, y = Y) # 8.(c) library(leaps) model = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY, nvmax=10) ## ploy(x,10,raw=T)生成x到x^10的非正交多项式(非正交:原始多项式,正交:减少多重共线性) ## nvmax最大使用的参数量,即模型最大大小 summary(model) model.summary = summary(model) par(mfrow = c(2, 2)) ## Cp图 plot(1:length(model.summary$cp), model.summary$cp, xlab = "预测变量数", ylab = "Cp统计量", type = "l") ## type=l绘制线图 points(which.min(model.summary$cp), min(model.summary$cp), col = "red", cex = 2, pch = 20) ### 横轴which.min(model.summary$cp), 纵轴min(model.summary$cp), 颜色红色,大小为2,形状为填充 ## BIC plot(1:length(model.summary$bic), model.summary$bic, xlab = "预测变量数", ylab = "BIC", type = "l") points(which.min(model.summary$bic), min(model.summary$bic), col = "red", cex = 2, pch = 20) ## 调整R² plot(1:length(model.summary$adjr2), model.summary$adjr2, xlab = "预测变量数", ylab = "调整R²", type = "l") points(which.max(model.summary$adjr2), max(model.summary$adjr2), col = "red", cex = 2, pch = 20) ## 选择大小为4的模型(虽然实际情况应为3,但是得到结果为4,可能考虑eps项以及随机性) ## 模型包含 常数+一次项+二次项+三次项+五次项 coef(model, 4) ## β0=10.1 β1=1.4 β2=4.8 β3=8.6 β4=0.1 # 8.(d) model_forward = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY, nvmax=10, method="forward") model_forward.summary = summary(model_forward) print(which.min(model_forward.summary$cp)) print(which.min(model_forward.summary$bic)) print(which.max(model_forward.summary$adjr2)) coef(model_forward, 4) model_backward = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY, nvmax=10, method="backward") model_backward.summary = summary(model_backward) print(which.min(model_backward.summary$cp)) print(which.min(model_backward.summary$bic)) print(which.max(model_backward.summary$adjr2)) coef(model_backward, 4) # 8.(e) library("glmnet") x = model.matrix(y ~ poly(x,10,raw=TRUE), data=data.XY)[,-1] ## 创建设计矩阵,并去掉第一列(截距列) y = data.XY$y set.seed(1) model.lasso = cv.glmnet(x, y, alpha=1, nfolds=10) ## alpha=1 Lasso =0 岭 ## nfolds=10折交叉验证 best.lambda = model.lasso$lambda.min best.lambda ## 0.128264 par(mfrow = c(1, 1)) plot(model.lasso$lambda, model.lasso$cvm, xlab="λ", ylab="MSE", main="Lasso回归交叉验证均方误差-λ", log="x", type ="o") points(which.max(best.lambda), best.lambda, col = "red", cex = 2, pch = 20) model.lasso.best = glmnet(x, y, alpha=1, lambda=best.lambda) coef(model.lasso.best) # 8.(f) Y2 = 10 + 7*X^7 + eps ## β0=10, β7=7 data.XY2 = data.frame(x=X, y=Y2) model2 = regsubsets(y~poly(x,10,raw=TRUE), data=data.XY2, nvmax=10) model2.summary = summary(model) print(which.min(model2.summary$cp)) print(which.min(model2.summary$bic)) print(which.max(model2.summary$adjr2)) coef(model2, 4) x = model.matrix(y ~ poly(x,10,raw=TRUE), data=data.XY2)[,-1] y = data.XY2$y set.seed(1) model.lasso = cv.glmnet(x, y, alpha=1, nfolds=10) best.lambda = model.lasso$lambda.min model.lasso.best = glmnet(x, y, alpha=1, lambda=best.lambda) coef(model.lasso.best) ## 两种方法在七次项的系数均接近真实值7,而其他项系数均接近0

6.8.9

(a)

# 9.(a) library(ISLR) set.seed(1) n = nrow(College) train_indices = sample(1:n, size=round(0.7*n)) # 训练集索引,将数据随机抽70%作为训练集 College.train = College[train_indices, ] College.test = College[-train_indices, ]

(b)

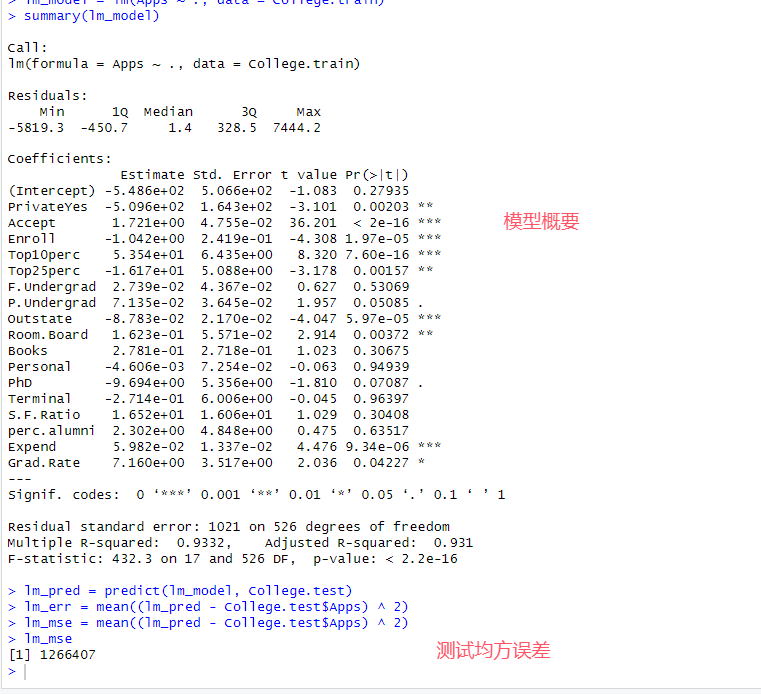

# 9.(b) lm_model = lm(Apps ~ ., data = College.train) summary(lm_model) lm_pred = predict(lm_model, College.test) # 使用模型预测测试集 lm_mse = mean((lm_pred - College.test$Apps) ^ 2) # 计算测试均方误差 lm_mse # 1266407

(c)

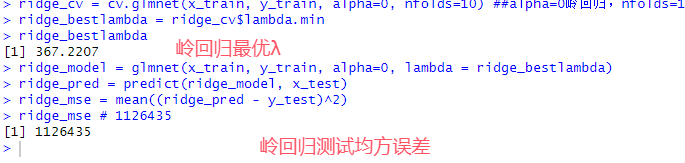

# 9.(c) x_train = model.matrix(Apps ~ ., data = College.train)[, -1] y_train = College.train$Apps x_test = model.matrix(Apps ~ ., data = College.test)[, -1] y_test = College.test$Apps set.seed(1) library(glmnet) lasso_cv = cv.glmnet(x_train, y_train, alpha=0, nfolds=10) ##alpha=0岭回归,nfolds=10十折交叉认证 lasso_bestlambda = lasso.cv$lambda.min lasso_model = glmnet(x_train, y_train, alpha=0, lambda = lasso.bestlambda) lasso_pred = predict(lasso_model, x_test) lasso_mse = mean((lasso_pred - y_test)^2) lasso_mse # 1126435

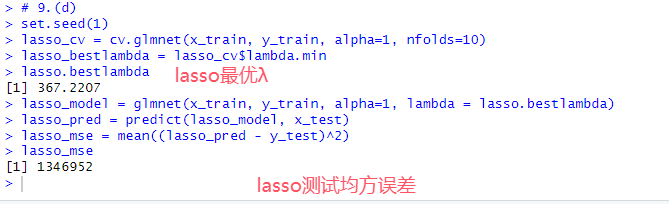

(d)

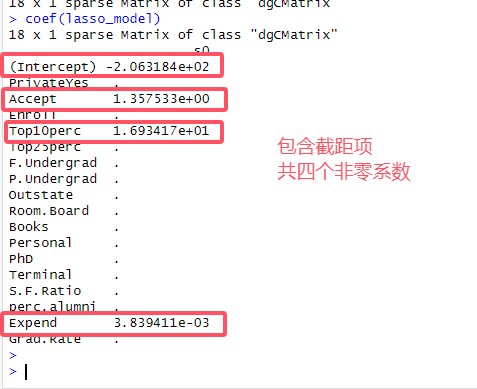

# 9.(d) set.seed(1) lasso_cv = cv.glmnet(x_train, y_train, alpha=1, nfolds=10) lasso_bestlambda = lasso_cv$lambda.min lasso.bestlambda lasso_model = glmnet(x_train, y_train, alpha=1, lambda = lasso.bestlambda) lasso_pred = predict(lasso_model, x_test) lasso_mse = mean((lasso_pred - y_test)^2) lasso_mse # 1346952 coef(lasso_model) # 根据结果共有4个非零系数(包括截距项)

(e)

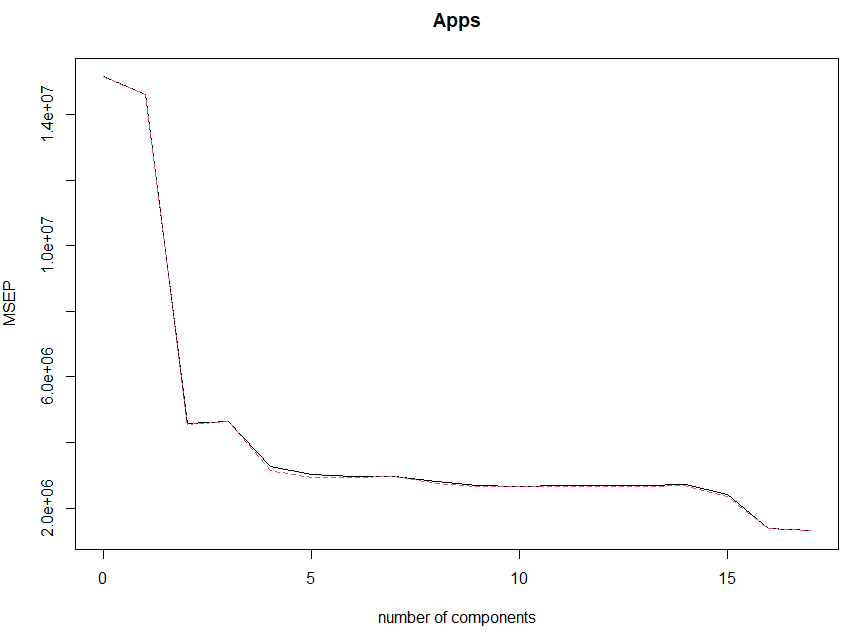

# 9.(e) library(pls) set.seed(1) pcr_cv = pcr(Apps~., data=College.train, scale=TRUE, validation="CV") #拟合PCR模型并进行交叉验证 validationplot(pcr_cv, val.type = "MSEP") # 可视化交叉验证误差,MSEP指定误差类型为均方误差 pcr_bestm = which.min(pcr_cv$validation$PRESS) # 提取使测试残差平方和(PRESS)最小的m pcr_bestm pcr_model = pcr(Apps~., data=College.train, scale=TRUE, ncomp=pcr_bestm) # 使用最佳m拟合模型 pcr_pred = predict(pcr_model, College.test, ncomp=pcr_bestm) # 使用PCR模型预测,ncomp设置使用主成分数为bestm pcr_mse = mean((pcr_pred - College.test$Apps)^2) # 计算均方误差 pcr_mse

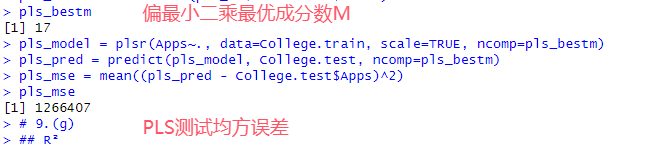

(f)

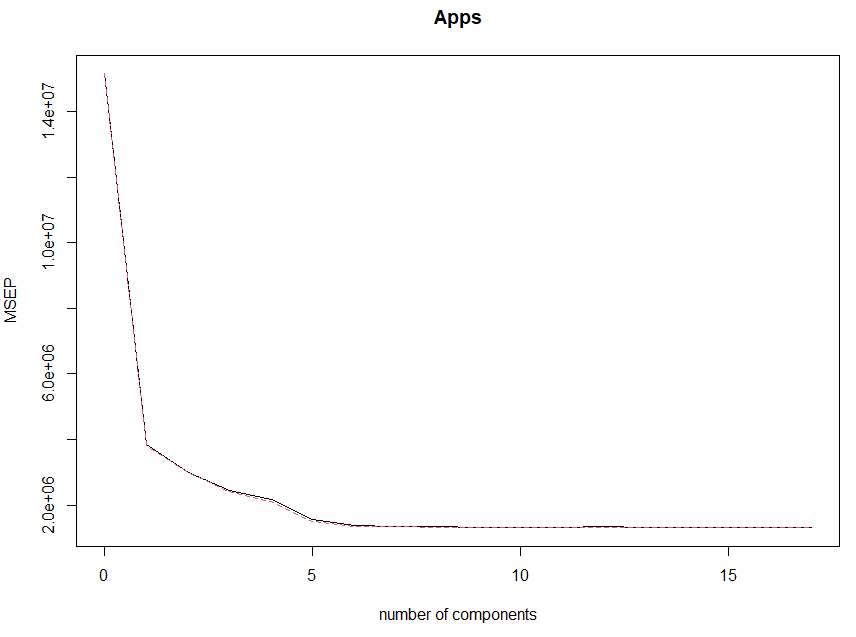

# 9.(f) set.seed(1) pls_cv = plsr(Apps~., data=College.train, scale=TRUE, validation="CV") validationplot(pls_cv, val.type = "MSEP") pls_bestm = which.min(pls_cv$validation$PRESS) pls_bestm pls_model = plsr(Apps~., data=College.train, scale=TRUE, ncomp=pls_bestm) pls_pred = predict(pls_model, College.test, ncomp=pls_bestm) pls_mse = mean((pls_pred - College.test$Apps)^2) pls_mse

(g)

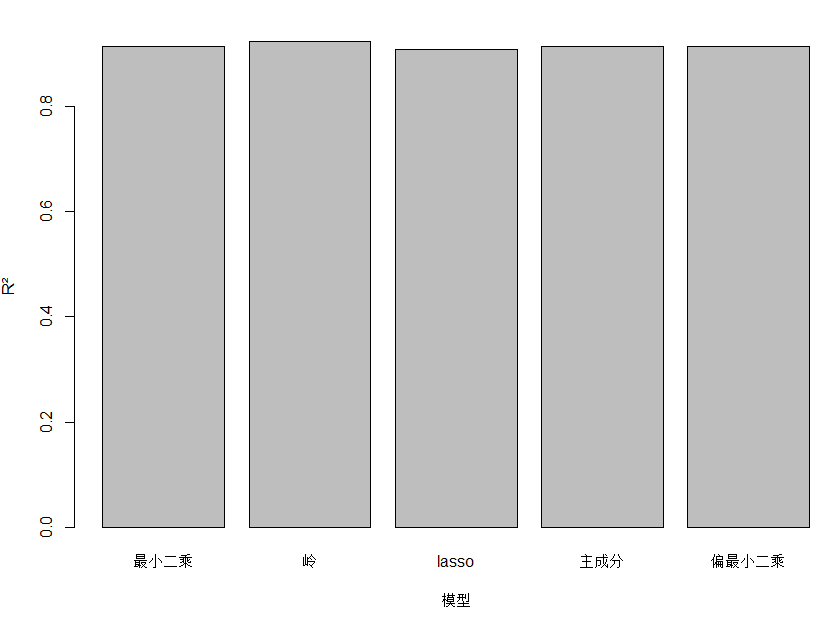

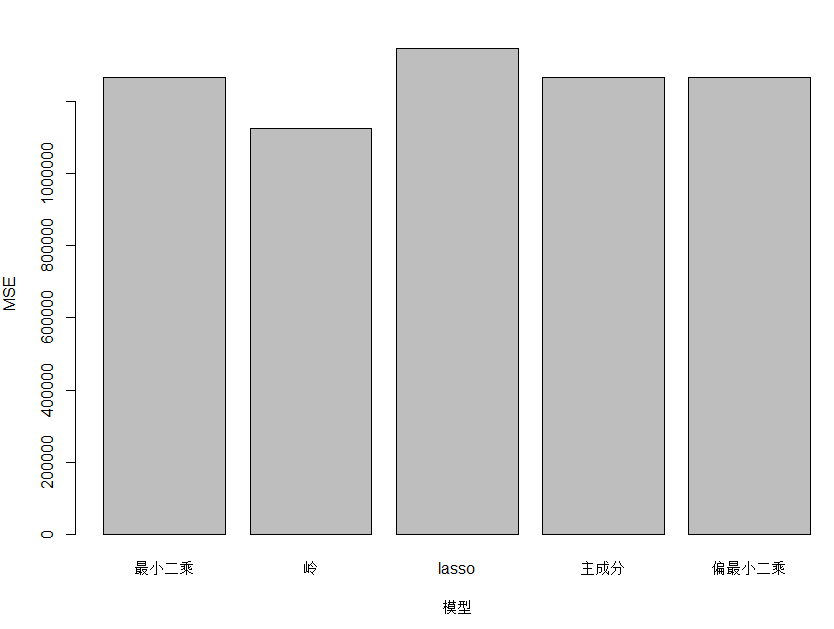

# 9.(g) y_mean = mean(y_test) lm_r2 = 1 - sum((lm_pred - y_test)^2) / sum((y_test - y_mean)^2) ridge_r2 = 1 - sum((ridge_pred - y_test)^2) / sum((y_test - y_mean)^2) lasso_r2 = 1 - sum((lasso_pred - y_test)^2) / sum((y_test - y_mean)^2) pcr_r2 = 1 - sum((pcr_pred - y_test)^2) / sum((y_test - y_mean)^2) pls_r2 = 1 - sum((pls_pred - y_test)^2) / sum((y_test - y_mean)^2) models = c("最小二乘", "岭", "lasso", "主成分", "偏最小二乘") mses = c(lm_mse, ridge_mse, lasso_mse, pcr_mse, pls_mse) r2s = c(lm_r2, ridge_r2, lasso_r2, pcr_r2, pls_r2) barplot(r2s, xlab="模型", ylab="R²", names=models) barplot(mses, xlab="模型", ylab="MSE", names=models) ## 五种模型的测试均方误差相近,并没有特别大的差别 ## 通过图像看出岭回归的R²最大,MSE最小,相对来说拟合效果最好

完整代码

# 9.(a) library(ISLR) set.seed(1) n = nrow(College) train_indices = sample(1:n, size=round(0.7*n)) # 训练集索引,将数据随机抽70%作为训练集 College.train = College[train_indices, ] College.test = College[-train_indices, ] # 9.(b) lm_model = lm(Apps ~ ., data = College.train) summary(lm_model) lm_pred = predict(lm_model, College.test) # 使用模型预测测试集 lm_mse = mean((lm_pred - College.test$Apps) ^ 2) # 计算测试均方误差 lm_mse # 1266407 # 9.(c) x_train = model.matrix(Apps ~ ., data = College.train)[, -1] y_train = College.train$Apps x_test = model.matrix(Apps ~ ., data = College.test)[, -1] y_test = College.test$Apps set.seed(1) library(glmnet) ridge_cv = cv.glmnet(x_train, y_train, alpha=0, nfolds=10) ##alpha=0岭回归,nfolds=10十折交叉认证 ridge_bestlambda = ridge_cv$lambda.min ridge_bestlambda ridge_model = glmnet(x_train, y_train, alpha=0, lambda = ridge_bestlambda) ridge_pred = predict(ridge_model, x_test) ridge_mse = mean((ridge_pred - y_test)^2) ridge_mse # 1126435 # 9.(d) set.seed(1) lasso_cv = cv.glmnet(x_train, y_train, alpha=1, nfolds=10) lasso_bestlambda = lasso_cv$lambda.min lasso.bestlambda lasso_model = glmnet(x_train, y_train, alpha=1, lambda = lasso.bestlambda) lasso_pred = predict(lasso_model, x_test) lasso_mse = mean((lasso_pred - y_test)^2) lasso_mse # 1346952 coef(lasso_model) # 根据结果共有4个非零系数(包括截距项) # 9.(e) library(pls) set.seed(1) pcr_cv = pcr(Apps~., data=College.train, scale=TRUE, validation="CV") #拟合PCR模型并进行交叉验证 scale=TRUE表示标准化解释变量 validationplot(pcr_cv, val.type = "MSEP") # 可视化交叉验证误差,MSEP指定误差类型为均方误差 pcr_bestm = which.min(pcr_cv$validation$PRESS) # 提取使测试残差平方和(PRESS)最小的m pcr_bestm pcr_model = pcr(Apps~., data=College.train, scale=TRUE, ncomp=pcr_bestm) # 使用最佳m拟合模型 pcr_pred = predict(pcr_model, College.test, ncomp=pcr_bestm) # 使用PCR模型预测,ncomp设置使用主成分数为bestm pcr_mse = mean((pcr_pred - College.test$Apps)^2) # 计算均方误差 pcr_mse # 9.(f) set.seed(1) pls_cv = plsr(Apps~., data=College.train, scale=TRUE, validation="CV") validationplot(pls_cv, val.type = "MSEP") pls_bestm = which.min(pls_cv$validation$PRESS) pls_bestm pls_model = plsr(Apps~., data=College.train, scale=TRUE, ncomp=pls_bestm) pls_pred = predict(pls_model, College.test, ncomp=pls_bestm) pls_mse = mean((pls_pred - College.test$Apps)^2) pls_mse # 9.(g) y_mean = mean(y_test) lm_r2 = 1 - sum((lm_pred - y_test)^2) / sum((y_test - y_mean)^2) ridge_r2 = 1 - sum((ridge_pred - y_test)^2) / sum((y_test - y_mean)^2) lasso_r2 = 1 - sum((lasso_pred - y_test)^2) / sum((y_test - y_mean)^2) pcr_r2 = 1 - sum((pcr_pred - y_test)^2) / sum((y_test - y_mean)^2) pls_r2 = 1 - sum((pls_pred - y_test)^2) / sum((y_test - y_mean)^2) models = c("最小二乘", "岭", "lasso", "主成分", "偏最小二乘") mses = c(lm_mse, ridge_mse, lasso_mse, pcr_mse, pls_mse) r2s = c(lm_r2, ridge_r2, lasso_r2, pcr_r2, pls_r2) barplot(r2s, xlab="模型", ylab="R²", names=models) barplot(mses, xlab="模型", ylab="MSE", names=models) ## 五种模型的测试均方误差相近,并没有特别大的差别 ## 通过图像看出岭回归的R²最大,MSE最小,相对来说拟合效果最好

6.8.10

(a)

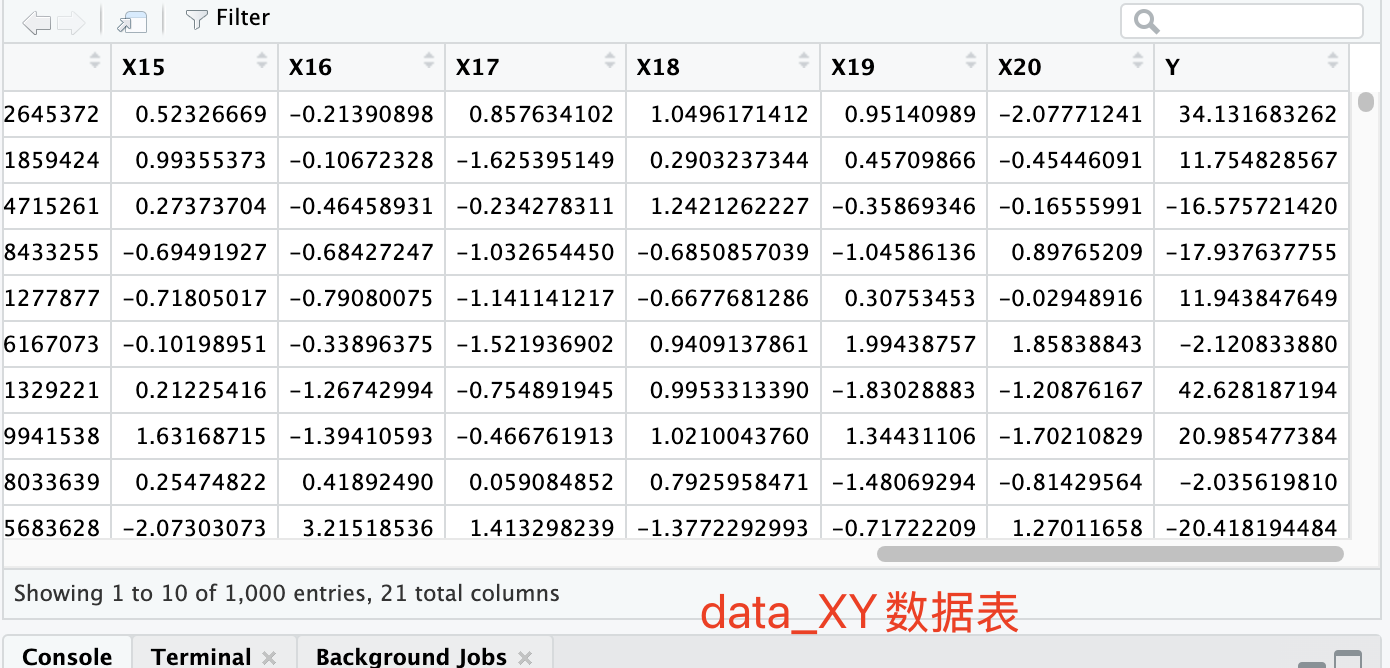

# 10.(a) set.seed(1) n = 1000 # 观测数 p = 20 # 特征数 X = matrix(rnorm(n*p), nrow = n, ncol = p) eps = rnorm(n, mean=0, sd=0.3) # 生成标准差为0.3,均值为0的误差项 beta = sample(-10:10, 20) # 生成20个beta,取值在[-10,10] beta[3] = 0 beta[7] = 0 beta[11] = 0 beta[15] = 0 beta[19] = 0 Y = X %*% beta + eps # %*%为矩阵乘法运算符 data_XY = data.frame(X, Y) # 组合数据

(b)

# 10.(b) set.seed(1) train_indices = sample(1:n, size = 100) data_train = data_XY[train_indices, ] data_test = data_XY[-train_indices, ]

(c)

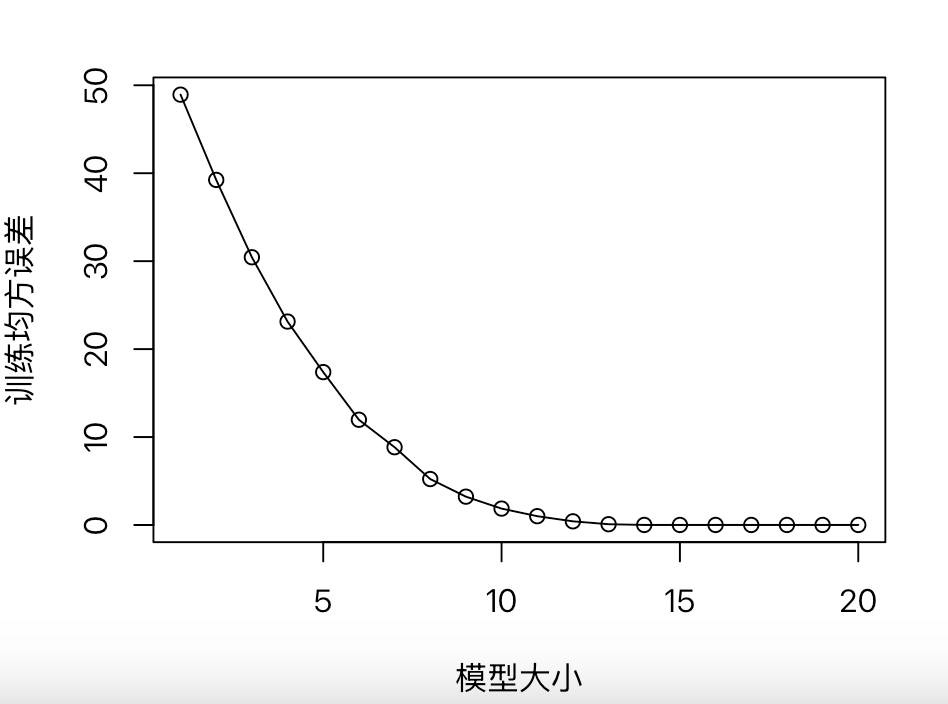

# 10.(c) library(leaps) set.seed(1) model = regsubsets(Y~., data=data_train, nvmax=20) # 使用最优子集法,最大预测变量数20 model.summary = summary(model) model.rss = model.summary$rss model.mse = model.rss / n # 均方误差=RSS/样本数 print(model.mse) plot(1:20, model.mse, xlab="模型大小", ylab="训练均方误差", pch=1, type="o")

(d)

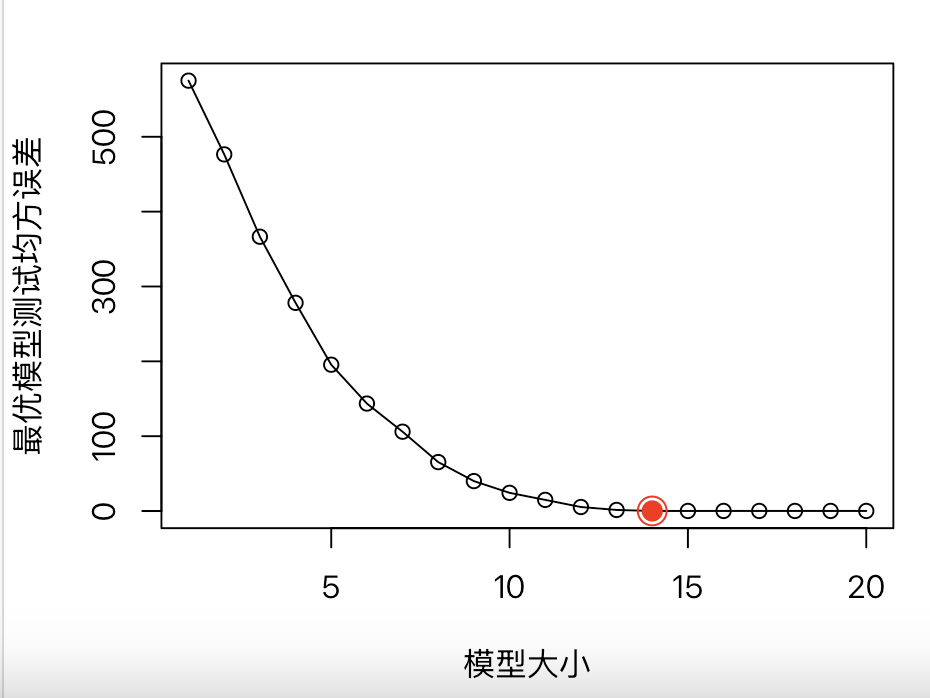

# 10.(d) library(HH) test.mse = numeric(p) # 生成一个初始化为0、包含20元素的向量 for(i in 1:20){ test.model = lm.regsubsets(model, i) # 从regsubsets对象中提取指定大小的模型 test.pred = predict(test.model, data_test) test.mse[i] = mean((test.pred - data_test$Y)^2) } test.mse plot(1:20, test.mse, xlab="模型大小", ylab="最优模型测试均方误差", pch=1, type="o")

(e)

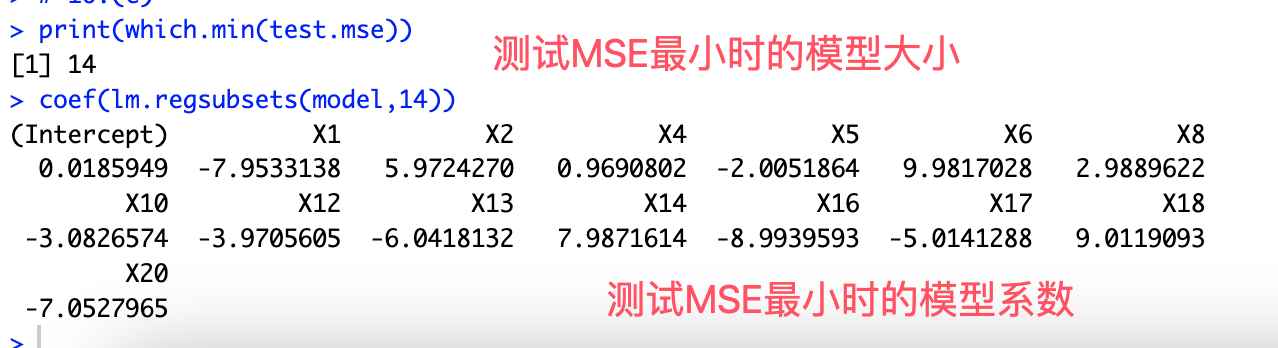

# 10.(e) print(which.min(test.mse)) coef(lm.regsubsets(model,14)) ## 可以发现在随着模型大小的提升,模型的预测变量数增加,灵活性增加 ## 拟合情况更贴近真实情况,测试MSE降低直到最小值 ## 但是随着模型大小进一步提升,预测变量数超过了真实情况 ## 从而导致在训练集上出现过拟合情况,导致测试MSE增加

(f)

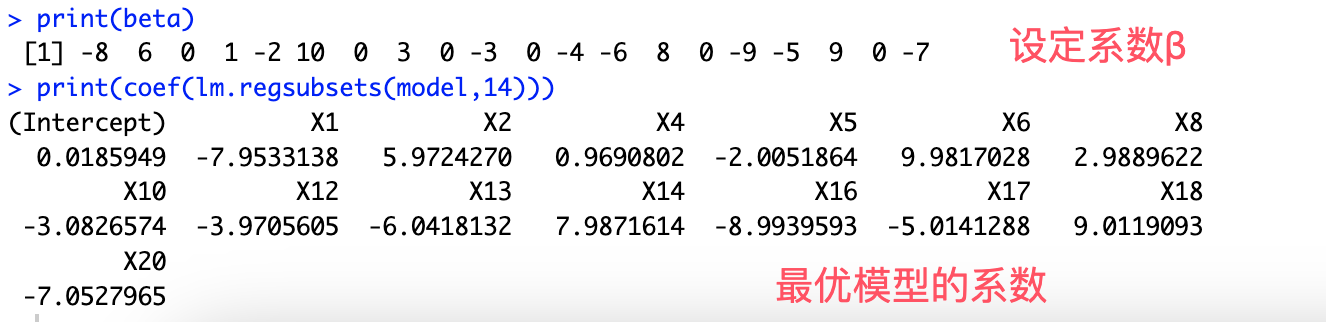

# 10.(f) print(beta) print(coef(lm.regsubsets(model,14))) ## 我们设置了5个β值为0,在这里我们得到最优模型大小为14(6个β被认为为0) ## 根据系数也可以看出,除了我们设置的五个β,这里认为β9也为0 ## 通过对比模型系数和设定系数发现二者几乎相等

(g)

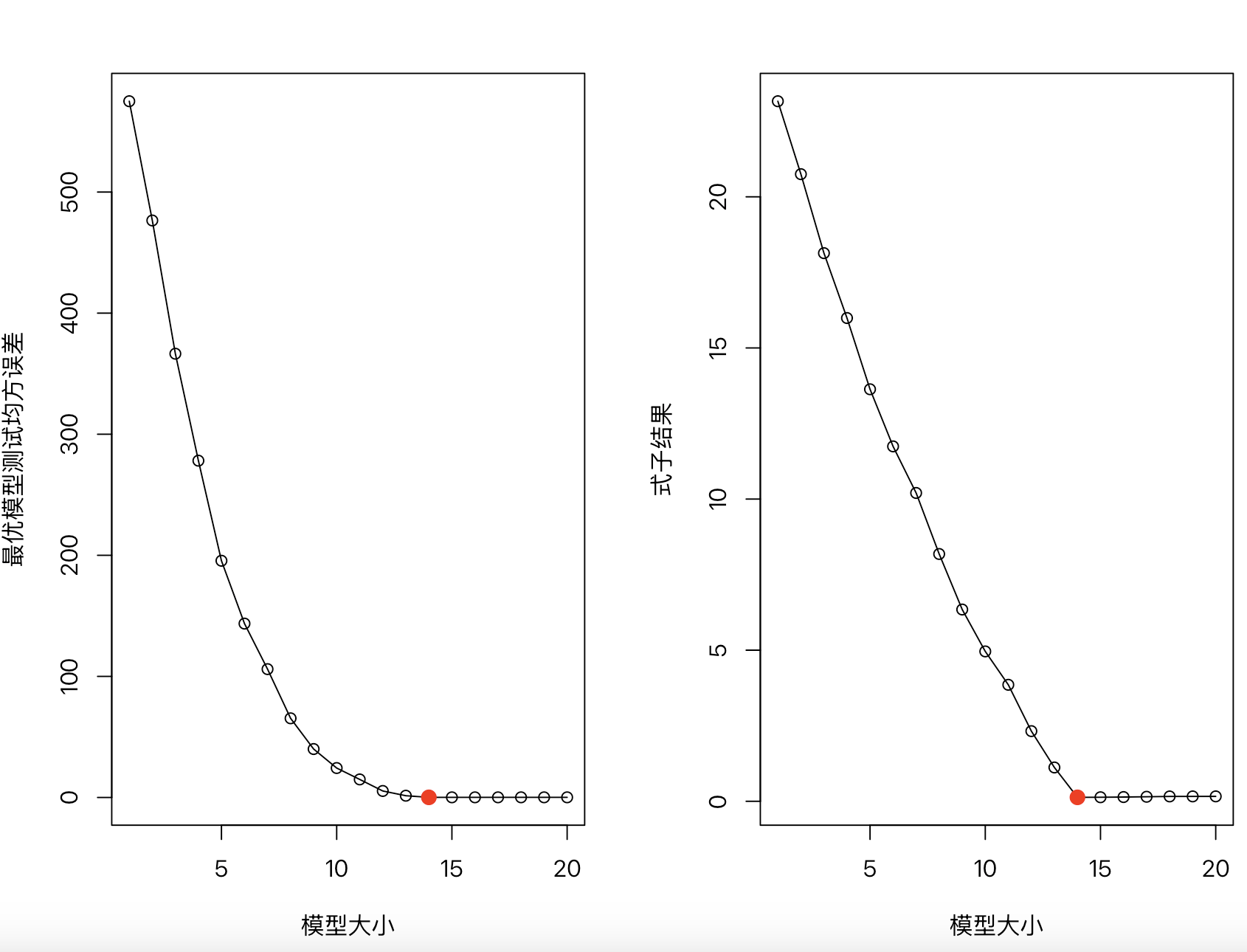

# 10.(g) result = numeric(p) for (i in 1:20) { model_coef_i = coef(lm.regsubsets(model, i)) # 获取大小为i的模型的系数 coef_i = numeric(p) # 创建一个全零的系数向量 coef_names = names(model_coef_i) # 提取变量名,排除截距项 coef_names = coef_names[coef_names != "(Intercept)"] # 逻辑索引排除截距项 coef_indices = match(coef_names, paste0("X", 1:p)) # 将变量名转换为索引并填入系数 coef_i[coef_indices] = model_coef_i[coef_names] result[i] = sqrt(sum((beta - coef_i)^2)) } par(mfrow = c(1, 2)) plot(1:20, test.mse, xlab="模型大小", ylab="最优模型测试均方误差", pch=1, type="o") points(which.min(test.mse), min(test.mse), col="red", cex=2, pch=20) plot(1:20, result, xlab="模型大小", ylab="式子结果", pch=1, type="o") points(which.min(result), min(result), col="red", cex=2, pch=20) ## 可以发现随着模型大小增加,两者先下降,并在模型大小为14时得到最小值 ## 两个图像都展示了模型大小与模型拟合效果的关系

完整代码

# 10.(a) set.seed(1) n = 1000 # 观测数 p = 20 # 特征数 X = matrix(rnorm(n*p), nrow = n, ncol = p) eps = rnorm(n, mean=0, sd=0.3) # 生成标准差为0.3,均值为0的误差项 beta = sample(-10:10, 20) # 生成20个beta,取值在[-10,10] beta[3] = 0 beta[7] = 0 beta[11] = 0 beta[15] = 0 beta[19] = 0 Y = X %*% beta + eps # %*%为矩阵乘法运算符 data_XY = data.frame(X, Y) # 组合数据 # 10.(b) set.seed(1) train_indices = sample(1:n, size = 100) data_train = data_XY[train_indices, ] data_test = data_XY[-train_indices, ] # 10.(c) library(leaps) set.seed(1) model = regsubsets(Y~., data=data_train, nvmax=20) # 使用最优子集法,最大预测变量数20 model.summary = summary(model) model.rss = model.summary$rss model.mse = model.rss / n # 均方误差=RSS/样本数 print(model.mse) plot(1:20, model.mse, xlab="模型大小", ylab="训练均方误差", pch=1, type="o") # 10.(d) library(HH) test.mse = numeric(p) # 生成一个初始化为0、包含20元素的向量 for(i in 1:20){ test.model = lm.regsubsets(model, i) # 从regsubsets对象中提取指定大小的模型 test.pred = predict(test.model, data_test) test.mse[i] = mean((test.pred - data_test$Y)^2) } test.mse plot(1:20, test.mse, xlab="模型大小", ylab="最优模型测试均方误差", pch=1, type="o") points(which.min(test.mse), min(test.mse), col="red", cex=2, pch=20) # 10.(e) print(which.min(test.mse)) coef(lm.regsubsets(model,14)) ## 可以发现在随着模型大小的提升,模型的预测变量数增加,灵活性增加 ## 拟合情况更贴近真实情况,测试MSE降低直到最小值 ## 但是随着模型大小进一步提升,预测变量数超过了真实情况 ## 从而导致在训练集上出现过拟合情况,导致测试MSE增加 # 10.(f) print(beta) print(coef(lm.regsubsets(model,14))) ## 我们设置了5个β值为0,在这里我们得到最优模型大小为14(6个β被认为为0) ## 根据系数也可以看出,除了我们设置的五个β,这里认为β9也为0 ## 通过对比模型系数和设定系数发现二者几乎相等 # 10.(g) result = numeric(p) for (i in 1:20) { model_coef_i = coef(lm.regsubsets(model, i)) # 获取大小为i的模型的系数 coef_i = numeric(p) # 创建一个全零的系数向量 coef_names = names(model_coef_i) # 提取变量名,排除截距项 coef_names = coef_names[coef_names != "(Intercept)"] # 逻辑索引排除截距项 coef_indices = match(coef_names, paste0("X", 1:p)) # 将变量名转换为索引并填入系数 coef_i[coef_indices] = model_coef_i[coef_names] result[i] = sqrt(sum((beta - coef_i)^2)) } par(mfrow = c(1, 2)) plot(1:20, test.mse, xlab="模型大小", ylab="最优模型测试均方误差", pch=1, type="o") points(which.min(test.mse), min(test.mse), col="red", cex=2, pch=20) plot(1:20, result, xlab="模型大小", ylab="式子结果", pch=1, type="o") points(which.min(result), min(result), col="red", cex=2, pch=20) ## 可以发现随着模型大小增加,两者先下降,并在模型大小为14时得到最小值 ## 两个图像都展示了模型大小与模型拟合效果的关系